Download

1 / 15

160 likes | 418 Views

Chapter 28. The Theory of Active Portfolio Management. Lure of Active Management. Are markets totally efficient? Some managers outperform the market for extended periods While the abnormal performance may not be too large, it is too large to be attributed solely to noise

E N D

Chapter 28 The Theory ofActive PortfolioManagement 28-1

Lure of Active Management Are markets totally efficient? • Some managers outperform the market for extended periods • While the abnormal performance may not be too large, it is too large to be attributed solely to noise • Evidence of anomalies such as the turn of the year exist The evidence suggests that there is some role for active management 28-2

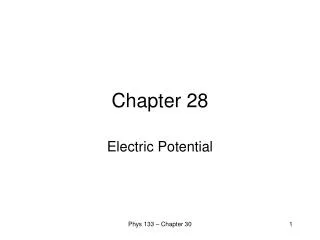

Market Timing • Adjust the portfolio for movements in the market • Shift between stocks and money market instruments or bonds • Results: higher returns, lower risk (downside is eliminated) • With perfect ability to forecast behaves like an option 28-3

rf rM rf Rate of Return of a Perfect Market Timer 28-4

Returns from 1987 - 1996 Year Lg. Stock Return T-Bill Return 87 5.34 5.50 88 16.86 6.44 89 31.34 8.32 90 -3.20 7.86 91 30.66 5.65 92 7.71 3.54 93 9.87 2.97 94 1.29 3.91 95 37.71 5.58 96 23.00 5.20 Average 16.06 Standard Dev. 14.05 28-5

With Perfect Forecasting Ability • Switch to T-Bills in 87, 90 and 94 • No negative returns or losses • Average Ret. = 17.44% • S.D. Ret. = 12.38% • Results with perfect timing • Increase in mean return • Lower S.D. 28-6

With Imperfect Ability to Forecast • Long horizon to judge the ability • Judge proportions of correct calls • Bull markets and bear market calls 28-7

Superior Selection Ability • Concentrate funds in undervalued stocks or undervalued sectors or industries • Balance funds in an active portfolio and in a passive portfolio • Active selection will mean some unsystematic risk 28-8

Treynor-Black Model • Model used to combine actively managed stocks with a passively managed portfolio • Using a reward-to-risk measure that is similar to the the Sharpe Measure, the optimal combination of active and passive portfolios can be determined 28-9

Treynor-Black Model: Assumptions • Analysts will have a limited ability to find a select number of undervalued securities • Portfolio managers can estimate the expected return and risk, and the abnormal performance for the actively-managed portfolio • Portfolio managers can estimate the expected risk and return parameters for a broad market (passively managed) portfolio 28-10

Passive Portfolio : E ( r ) - r 2 m f 2 S = [ ] m m Reward to Variability Measures 28-11

Reward to Variability Measures Appraisal Ratio: A (eA) = Alpha for the active portfolio A = Unsystematic standard deviation for active (eA) 28-12

( r r m Reward to Variability Measures Combined Portfolio : E ) - 2 2 m f 2 S = [ ] + ] A [ p eA 28-13

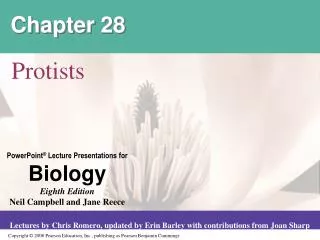

Treynor-Black Allocation CAL E(r) CML P A M Rf 28-14

Summary Points: Treynor-Black Model • Sharpe Measure will increase with added ability to pick stocks • Slope of CAL>CML (rp-rf)/p > (rm-rf)/p • P is the portfolio that combines the passively managed portfolio with the actively managed portfolio • The combined efficient frontier has a higher return for the same level of risk 28-15