Download

1 / 27

270 likes | 435 Views

Final Conference Revenue Use from Transport Pricing Brussels 29- 30 November. POLICY CONCLUSIONS FROM THE REVENUE PROJECT. CARLO SESSA (ISIS). OBJECTIVES. Identify the most effective options for utilising the revenues arising from transport pricing. METHOD.

E N D

Final Conference Revenue Use from Transport Pricing Brussels 29- 30 November POLICY CONCLUSIONS FROM THE REVENUE PROJECT CARLO SESSA (ISIS)

OBJECTIVES Identify the most effective options for utilising the revenues arising from transport pricing

METHOD Distillate the policy conclusions and recommendations from consolidating and summarising the findings of work-packages 1-5

OUTPUT Concrete and practical guidelines on the topic, to be disseminated to policy makers and stakeholders (Deliverable 6)

PLANNING OF DELIVERABLE 6 0. Executive Summary 1. Introduction: what are the research questions raised in D1 2. Methodological framework for the assessment of alternative uses of revenue regulation schemes using D2 3. Case study results for interurban transport using Deliverable 4 4. Regulation schemes in urban transport using Deliverable 5 5. Overview of current and potential practice in pricing and revenue use in Europe and confrontation with the results of the case studies : using Deliverable 3 6. Policy conclusions and recommendations

KEY ISSUES • Cost Benefit Analysis of the pricing schemes • (welfare impacts) • Clear understanding of the revenue flows • (current and potential changes) • Interaction between 1 and 2 • Acceptability of the pricing and revenue • recycling strategies

WELFARE IMPACTS: Key Questions • Are the welfare impacts really significant ? • To what extent the results are constrained • by the methodology, assumptions, input data • used ? • To what extent the case study findings can • be generalised ?

REVENUE STRATEGIES: Key Questions • Are the case studies showing clear options • for revenue recycling ? • Is it clear who should pay to whom for what • (e.g. implications for different levels of • government, taxes and subsidies) ? • To what extent the different revenue • recycling strategies influence the welfare • impact ?

ACCEPTABILITY: Key Questions • What are the lessons learned about the • acceptability of the pricing schemes ? • Who are the actors involved (stakeholders, • citizens) ? • Is a clear understanding of the consequence of • transport pricing and revenue recycling • strategies for the people welfare enough to • enhance acceptability ?

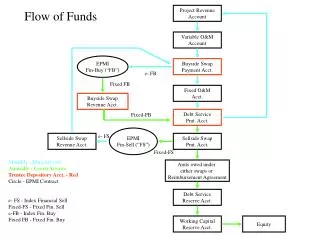

COMPREHENSIVE FRAMEWORKTO BENCHMARK REVENUE RECYCLING STRATEGIES Why we need a comprehensive framework to illustrate the case study findings ? Example of Zurich airport case study We do not need to invent a new conceptual framework, we already have it ! Transport accounting

USING A REVENUE ALLOCATION METADATA FRAMEWORK TO BENCHMARK REVENUE RECYCLING STRATEGIES REVENUE CASE STUDIES Common framework to benchmark revenue recycling strategies Analysis of pricing and revenue recycling (regulation schemes) NAT NATIONAL TRANSPORT ACCOUNTING METADATA INTERNALISATION Environmental themes/indicators INTEGRATION OF EXTERNALITIES ACCOUNTS (NAMEA approach) - “NATEA” METADATA - VALUATION OF EXTERNALITIES

WHY TO USE NATIONAL ACCOUNTING CONCEPTS ? • The System of National Accounts (SNA) records economic flows and stocks of a country, allowing • to answer systematically to the question: • WHO DOES WHAT BY WHAT MEANS FOR WHAT PURPOSE WITH WHOM • IN EXCHANGE FOR WHAT WITH WHAT CHANGES IN STOCK ? The SNA does not attempt to determine the utility of the flows and stocks which come within its scope (neutrality in relation to the welfare impacts of the regulation schemes investigated in the REVENUE case studies) The SNA can be adapted to improve the representation of economic flows and stocks related to all transport activities (recording commercial and own-account transport in Transport Satellite Accounts) The SNA doesn’t include externalities within its scope, but extended accounts (NAMEA) include external impacts denominated in physical units

OVERVIEW OF NATIONAL ACCOUNTING METADATA SEQUENCE OF ACCOUNTS: production accounts, distribution and use of income, accumulation accounts INSTITUTIONAL SECTORS: non-financial corporations, financial corporations government units, non-profit institutions serving households, households • SYSTEM OF NATIONAL ACCOUNTS (SNA) PRODUCTION BOUNDARY: • - Includes market output, non-market output, own-account output for fixed capital formation • of producers • Includes households’ productions of goods for own final consumption, dwelling services, • domestic services produced by employed staff • - Does not include “do-it-yourselves” households’ activities (including car driving)

