Download

1 / 13

230 likes | 660 Views

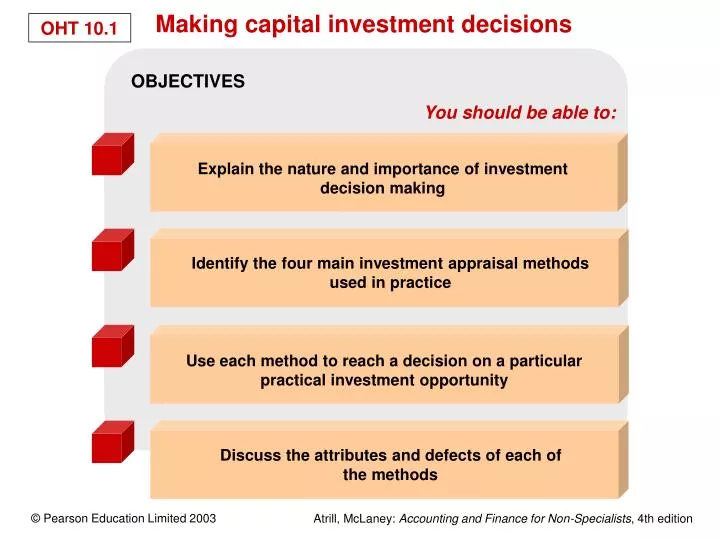

OBJECTIVES. You should be able to:. Explain the nature and importance of investment decision making. Identify the four main investment appraisal methods used in practice. Use each method to reach a decision on a particular practical investment opportunity.

E N D

OBJECTIVES You should be able to: Explain the nature and importance of investment decision making Identify the four main investment appraisal methods used in practice Use each method to reach a decision on a particular practical investment opportunity Discuss the attributes and defects of each of the methods Making capital investment decisions

Business Expenditure on additional fixed assets as a percentage of: Annual sales Start of year fixed assets Associated British Foods plc 10.1 28.6 The Boots Company plc 3.2 7.6 British Airways plc 9.3 7.0 BT plc 19.9 17.0 British Sky Broadcasting Group plc 5.0 20.1 J D Wetherspoon plc 25.1 24.1 Manchester United plc 27.5 20.5 Stagecoach Group plc 6.0 5.4 Tesco plc 8.5 20.1 Vodafone Group plc 79.4 11.8 Exhibit 10.1

Four methods of evaluation Accounting rate of return (ARR) Payback period (PP) Net present value (NPV) Internal rate of return (IRR) Methods of investment appraisal

x 100% Average annual profitAverage investment to earn that profit ARR = Accounting rate of return (ARR)

The payback period is the length of time it takes for the initial investment to be repaid out of the net cash inflows from the project. Payback period (PP) Payback period (PP)

Initial outlay Payback period Yr 1 Yr 2 Yr 3 Yr 5 Yr 4 Project 1 Yr 4 Yr 1 Y 2 Yr 3 Y1 Y4 Y 5 Project 2 Project 3 Yr 1 Yr 2 Yr 3 Yr 5 400 600 300 500 700 800 900 0 100 200 Cash flows (£000) The cumulative cash flows of each project in Activity 10.6

Discount rate Interest foregone Inflation Risk premium The factors influencing the discount rate to be applied to a project

1 3 4 5 6 8 9 10 0 2 7 Present value of £1 receivable at various times in the future, assuming an annual financing cost of 20 per cent £1 Years into the future

NPV fully addresses each of the following: The timing of the cash flows The whole of the relevant cash flows The objectives of the business Why NPV is superior to ARR and PP

The internal rate of return is the discount rate, which, when applied to the future cash flows of a project, will produce an NPV of precisely zero. Internal rate of return (IRR) Internal rate of return (IRR)

70 NPV (£000) 60 50 40 30 20 IRR 10 0 20 30 10 40 Rate of return (%) The relationship between the NPV and IRR methods

Some practical points Year-end assumption Relevant cash flows Opportunity costs Interest payments Other factors Taxation Cash flow not profit flow Dealing with questions relating to investment appraisal

Many surveys have tended to show: Businesses using more than one method to assess each investment decision An increased use of the discounting methods (NPV and IRR) over time Continued popularity of ARR and payback period A tendency for larger businesses to use the discounting methods and to use more than one method Investment appraisal in practice