Download

1 / 4

40 likes | 45 Views

In the world of small business financing, the options are almost endless. One can take out a loan, apply for an equity investment or even use their own personal credit to fund the companyu2019s growth. Every business operates differently and has different needs.

E N D

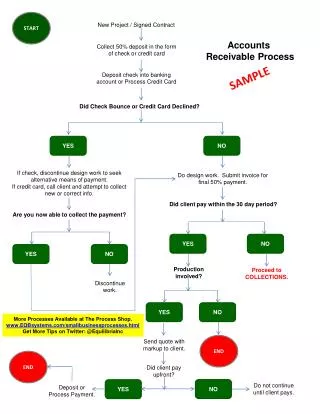

Accounts Receivable Financing: How It Works In the world of small business financing, the options are almost endless. One can take out a loan, apply for an equity investment or even use their own personal credit to fund the company’s growth. Every business operates differently and has different needs. Depending on the industry and the stage of growth of the business, one option may be more beneficial than another. However, while so many financing options exist, there is one that is often overlooked by small businesses: accounts receivable financing. Even though it’s a great way to get money fast and help manage cash flow, AR financing isn’t well known among businesses of all sizes. If one needs fast cash and has outstanding invoices from customers who are willing to make payment at a later date, they should be looking at accounts receivable financing. What is Accounts Receivable Financing? Accounts receivable financing (also called factoring) is a type of financing in which a company sells a customer’s outstanding invoices to a third-party lender. This is an effective way for small businesses to sell products or provide services and receive cash up front. The lender then collects the money owed from the customers at the agreed maturity date. In exchange for assuming the risk of nonpayment by your customers, the lender will charge a discount fee and give the funds upfront for the company to pay the bills and/or restock inventory. The amount received from the lender is based on the amount of the invoices minus the discount fee charged by the lender. The process of selling an outstanding invoice is typically referred to as an AR factoring or AR financing transaction. How AR Financing Works AR Financing enables companies to receive early payment for their outstanding invoices. For the small business owner, accounts

receivable financing is a great way to get cash quickly and easily to optimise your working capital cycle. Additionally, AR financing allows small suppliers to get access to cheaper financing compared to a bilateral bank loan when dealing with larger buyers, as the credit risk ultimately falls on the buyer as the payment obligor. But what happens if the buyer who owes money doesn’t pay on time? That’s where the risk factor of AR financing comes into play. The lender who purchases the invoices from the customers assumes the risk of nonpayment in doing so. That’s why the interest rates for this type of financing may even be higher than those for a traditional loan, if the buyer is a small business as well and assessed to have a higher credit risk. But even though there is a risk involved, AR financing is a great way to get cash quickly and help manage cash flow. It’s a good idea to do some research and find the right lender or provider who can give the terms that work best for one’s business. And one way to do that is to find a digital marketplace that connects businesses with lenders that offer AR financing. Why Should You Use AR Financing? •You can get cash fast – If your customers are paying on their own schedule, it might be hard to meet payroll and pay other bills. With AR financing, you can get the money you need to cover your expenses and keep your business running smoothly. •You don’t have to wait for customers to pay – You may have a ton of great customers who are happy with your products and services and are paying on time. But even if you have 100% payment rates, you still have to wait for customers to pay you. With an AR financing provider, you can get cash upfront for invoices you already have. •You don’t have to use your own money to finance growth – If you are financing your company’s growth with your own money, you may risk depleting your cash reserves. With an AR financing option, you can get the liquidity you need to optimise your cash flow.

•You can get more done with less stress –It’s easy to put off important tasks when you are stressed about cash flow. With the right financing option, you can get the cash you need and make better strategic decisions. •Your customers aren’t impacted – You might be considering using your personal credit or taking out a loan to fund your company’s growth. But those types of financing can impact your credit score and your relationship with your bank. AR financing isn’t a personal loan but a banking facility. It just gives your customers more time to pay their bills. Using a Marketplace to Find the Right AR Financing Partner It’s estimated that about $3 trillion in invoices are paid late every year. That’s nearly $5 billion in uncollected payments every day in the U.S. alone. Small business owners don’t have time to go after every bill that is late. Instead, they need to focus on growing their business. They, however, still need the cash. That’s where accounts receivable financing comes in. When one takes out an AR financing loan, they receive the funds upfront to pay bills and restock inventory. Next one just has to wait for the lender to pay. Researching online and finding a digital marketplace that connects businesses with lenders that offer AR financing is the first step. A marketplace can help one compare lenders. A digital marketplace generally will have financing partners to choose from, integrate modern algorithms and leverage data to mitigate risk and make the AR financing process smooth. The Drawback of Accounts Receivable Financing In the same way that taking out a loan has its drawbacks, so does accounts receivable financing. For starters, if a customer doesn’t pay their invoice, the lender may in some cases seek recourse to collect the money you initially received to pay it off. That means you may owe money you don’t have to pay the invoice off. That may seem like a huge drawback, but it’s also a reality.

It’s important to remember that even though AR financing is a great way to get cash and help manage your cash flow, you have to pay it back. Before you sign on the dotted line, make sure you find the right lender and that you have a good plan to pay that money back on time. With the right financing option, you can get the cash you need without putting added stress on your