OVERVIEW OF NATIONAL ACCOUNTING METADATA NEEDS FOR ADAPTATIONS: Transport activities undertaken by households are not included in the production boundary The production of transport for own use within an enterprises is an ancillary activity that is not separately identified and recorded. Therefore, costs of in-house transport – fuels and vehicle costs, drivers’ wages etc – are embedded in the accounts of various industries other than the transport service sector Part of the operation of the transport system is undertaken by non-market producers – i.e. government units – in the form of collective services, such as: cleaning, maintenance and repair of public roads, bridge, tunnels; provision of street lighting. The output of non-market transport is included in the System, but being treated as collective service provided free to households and enterprise, it is difficult to separate its contribution to intermediate and final consumption.

OVERVIEW OF NATIONAL ACCOUNTING METADATA Full accounting of transport activities NAT’S INNOVATIONS: To expand the production boundary of the System including the usage of private cars for work trips, as additional output produced for own final consumption by households To estimate the amount of in-house transport undertaken by enterprises as ancillary activity in the various sectors of the economy, and to form a separate virtual “in-house” transport sector, extracting the ancillary transport related costs from all other sectors of the economy To show transport non-market services separately from other non-market goods and services provided by government units and NIPSHs, and to estimate the consumption of transport collective goods and services (e.g. the use of road infrastructure) by households and by enterprises

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items PRODUCTION ACCOUNT: Market output of the transport services rendered to third parties: - Land transport: road, rail, pipelines - Water transport: sea, inland waterways - Air transport - Auxiliary transport services Non-market transport activities typically include: - Provision of road infrastructure by the State (national roads), provinces (provincial roads and local authorities (urban road); their maintenance and cleaning activities - Provision of port infrastructure, lighthouses; their operation and maintenance - Provision of inland channel and river port infrastructure; their operation and maintenance activities - Air control services - Minor services such as provision of street lighting, shool bus services, etc.

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items PRODUCTION ACCOUNT: • Output produced for own final use: this category shall include as new transport related • items: • Output for own final consumption of transport of members of the household or their • their goods, undertaken with households own vehicles: cars, mopeds, bicycles (as a • result of the extension of the production boundary to include this activity and limited • to work related journeys • Output for own intermediate consumption of transport of goods and persons undertaken • by any kind of enterprise – including market and non-market producers – as ancillary • activity

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items PRODUCTION ACCOUNT: • Intermediate consumption of transport services includes various items for different modes: • Road freight transport services • Own account road freight transport (ancillary activity not recorded separately in the standard SNA; • to be estimated and included in a separate in-house transport sector of the NAT) • Road passenger transport services • Own-account road passenger transport (ancillary activity, see above) • Highways’ services • Road infrastructure use costs (these included in the government collective services in the standard • SNA; the portion of these costs due to enterprises’ use of the road shall be estimated and included • as intermediate consumption in the NAT) • Rail freight transport services • Rail passenger transport services • Rail infrastructure charges • Urban Public Transport services • Air passenger services • Air freight services • Airport infrastructure charges • Air control charges • Sea freight transport • Port warehouse services • Port infrastructure charges • Inland freight transport • Inland waterways charges

OVERVIEW OF NATIONAL ACCOUNTING METADATATransport accounting items PRODUCTION ACCOUNT: • Consumption of fixed capital assets: • Transport infrastructure • Transport vehicles (including part of households’ vehicles) • Value added from: • Transport services to third parties • Own-account transport of market and non-market producers • Non-market transport activities (mainly labour costs) • Household “production” for own final consumption of private transport services normally • should not include a value added component

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items PRIMARY DISTRIBUTION OF INCOME ACCOUNT: Taxes on products: VAT on transport services, fuel taxes, taxes on specific transport services Other taxes on production: taxes levied periodically on the use of vehicles, ships, aircraft in the production of transport services Business and professional licenses, to the extent that these are applied on transport operation (e.g. taxi services) Taxes on pollution caused by transport activities Subsidies on products: subsidies to urban public transport operators; State subsidies to rail infrastructure undertakings; State subsidies for rail passenger transport; Stare subsidies for rail freight transport; subsidies to maritime transport; subsidies to inland water operators. Subsidies on production: State, regional or local authorities subsidies to the operation of environmetally friendly vehicles

