Download

1 / 20

200 likes | 412 Views

Understanding Goodwill and When to Appraise the Loss. Presented to the 1 st Joint Luncheon IRWA – Chapter 1 and The Los Angeles Chapter of the ASA by Dave Girbovan, ASA and Vanita Spaulding, CFA, ASA. Today’s Discussion. Intangible assets valued in Purchase Price Allocation Studies

E N D

Understanding Goodwill and When to Appraise the Loss Presented to the 1st Joint Luncheon IRWA – Chapter 1 and The Los Angeles Chapter of the ASA by Dave Girbovan, ASA and Vanita Spaulding, CFA, ASA

Today’s Discussion • Intangible assets valued in Purchase Price Allocation Studies • The Micro and Macro Approach • Goodwill can be narrowly or broadly defined • The basics of the Aklilu case • When lost goodwill is appraised. • The effects of relocation on specific intangible assets.

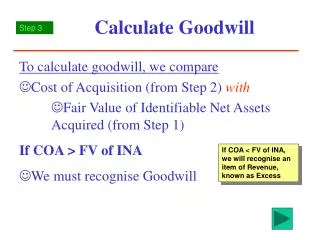

Purchase Price Allocation Studies • Purpose – To allocate the premium paid for a company in excess of the tangible assets to specific categories of intangible assets. • Provides additional amortization resulting in tax savings.

Historical Example • MegaHuge Conglomerate acquires the assets of PalTron for $100 million. • The current assets and fixed assets have a value of $60 million. • The company was not allowed to amortize the residual of $40 million if booked as goodwill. • Significant tax savings result when a portion of the premium is allocated to identified, amortizable, intangible assets.

Two Phases of the Study • Macro Approach – An income approach resulting in the acquisition price. • Micro Approach – All intangible assets are value and assigned a useful remaining life.

Categories of Intangible Assets • Trademarks • Trade Names • Proprietary Technology • Internally Created Software • Assembled Work Force • Favorable Contracts • Advertising Programs • Distribution Networks • Training Materials • Customer Lists • Going Concern Value • Licenses and Certifications • Favorable Leases • Goodwill

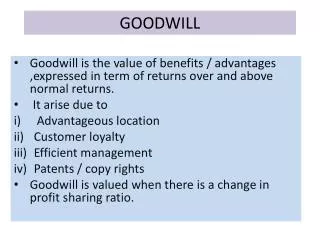

Broad and Narrow Definitions of Goodwill • Goodwill narrowly defined in purchase price allocation studies. • Goodwill in eminent domain is broadly defined. • Marketable licenses (Liquor) are separated. • Favorable leases are separated. • Everything else is included in goodwill.

Broad Definition of Goodwill • Although goodwill is broadly defined in eminent domain, considering the components is useful to: • Determine if and why a business may have goodwill, • Where a business may need to relocate so that goodwill can be preserved, and • Analyze how a relocation may affect goodwill

Methods to Value Intangibles • Income Approach • Preferable • Value based on income potential • Market Approach • Rarely used • Cost Approach – Cost to Create • Represents a sunk cost

Cost to Create Method • By acquiring an operating company one can avoid the costs to create those assets and the costs represent their value. • An investor would pay no more for an asset than the cost to create the asset.

Cost to Create Method • Examples • Assembled work force • Cost to hire, train and orient employees • Going concern value • Can avoid start up losses • Key Point • The actual sale of the company established that intangible asset exists • As confirmed by the macro approach, the business is expected to be profitable.

Cost to Create Method • Drawbacks • Method does not incorporate economic benefits of the intangibles. • Information regarding the trend of the economic benefits is lacking. • Duration of the benefits not considered. • Sunk costs.

Inglewood Redevelopment Agency v. Aklilu, Cal.App 2 Dist., 2007 • Facts • Auto Inn Lube and Oil was started in 1997 by Elias Aklilu • Believed it would take 3 to 5 years to be successful. • Construction of the Marketplace at Hollywood Park disrupted the business from 1999 to 2002. • In 2003 the Marketplace was largely completed, traffic returned to normal, and the business became profitable. • Complaint filed in October 2004.

The Aklilu Case • Valuation Approaches • Both appraisers agreed no goodwill using historic statements and traditional approaches. • Chris Pedersen for the business owner used a cost to create method. The adjusted historic losses were added to arrive at goodwill of $238,761. • Chris Pedersen qualitatively established goodwill, citing a fine location, outstanding exposure, excellent parking and access, and no competition. The business had a “very promising future”.

The Aklilu Case • Issue on Appeal – Is the cost to create method valid to appraise lost business goodwill? • The Appellate Court said yes. • Adopted a point of view from Muller case that Code Section 1263.510 should be liberally construed.

The Aklilu Case • Discussion Points • The business’s past was not indicative of its future • Historic losses are sunk costs • Goodwill was qualitatively established • A dangerous precedent • What method has more typically been used to appraise goodwill under these circumstances? • Distinction from Redevelopment Agency of the city of San Diego v. Ahmad Mesdaq.

The Effects of Relocation on Goodwill • Can examine each category of intangible assets to determine how goodwill may be affected. • Also helps to establish primary and secondary relocation areas • Primary relocation area is where the most goodwill may be preserved • Secondary relocation area may preserve some goodwill.

When to Appraise the Loss • Possibilities • Before relocation • After relocation • Often do not have a choice • Not always better off waiting • Must recognize appraising lost business goodwill is somewhat subjective.

Examining Goodwill Before and After Relocation • If appraising goodwill in the after condition prior to an actual relocation, the before condition model is alter to reflect the anticipated effects of relocation on the business. • If appraising goodwill in the after condition after the actual relocation, the appraiser must be careful to consider changes not attributable to relocation.

Examples of When to Appraise the Loss • Some agencies have given the business owner the choice on when lost business goodwill is appraised. • Value loss before example. • Value loss after example.