Download

1 / 39

390 likes | 399 Views

Administration of Alternative Investments in Fiduciary Accounts. FIRMA 25th Annual Risk Management Training Conference April 18, 2011 Suzanne L. Shier Chapman and Cutler LLP Chicago, Illinois 312-845-2983 shier@chapman.com. 2974368. Overview.

E N D

Administration of Alternative Investments in Fiduciary Accounts FIRMA 25th Annual Risk Management Training Conference April 18, 2011 Suzanne L. Shier Chapman and Cutler LLP Chicago, Illinois 312-845-2983 shier@chapman.com 2974368

Overview • Types of Non-Traditional Investments – Hedge Funds, Private Equity, Real Estate, Etc. • Prudent Investor Rule and Non-Traditional Investments • Use of Non-Traditional Investments - Diversification and Enhanced Returns • PWG Best Practices Guidance • Authority to Invest in Non-Traditional Investments • Legal Structure of Alternative Investments • Qualification to Make Alternative Investments • Dodd-Frank Volcker Rule • Valuation of Alternative Investments • Fiduciary Accounting • Fiduciary Administration

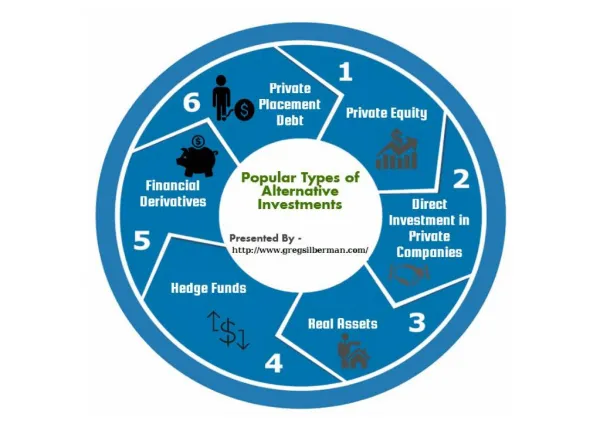

I. Introduction • “Traditional” investment in cash, cash equivalents, fixed income and equities • Expanded fiduciary investment in “non-traditional” investments • Hedge funds and funds-of-funds • Private equity • Real estate • Commodities • Pensions funds • 40% of large pension funds invest in private equity and approximately 25% invest in hedge funds • Private trust investment in non-traditional assets

Alternatives Bonds U.S. Equities Foreign Investments

II. Background - Hedge Funds • Increase in number of funds 3,000 ($200 billion) in 1998 to 9,000 ($2 trillion) peak in 2007; 25% decrease by end of 2008 with numerous fund collapses • Not an asset class; employ specific investment strategies to “hedge” against particular risk (e.g., interest rate, currency prices) • Not marketed to the general public; not publicly traded • Investors limited to high net worth individuals and institutions • Not regulated or registered • Managed by professional managers compensated based on performance • Periodic but restricted or limited investor redemption rights

II. Background - Private Equity • Increase in capital raised from $2 billion in 1980 to $207 billion peak in 2007 and increase in number of funds from 56 to 432 • Privately managed investment pools making long-term investments in private companies • Take a controlling interest in company with aim of increasing value • Investment made at various stages of existence of company • Start-up – venture capital • Intermediate – transition from start-up • Mature company – restructuring

III. Prudent Investor - General Rule • Rule for Trustees, not Guardians, Executors or Investment Managers • Duty to invest and manage as a prudent investor in light of – • Purpose and terms of the trust • Distribution requirements and other circumstances of the trust • Requires exercise of reasonable care, skill and caution • Applied to investments in the context of the trust portfolio as a whole as a part of an overall investment strategy rather than in isolation • Incorporate risk and return reasonably suitable to the trust

III. Prudent Investor - General Rule (Cont’d.) • Trustee has a duty to - • Diversity the investments of the trust, unless under the circumstances it is prudent not to do so (e.g., issues with concentrations) • Conform to the duties of loyalty and impartiality • Act with prudence in deciding whether and how to delegate • Incur only costs that are reasonable in amount and appropriate to the investment responsibilities • No particular investment is per se imprudent • Review investments in the context of the trust portfolio • Process is key

III. Prudent Investor – Non-Traditional Assets • Duty of caution and risk management • Risk tolerance varies from trust-to-trust and from time-to-time • Use of non-traditional investments to manage risks • Duty to diversify • Use of non-traditional assets whose returns are not correlated to particular traditional assets • Real estate limited covariance with publicly traded securities; inflation hedge • Duty to manage costs • Use of non-traditional assets may incur substantial costs • Investment review; legal review; managers’ fees

III. Prudent Investor – Non-Traditional Assets (Cont’d.) • Delegation • Expert assistance may be required with non-traditional assets • Engage investment managers with specific expertise • Use of pooled investment vehicles – “fund-of-funds” • Restatement Third, Trusts §90 • “Delegation” to manager of the fund • Investment in the fund itself rather than the underlying assets of the fund • Trustee controls the decision to invest in the fund

