Download

1 / 7

80 likes | 91 Views

The Price System. Chapter 21.4 Questions, Activities and Graphing Exercises. Setting Prices. Producers want high prices. Consumers want low prices. Prices must be high enough to make a profit and low enough to attract consumers. Shortages cause prices to increase. D>S

E N D

The Price System Chapter 21.4Questions, Activities and Graphing Exercises

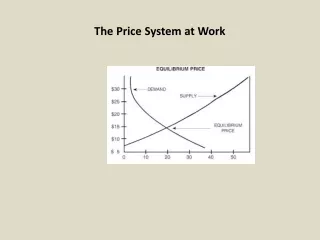

Setting Prices • Producers want high prices. • Consumers want low prices. • Prices must be high enough to make a profit and low enough to attract consumers. • Shortages cause prices to increase. D>S • Surpluses cause prices to decrease. D<S • Where producers and consumers wants intersect is how prices & quantity are determined. This is called the equilibrium point. This point determines the EP & EQ.

Price Schedule Quantity (liters) demanded/week 120 95 75 60 50 Price per liter $1.20 $1.30 $1.50 $1.75 $2.15 Price per literQuantity (liters) supplied/week $1.20 50 $1.30 60 $1.50 75 $1.75 95 $2.15 120 EP 0 EQ

Setting Prices • Price ceilings are limits on how much producers can charge for a good or service. These are VERY rare in our economy. Ex. Is rent controls in NYC • Price floors are limits on how little businesses can charge for a good or service. Ex are farm prices kept low by subsidies. Another example is minimum wage. • Consumers & producers largely determine prices in US economy. However, there is gov’t rules so we’re a mixed market economy.

Setting Prices • What are the advantages of our price system in Capitalism? • Prices are neutral…What does a “buyer’s market” mean? • Prices are flexible…Give an example of how prices may flex. • Prices offer choice…How many choices do you have for shoes? • Prices are familiar…Why is inflation bad for consumers?

Practice • Discuss the graph at the bottom of p. 74. • Graph the schedules on p. 75 & label all parts correctly. • Label all 10 points! • Discuss & peer score • Demonstrate each graph and check information. • Complete the scenarios with your elbow partner. Discuss as a group.

Assignment • Read 23 & selected pages to complete questions for p. 76. • Due Tomorrow!