Download

1 / 54

560 likes | 974 Views

UNBC Retirement Savings Plan Defined Contribution Pension Plan (DCPP). why save? Getting started my plan Your plan advantage my investments Investment review Choosing your funds my account Get involved. Saving for Retirement. How much money do you need for retirement?.

E N D

UNBC Retirement Savings Plan Defined Contribution Pension Plan (DCPP)

why save? • Getting started my plan • Your plan advantage my investments • Investment review • Choosing your funds my account • Get involved

How much money do you need for retirement? Canadians need 65% to 80% pre-retirement income replacement

Where will your money come from? Retirement income supplement CPP/OAS Home secondary Other Savings Personal RRSP primary UNBC Defined Contribution Pension Plan

Government benefits Request your CPP/QPP contributions & benefit statement from: www.servicecanada.gc.ca * Rates above as of April 2009

Benefits of starting early Assumes a 6% rate of return

Sun Life Financial InvestmentManagers You/member UNBC • Your Account • Making contributions • Understanding investments • Choosing investments • Monitoring savings and investments • Filing personal information updates • RRSP limits • Paying investment • management fees • Payingwithdrawal fees • Sponsor the plan • Pension Committee • Plan design • Selecting Investment Managers • Selecting funds • Selecting the record keeper • Monitoring the plan • Record keeping • Preparing statements • Developing tools • Member education • Tracking your investments • Tax receipts • Funds • Performing research • Creating the fund • Selecting the stocksor bonds • Buying and selling Responsibilities Insert Slide Title Here

2008 $21,000 2009 $22,000 2010 indexed DC Plan contribution limits Lesser of 18% of current years earnings or $22,000 • Includes: • Your contributions • UNBC’s contributions • Additional voluntary contributions DC Pension Plan Contributions are part of your Pension Adjustment, show up on your T4 slip and affect the amount that you can contribute to your RRSP

2008 $20,000 2009 $21,000 2010 $22,000 RRSP contribution limits Lesser of 18% of previous years earnings or $21,000 Pension Adjustment (PA)* Unused RRSP Room (if any) - + For your information about your personal limits visit www.cra.gc.ca • Pension Adjustment (PA) shown on T4.

2009 Plan Contributions UNBC Registered Pension Plan Registered Retirement Savings Plan (RRSP) UNBC Employee Compulsory • 3% of earnings up to the YMPE • 5% above the YMPE • Additional Voluntary (no match) • Transfers-in allowed • 8% of earnings up to the YMPE • 10% above the YMPE 2009 YMPE = Yearly Maximum Pensionable Earnings = $46,300.

Doing the math Assumption: Mary earns $65,000 annually. Registered Retirement Savings Plan (RRSP) Mary $46,300 x 3% = $1,389.00 Mary $18,700 x 5% = $ 935.00 UNBC $46,300 x 8% = $3,704.00 UNBC $18,700 x 10% = $1,870.00 Total Benefit = $7,898.00

When do you own the funds? • Vesting • Vesting refers to when you own the University contributions. You are vested after 2 years of continuous service with the University. • If you leave UNBC prior to 2 years of continuous service, contributions are not yours to take with you. • You always own your contributions. • Locking in • Once you have been contributing into the DCPP for 2 years, the funds become locked in which means they are not available for you to use until you retire. Registered Retirement Savings Plan (RRSP) Mary $44,900 x 3% = $1,263.00 Mary $ 7,900 x 5% = $ 395.00 UNBC $44,900 x 8% = $3,368.00 UNBC $ 7,900 x 10% = $ 790.00 Total Benefit = $5,816.00

What happens if you…. What happens if you…. What happens if you… • Leave UNBC • Transfer your DCPP to: • Locked in account with Sun Life Financial - CHOICES • Locked in account at another financial institution • A new employer (if permitted) • Retire from UNBC • Transfer your DCPP to: • A LIF (Life Income Fund) with Sun Life Financial - CHOICES • A LIF at another financial institution • Purchase an annuity

You get it all when you save through your company plan × × × × × × × × × × × × × × × × ×

Your steps to investing • Understand the basics • types of funds • risk vs. returns • importance of diversification • Determine what type of investor you are • Choose your funds • refer to theInvestment Reportssection through your online account

Understand risk vs. return • Money market • Federal government debt • Short term, less than 1 year • Bonds • Promise to repay debt • Receives interest • Various terms to maturity • Government and corporate • Balanced • Mix of cash, bond and equities • Automatic diversification • Equities • Ownership in company • Share in company profits • Canadian or foreign

$35,000 $30,000 $25,000 $20,000 $15,000 $10,000 $5,000 Dec 98 Dec 99 Dec 00 Dec 01 Dec 02 Dec 03 Dec 04 Dec 05 Dec 06 Dec 07 Dec 08 TSX DEX 91-Day T-Bill Index TSX DEX Universe Bond Index S&P/TSX Composite Index Consumer Price Index Growth of $10,000 (January 1999 – December 2008) $18,000 $18,000 $17,200 $17,200 $14,400 $14,400 $12,500 Source : Morningstar.ca