III. Prudent Investor – Non-Traditional Assets (Cont’d.) • Delegation – State law • Reasonable care, skill and caution in – • Selecting the agent • Establishing the scope and terms of the delegation • Periodically reviewing the agent’s actions to monitor overall performance and compliance with scope and terms of delegation • Due diligence regarding experience, performance history, licensing • Subject to jurisdiction Illinois courts (consider binding arbitration provisions) • Investment agent liable to beneficiaries • Advance written notice to current income beneficiaries

III. Prudent Investment – Restatement Third, Trusts Non-traditional Investments • Real Estate • Enhance diversification due to limited covariance with publicly traded securities • Long-term protection against inflation • Potential to augment income productivity or capital appreciation • Consider complexities of administrative burdens • Venture Capital (Private Equity) • Historically not an appropriate investment • 1979 DOL guidance “riskier” assets such as venture capital • Requires special due diligence and monitoring; use of funds not a substitute

III. Prudent Investment - Statutory and Judicial Guidance Non-Traditional Investments • Washington Probate Code • Authorizes investment in “new, unproven, untried” enterprises with a potential for significant growth directly or through commingled funds • Aggregate amount of investment, valued at cost, may not exceed 10% of the net fair market value of the trust corpus • Value for purposes of 10% limitation determined at the time the investment is made

III. Prudent Investment - Statutory and Judicial Guidance Non-Traditional Investments (Cont’d.) • Harley v. Minnesota Mining and Manufacturing Co. (ERISA), 42 F. Supp. 2d 898 (1999) • Investment in hedge fund holding collateralized mortgage obligations • Failure to conduct sufficient investigation and to seek independent advice • IBEW-NECA Southwestern Health & Benefit Trust Fund v. EMG Advisors, Inc. (ERISA), 172 F.3d 876 (1999)* • Investment in complex derivatives • Failure to conduct thorough and independent investigation

III. Prudent Investment - Statutory and Judicial Guidance Non-Traditional Investments (Cont’d.) • Laborers National Pension Fund v. Northern Trust Quantitative Advisors, Inc. (ERISA), 173 F.3d 313 (1999)* • Investment in interest-only mortgage backed securities • Investment was made as a hedge against countervailing risks in the portfolio, and appropriate consideration given and analysis done of characteristics and projected performance of the investment • Brane v. Roth, 590 N.E.2d 587 (1992)* • Investment in hedge funds • Breach of fiduciary duty in retaining inexperienced manager and in failing to attain sufficient knowledge to properly supervise the manager

III. Prudent Investment - Statutory and Regulatory Guidance Non-Traditional Investments (Cont’d.) • Levy v. Bessemer Trust Company, N.A., 1997 US Dist LEXIS 11056, 1997 US Dist. LEXIS 4045* • Claims for breach of contract, breach of fiduciary duty, and breach of duty to supervise (among others) with respect to failure to purchase collars to manage risk for concentrated investment in an investment management account

IV. Diversification and Enhanced Returns – Hedge Funds • Objectives • Lessen volatility • Enhance returns by investments not correlated to other investments • Challenges • Active management based on skill of manager (and manager may change) • Use of leverage to enhance returns; not regulated as in mutual funds • Fees – As high as 2% AUM and 20% of profits • Lack of transparency – valuation • Liquidity – lock-up periods and gates

IV. Objectives and Challenges – Private Equity • Objective – attain superior returns • Challenges • Increased risk/volatility • Concentration in limited number of companies in a single sector • Use of leverage in venture capital and limited track record • Competitive pressures in strong market resulting in overpayment • Long-term commitment and valuation

V. Best Practices - Hedge Funds • GAO Report to Congressional Requesters, Defined Benefit Plans - Guidance Needed to Better Inform Plans of the Challenges and Risk of Investing in Hedge Funds and Private Equity, GAO-08-692 (August 2008) • President’s Working Group on Financial Market, Best Practices for the Hedge Fund Industry (January 2009) • www.amaicmte.org

VI. Authority under Governing Instrument – Non-traditional Assets • Language of governing instrument controls • Prudent investment – non-traditional assets not prohibited per se; question of whether appropriate to the trust • Specific authorization is ideal • Specific limitations should be adhered to (e.g., margin transactions) • Consider amendment of revocable instruments and non-judicial settlement agreements for irrevocable instruments if authority a question • For corporate fiduciary considering investment in proprietary funds assess conflicts of interest

VII. Legal Structure of Alternative Investments • Organized as limited partnerships and limited liability companies • Governed by Delaware partnership and corporate law, not trust law • Broader investment authority • Reduced standards for liability • Document review • Operating memorandum/private placement memorandum • Entity operating agreement • Subscription agreement • Side letters and legal opinions

VII. Legal Structure of Alternative Investments (Cont’d.) • Appendix A – Summary of Delaware Limited Partnership Act • Appendix B – Comparison of Common Terms of Private Equity and Hedge Funds • Appendix C – Model Hedge Fund Due Diligence Questionnaire

