Download

1 / 5

50 likes | 51 Views

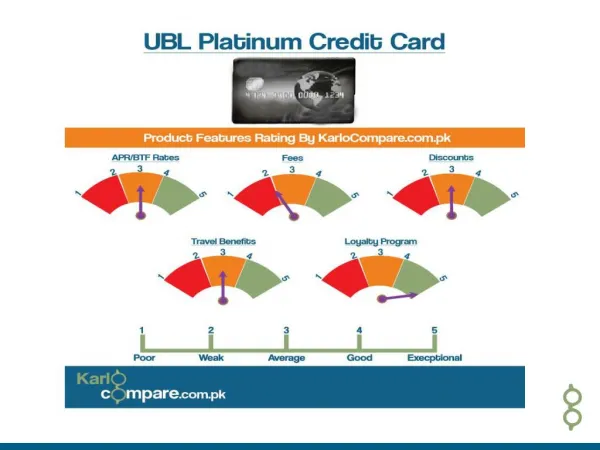

Through different documented transactions, financial statements depict a company's funding, investing, and operating operations. The financial statements were created domestically, so there is a high possibility that they were prepared fraudulently.<br><br>Without the right rules and guidelines, preparers can easily inflate the company's financial condition to make it seem more successful or prosperous than it actually is. IMPROVE CREDIBILITY IN FINANCIAL AUDITING WITH UBL

E N D

What Steps Comprise a Risk-Based Approach to Internal Audits? The typical approach to auditing is performing tests in order to make a determination regarding the accuracy of the business’s financial accounts. A risk-based audit, as opposed to a typical audit, is entirely focused on hazards. It is a technique that connects the internal auditing technique to the organization’s risk criteria. auditing consultancy dubai This approach to risk-based auditing not only establishes an organization’s risk profiles but also improves business efficiency and concentrates on the most important organizational requirements. With this particular approach, risks related to the company are managed while also being seen and evaluated as a whole. Internal auditors should address these issues and offer different recommendations to help people make wise decisions. The hazards that are most important should be dealt with and examined first. With this

strategy, the business goals and objectives are emphasized while a sound risk auditing strategy is maintained. In a case study, Greek banks implemented internal auditing practices based on the conventional auditing methodology. best auditing consultancy dubai After looking into several branches and accounts, it was determined that conventional internal auditing did not produce reliable results and did not adhere to the necessary risk coverage guidelines. A corporation should use the risk-based internal auditing method by carrying out the following procedures to prevent situations like these from occurring Understanding and identifying the risks is the first stage in the lengthy process of risk-based internal auditing. An auditor should be completely knowledgeable about the business environment and operations of the organization. The auditor must be knowledgeable about the company’s internal controls and the risk management strategy it employs. An analytical procedure that comprises appropriate observation,

examination, evaluation, and documentation of the company can be used to gather this information. Although the first and most crucial phase in the risk-based internal auditing technique can be a little tedious for the auditor. Phase 2: The following step is risk assessment, where the auditor assesses the organisational hazards related to the business. The auditor can identify the precise area of the business where the risk is greatest and can identify it by gaining information and having the necessary abilities. The auditor must comprehend the nature of the risks and their potential effects on the business after they have been assessed. As a revised plan may identify new risks related to the company, risk assessment is done while creating an internal audit strategy for the organisation. The auditor is supposed to utilise analytical skills and professional judgement while assessing and categorising risks to decide whether or not it is a high, medium, or low risk.

Phase 3: Conducting the risk-based audit is part of the third step. This step entails really auditing the internal elements that are predicated on risk. The audit plan is implemented right here when all the risk assessment procedures have been completed. All sections are subject to auditing, and a suitable framework for risk management is upheld. While places with lower hazards won’t require as much time, those with higher risks are given more time. They then write a report about the issues they found in light of their findings. Phase 4: Monitoring any changes to risks and taking action are part of the risk-based internal auditing approach’s final step. This auditing method needs the auditor to pay close attention and conduct careful monitoring. The company’s risks vary depending on the shifting demands and the organization’s shifting dynamic environment. As a result, it is the auditor’s duty to monitor any changes or variations that may take place when the risk-based internal auditing approach is being implemented. The internal auditor must

also follow up on the insights they gained from the audit and ensure that the vulnerabilities found are promptly fixed. For a corporation to be effective, using a risk-based internal auditing method has a number of advantages.