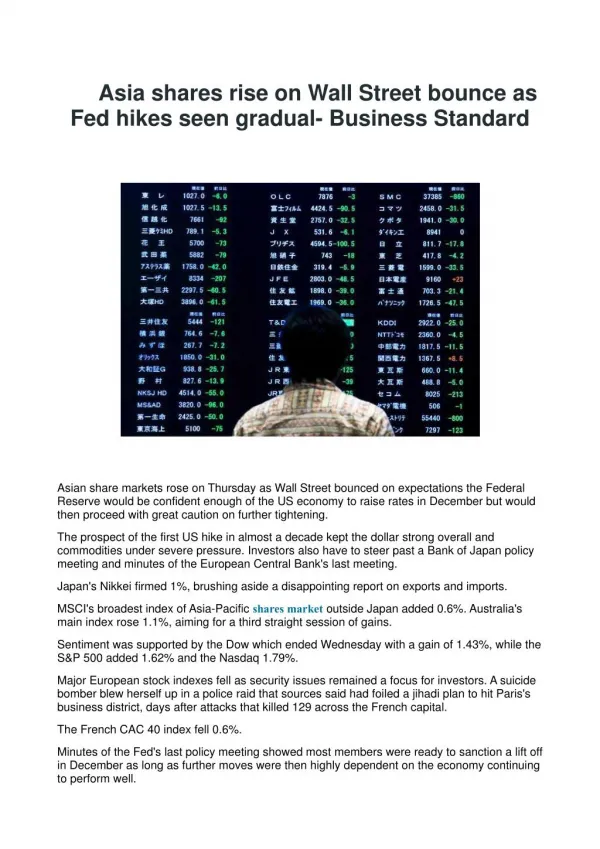

Download

1 / 11

110 likes | 230 Views

Stock Price Levels and Price Informativeness Konan Chan, Fengfei Li, Tse-Chun Lin, and Ji-Chai Lin Discussed by Tie Su University of Miami. Stock Price Levels and Informed Trading. High stock price levels: Impede informed trading Reduce price informativeness

E N D

Stock Price Levels and Price Informativeness Konan Chan, Fengfei Li, Tse-Chun Lin, and Ji-Chai Lin Discussed by Tie Su University of Miami 2012 NTUICF Conference

Stock Price Levels and Informed Trading • High stock price levels: • Impede informed trading • Reduce price informativeness • Make listed options more appealing • O/S goes up • Stock splits: • Lower stock prices • Improve informed trading • Enhance price informativeness • O/S goes down Stock price levels matter in trading! 2012 NTUICF Conference

Motivation • Nominal share price puzzle: markets have maintained a price level around $35 since the Great Depression. • Liquidity is important. • Uninformed trading is needed for informed trading to work. • Budget constraints prevents uninformed (liquidity) traders from diversifying their portfolios in high price stocks. • Informed trades gravitate to options markets to conduct trading. • O/S levels are high for high price stocks. • O/S increases with stock price levels and that this positive relation is stronger for firms that have more difficulty in attracting small investors as shareholders Stock price levels do matter in valuation and trading! 2012 NTUICF Conference

Hypotheses • H1: High stock price levels would impede informed trading on the stocks, reduce price informativeness, and make listed options more appealing to the informed because uninformed trading is needed for market making and high stock price levels may impose budget constraints on uninformed traders and limit their risk sharing capacity. • H2: For firms whose high stock price levels hinder uninformed traders to enter the market, managers can use stock splits to attract more uninformed traders to improve informed trading and enhance informational efficiency of stock prices. 2012 NTUICF Conference

Comments • VERY interesting paper: it paper examines impact of the level of stock prices on trading, a topic that has not yet been studied in literature. • Carefully executed in all estimation procedures. • Well and clearly written, a pleasure to read. • I have learned A LOT from this paper. I recommend the paper to everyone. 2012 NTUICF Conference

Comments: O/S • O/S = relative trading of option over stock, measured in # of shares and dollar trading volume. It is a measure of informed trading. • Figure 1: other factors that may lead to elevated level of O/S: speculation of split announcements, which may not be correlated with informed trading. 2012 NTUICF Conference

Comments: O/S 2012 NTUICF Conference

Comments: Stock Splits • The authors provide an important alternative benefit of stock splits. • Not all stock splits are executed when stock prices are very high. Do we have empirical evidence to support the hypothesis that the higher the stock price prior to a stock split, the larger the benefit of a stock split? • How does the size of the benefit vary over time, in bull/bear markets? 2012 NTUICF Conference

Comments: Price levels • Across firms: $0.88 - $741.79, mean = $32.01 • Across firm means: $11.37 - $52.76, mean = $26.05 • Intuitively, the means of firm prices are NOT high enough to impede informed trading and to produce high levels of O/S. Have the authors considered time series properties of O/S of the same firm, as firm’s stock price increases over time. It may be of particular interest if the firm experience stock splits in the horizon. 2012 NTUICF Conference

Other Comments • Interpretation of variable “small” is unclear. • Small is a dummy variable which equals 1 if dollar ownership per shareholder, defined as the firm size divided by the number of common/ordinary shareholders from Compustat, is greater than the cross-sectional median, and zero elsewhere. • Any alternative measure of “price informativeness”? • We follow Gelb and Zarowin (2002), who “define price informativeness by the association between current stock returns and future earnings changes: more informative stock price changes contain more information about future earnings changes.” 2012 NTUICF Conference

A great paper.I enjoyed reading it. 2012 NTUICF Conference