VII. Legal Structure of Alternative Investment – Key Questions • Purpose of fund • Investor’s liability • Capital contributions not in excess of specified capital commitment • Distribution refunding obligations (“claw back”) – Limited in time (maximum 3 years) and amount (maximum 25%) • How distributions will be made • Taxes • Tax withholding • Restrictions on redemptions and assignments – lock up periods and gates

VII. Legal Structure of Alternative Investment – Key Questions (Cont’d.) • Management of conflicts of interest by fund managers – at least arm’s length • Standard of care and limitations on duties of manager • Confidentiality restrictions • Investor inspection rights • Investor representations • Anti-money laundering and terrorist financing • Securities laws • Exemption from securities registration – qualified purchasers or accredited investors • Participation in new issue income from funds – not restricted persons

VIII. Qualification to Make Alternative Investments • Securities Act of 1933 • Accredited Investor • Investment Company Act of 1940 • Qualified Purchaser

IX. Dodd-Frank Act §619 – Volcker Rule • Hedge fund and private equity fund investment restrictions • Financial Stability Oversight Council Study and Recommendations on Prohibitions on Proprietary Trading and Certain Relationship with Hedge Funds and Private Equity Funds. • http://www.treasury.gov/initiatives/Documents/Volcker%20sec%20%20619%20study%20final%201%2018%2011% 20rg.pdf • Principles • Separation of banking system support from speculative investing with bank capital • Reduce potential conflicts of interest between bank and customer • Reduce risk banking entities

IX. Dodd-Frank Act §619 – Volcker Rule (Cont’d.) • Prohibited activities • Sponsorship of a hedge fund or private equity fund by a banking entity • Permitted activities • Provision of bona fide trust, fiduciary and investment advisory services • Limitations on permitted activities • Only in connection with designated services • Only to customers of designated services • Banking entity investment limited • No name sharing • No material conflict of interest • No material exposure or threat to banking entity safety and soundness

IX. Dodd-Frank Act §619 – Volcker Rule (Cont’d.) • Restrictions on relationships and transactions with private equity funds and hedge funds • Treatment of fund as an affiliate • Issues of conflicts of interest and transfer of funds from insured bank entity • Federal Reserve Act Section 23A covered transactions prohibited • Federal Reserve Act Section 23B arm’s length transactions

VIII. Dodd-Frank Act §619 – Volcker Rule (Cont’d.) • Volcker Rule implementation issues • Prohibited activities • Characteristics of fund • Structure as Section 3(c)(1) or Section 3(c)(7) fund • Permitted activities • “Customer” requirement • Feeder funds • De-minimis investments • Monitoring compliance • Investment and risk oversight • CEO public attestation • Transparency – public disclosure

X. Valuation • Duty to account/report and to inform - National Fiduciary Accounting Standards Project • Essential and useful information in a meaningful form • A fiduciary account should include the inventory value and current values • In determining current values for which there is no readily ascertainable current value, the source of the value should be stated and explained • The fiduciary should make a good faith effort to determine realistic values • Valuation impacts fees

X. Valuation (Cont’d.) • Financial Accounting Standard 157 – Fair Value Measurements • Financial statements, not trust accounting • Definition – The price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measuring date • Marketable securities – exchange price • Non-traditional assets – no market, limited transactions, limited information

X. Valuation (Cont’d.) • FASB Statement No. 157 Valuation Considerations for Interests in Alternative Investments; AICPA Accounting Standards Executive Committee and the Alternative Investments Task Force Draft Issues Paper (January 2009) • “Inputs” for estimating fair value • Net asset value, brokered transactions, discounted cash flow • “Integrity” of net asset value reported by fund managers • Additional factors affecting fair value - lock-up periods, suspension of redemptions, transfer restrictions

XI. Principal and Income Fiduciary Accounting • Interest and dividends trust accounting income • Partnership and LLC distributions generally income unless partial or total liquidations • Discretion under governing instrument and state law to make allocations in accordance with duty of impartiality • Allocation fees to income • No fraud or bad faith, allocation upheld • Power to adjust under some state P&I acts • Total return

XII. Fiduciary Administration • Tax reporting - state and federal • Entity 1065 and partner/member K-1; state tax reporting and withholding • Trust 1041 and beneficiary K-1 • Beneficiary 1040 • Investor qualifications and representations • Accredited investor and qualified purchaser • Indemnification provisions of operating agreements • Regulatory oversight • Distribution and liquidity requirements of trust

Conclusion • Universe of available investment vehicles has expanded • Non-traditional investments have been used by pension funds for years and are increasingly used in private trusts • The Prudent Investor Rule allows for use of non-traditional investments where appropriate • Complexity of non-traditional investments requires increased level of sophistication, consideration in certain circumstance of delegation, assessment of how the non-traditional investment will interface with overall administration of the trust

Conclusion • Keep all the ducks in a row

Contact Information Suzanne L. ShierChapman and Cutler LLP111 W. Monroe StreetChicago, Illinois 60603 312-845-2983shier@chapman.com