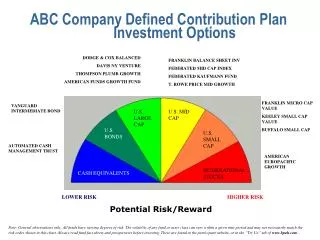

Ways you can diversify Asset Class Manager Style Foreign Markets Sector Diversify your investments • Diversification: holding different types of investments in your portfolio • Lower your overall risk by:not putting all of your eggs in one basket

Think about investing outside of Canada • Canada Revenue Agency now allows100%foreign content in your registered accounts • Canada represents only2-3%of the world stock market • Some foreign markets have historically outperformed Canada over the long-term • Consider investing outside of Canada as one way to diversify

Investment Manager approaches Active Objective is tooutperform a market indexbased on research of current market conditions and company prospects Actively buys and sells securities in individual funds Passive or Index Simply buys and sells assets tomatch characteristics of an index, fundperformance should be similar to the index, i.e. S&P TSX Fund Manager applies an Investment “style” to their approach BonaVista, Beutel Goodman McLean Budden, PH&N, CI Fund Management Fees tend to be lower than an Active Fund Manager BGI

Investment styles Value Focuses on stocks that a fund manager thinks are currentlyundervalued in price and will eventually have their worth recognized by the market Growth Believes that the single most important thing driving stock pricesis rapidlyrising corporate earnings-- and that's what they look for If the manager is right, the stock will increase in price as others in the market recognize the true value of the stock CI, BonaVista, Beutel Goodman If the manager is right, the company’s stock will increase in price as the company achieves business and earnings growth McLean Budden

Investment styles GARP Growth at a reasonable price - looks for stocks of growth companies that they canbuy for a reasonable price This is a combination of value and growth investing McLean Budden Global

Dollar cost averaging Dollar cost averaging Market Value = $3,557.96 Rate of Return = 18.59%

mymoney Investment Risk Profiler Your guide to choosing funds • Complete the questionnaire in theInvestment Risk Profileronline • www.sunlife.ca/member • Review your fund choices online throughMorningstar® • Select your funds according to your risk tolerance

Building your own asset mix Example: A score of 36 to 85 points - Moderate 15% Intl. Equity 10% Money Market 15% U.S. Equity 40% Fixed Income 20% CDN. Equity

1 year later Starting point 5% 5% 10% 45% 35% 60% 45% 60% Stocks Transfer: 10% Cdn Equity to Bonds 5% Cdn Equity to International Equity Rebalance often to match your risk tolerance Starting point 10% 10% 35% Bonds 45% Bonds 45% 45% 45% 45% Stocks International Equity Canadian Equity Bonds

Fund Performance Data through 31 Dec 2008

Fund Performance Data through 31 Dec 2008

Example $10,000 Fund Management % 0.70% Annual Fees $70.00 To view your fees visit www.sunlife.ca/member Understanding Fees Fund Management Fee (expressed as a % of fund assets you hold)

Investment management fee Annual contributions Years of contributions 2% $5,000 20 1.5% $5,000 20 Ending balance 2% $148,588 1% $167,568 1.5% $157,752 1% $5,000 20 Total contribution: $100,000 Low Fund Management Fees (FMF) make a difference * Assumes a 5.75% real rate of return

Retirement Planning Tools

Plan Member Website • SelectResource Centre • Click on My Money Tools Sign in to www.sunlife.ca/member

mymoney retirement planner • my information • This is the first screen of the retirement planner • Some of the information on this screen is pre-populated

mymoney retirement planner • my assets • Enter any additional assets or income you have • You can include pensions from previous employers

mymoney retirement planner • my lifestyle • A lifestyle is suggested based on your personal information • You can view information on other lifestyles • Select your lifestyle and receive your personal action plan

mymoney retirement planner Your personal action plan

Keeping you involved Read your personal statements • Quarterly (Available Online) • Easy to read • Personal rates of return • Summary of all plans • Transaction history • Plan information • Bulletin board

Keeping you involved Internet www.sunlife.ca/member Customer Care Centre 1-866-733-8612 • Receive up-to-date account balances • View transaction history • Make investment changes • Link directly to investment reports • View online member statements • 24 hour automated phone account access • Representatives available every business day (8 am to 8 pm ET) • Account updates • 150 languages supported

Getting information about your funds (Morningstar®) Investment Information • Capital market performance • Individual fund performance • Investment style, fund and manager updates Portfolio X-Ray • Analyze different combinations of funds as a single portfolio; including the effect of asset allocation changes to the portfolio Fund Compare • Compare and analyze funds in your plan with the full list of available funds Performance Reports • Generate investment performance reports for your plan’s funds