Download

1 / 0

10 likes | 537 Views

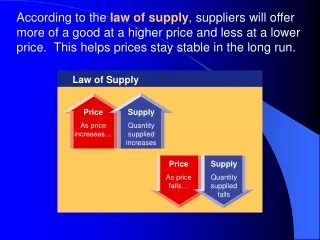

Law of Supply. Chapter Five. Law of Supply. http://www.youtube.com/watch?v=c9IwnbV0iow. Basic Definitions. Supply – The amount of goods available How do producers decide how much to supply? Law of Supply – Higher the price, the larger the quantity produced.

E N D