Download

1 / 31

310 likes | 546 Views

Managing Investment and idiosyncratic longevity risks for retirees. Michael S. Finke, Ph.D., CFP ® Professor & Director Retirement Planning & Living Department of Personal Financial Planning Texas Tech University. Congratulations!. You’re a pension manager!. Pension Managers.

E N D

Managing Investment and idiosyncratic longevity risks for retirees • Michael S. Finke, Ph.D., CFP® • Professor & • Director Retirement Planning & Living • Department of Personal Financial Planning • Texas Tech University

Congratulations! You’re a pension manager!

Pension Managers What do they worry most about? 1) Asset Return Risk 2) Longevity Risk

Individual Pensions are Harder • Asset Return • Pension Manager – Pool returns across generations • Advisor – One whack at the cat • Longevity Risk • Pension Manager – systemic increases in longevity • Advisor – Idiosyncratic longevity risk

Systematic Longevity Risk Source: Robine, 2012

Wealthier Live Longer Source: SSA, 2008

Idiosyncratic Longevity Risk Source: Frank, 2013

Idiosyncratic Longevity Risk • How do you deal with idiosyncratic risk? 1) Diversification (pool it) 2) Retain it • Avoiding running out of money by spending less and accepting portfolio risk • Live it up and accept greater risk of running out of money

The 4% Rule (William Bengen, 1994) • Safe Withdrawal Rates (1920s - present)

Philosophy of the 4% Rule • Retirees have a lifestyle goal and not meeting that goal indicates failure • Failure = inability to spend lifestyle goal for 30 years • Portfolio risk increases likelihood of meeting spending goal • Use prior returns to establish safe withdrawal rate

Historical Random Returns 8.99% -10.1% 3.0% 13.7% 23.5% -38.5% 31.0% 20.3% 34.1% -1.5% 7.1% 4.5% 26.3% -6.6% 27.3% 12.4%

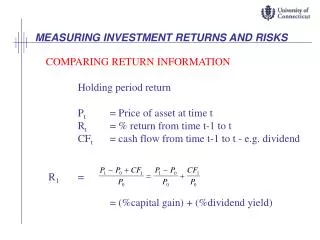

Asset Pricing 101 pt = Εt[β * u’(ct+1)/u’(ct) * xt+1] Price at time t (now) = Expectation (now) Of β(how much we discount the future) * Marginal utility tomorrow Marginal utility today *Expected payout tomorrow

What’s Affecting Asset Prices? How Much Do Global Investors Value the Future?

Importance of 1st Decade Source: Milevsky and Abaimova, 2005

Monte Carlo Failure Rates • Historical Real Returns: Stocks 8.6%, Bonds 2.6% Stock Allocation: 30%50%70% Failure Rates 6% 6% 6% • Slightly more realistic: Stocks 5.5%, Bonds 1.75% Failure Rates 24% 24% 27% • A little better than today’s rates: Stocks 6%, Bonds 0% Failure Rates 47% 33% 28% • Early 2013 Rates: Stocks 4.6%, Bonds -1.4% Failure Rates 77% 57% 46% Source: Blanchett, Finke and Pfau, 2013

What if Rates Revert in 5 Years? • Start out at current rates (Stocks 4.6%, Bonds -1.4%) • Revert to Stocks 8.6%, Bonds 2.6% Stock Allocation: 30%50%70% Failure Rates22% 18% 18% • What if Rates Revert after 10 years? Failure Rates43% 32% 38%

Other Problems with the 4% Rule Source: Blanchett and Finke, 1% fee

No Risk Tolerance, No Optimization Source: Finke, Pfau and Williams, 2011

Value of a Dynamic Approach Source: Blanchett, 2013

Illustration of Dynamic Source: Pfau, 2013

What Does Current P/E Imply? Source: Asness, 2012

A Better Approach • Prioritize spending categories (basic needs, discretionary expenses, legacy) • Employ risk when a retiree is willing to accept possibility of a loss • Deal efficiently with idiosyncratic risk • Simplicity - make sure real people can handle it, use research to create defaults • Be realistic about future asset returns

Questions/Comments • Michael S. Finke, Ph.D., CFP® • Professor, Ph.D. Program Director • Director Retirement Planning and Living • Department of Personal Financial Planning • Texas Tech University • Michael.Finke@ttu.edu