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items SECONDARY DISTRIBUTION OF INCOME ACCOUNT: Other current taxes: vehicle taxes; with the extension of the production boundary to include the use of households’ vehicles to travel to and from work, a quota of the vehicles taxes shall be transferred to taxes on production Social insurance benefits: these are specifically relevant to transport to the extent that the social benefits include the coverage of health or production loss damages caused by transport accidents Other current transfers include various items that can be related to transport: non-life insurance premiums and claims: they allow to internalise part of road accident costs current transfers within general government: in several countries funds for financing public transport operation costs (urban public transport, rail infrastructure) are constituted at national or regional level, out of general taxation, and then transferred for the State or regional government to the regional or local authorities in charge of the public transport services. These transfers are then used to subsidise public transport operators Miscellaneous current transfers: in some countries enterprises (e.g. France) enterprises are required to finance directly urban transport operators; fines for illegal parking or driving; payments of compensations to internalise damages caused by accidents or other transport externalities not covered by non-life insurance schemes

OVERVIEW OF NATIONAL ACCOUNTING METADATATransport accounting items REDISTRIBUTION OF INCOME IN KIND ACCOUNT: Social transfers in kind: A form of social transfer in kind related to transport is the provision of transport services – usually urban transport services and rail transport – at a reduced tariff to specific categories of households or persons (elderly, students etc.). When these services are provided by transport operators, usually their loss of revenue is covered by specific government subsidies, that should be recorded separately from those covering the normal operating deficits

OVERVIEW OF NATIONAL ACCOUNTING METADATATransport accounting items USE OF INCOME ACCOUNT: • Household road transport final consumption expenditure (COICOP): • Purchase of motor cars • Purchase of motor cycles • Purchase of bicycles • Spare parts and accessories • Fuels and lubricants • Maintenance and repair • Other services in respect of personal transport equipment (include also parking fees) • Passenger transport by road (bus, coach, taxi and hired car, without distrinction between • urban and interurban transport) • Insurance connected with transport • Actual and imputed rentals for the use of parking garages in connection with dwellings • (merged with other actual and imputed rentals for housing) In the NAT system: - divide consumption of passenger road transport services into urban and interurban - estimate transport to and from work and move it within the production boundary: part of vehicle purchase to fixed capital formation; part of spare parts, fuels, maintenance and repair, parking fees etc. to intermediate consumption

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items USE OF INCOME ACCOUNT: • Household rail transport final consumption expenditure: • Passenger transport by railway: both urban and interurban • In the NAT system this shall be divided into urban (to be included in urban public transport) • and interurban • Household final consumption expenditure on other transport modes: • Passenger transport by air • Passenger transport by sea and inland waterways • In the NAT system sea and inland waterways passenger trasport shall be separated

OVERVIEW OF NATIONAL ACCOUNTING METADATATransport accounting items USE OF INCOME ACCOUNT: Collective services: • Road maintenance and cleaning • Ports and lighthouses operation and maintenance • Inland channels and river ports operation and maintenance • Air control services • Minor services such as the provision of street lighting, school bus services If detailed data are available, any receipts from sales of non-market services, such as road pricing whose importance is now growing, shall be subtracted from the collective service value and allocated to final consumption and intermediate consumption, according to the amounts of user charges paid by households and enterprises

OVERVIEW OF NATIONAL ACCOUNTING METADATA Transport accounting items CAPITAL ACCOUNT: • Gross fixed capital formation shall include the value of the following fixed assets: • Transport infrastructure: highways, national and local roads, bridges, tunnels, railway tracks • railways stations, port infrastructures, airport infrastructures, inland waterway infrastructures; • Vehicle stocks: cars, buses, coaches, trams, rail rolling stocks, vessels etc. • Other transport related equipment and structures, such as parking lots in connection with • company premises • Capital transfers: • Investment grants from national or regional funds, to finance the construction of large transport • infrastructures, renovation of vehicle fleets, etc. • Capital endowment of national or local transport operators subscribed by State or local governments • State reimbursement of debt services of major transport undertakings

OVERVIEW OF NATIONAL ACCOUNTING METADATA WHY EXTERNALITIES ARE EXCLUDED ? • technical difficulties to associate economically meaningful values with externalities, but, • more substantially …. • they are not market transactions into which institutional units enter of their own accord, • there is no mechanism to ensure that the positive or negative values attached to externalities • by the various parties involved would be mutually consistent, and … • accounts including values for externalities could not be interpreted as representing equilibrium, • or economically sustainable, situations. If such values were to be replaced by actual payments • the economic behaviour of the units involved would change • therefore, valuation of externalities might be included only if a full modelling and scenario • analysis is undertaken, showing the impacts of internalisation of externalities via pricing • and revenue recycling strategies