Download

1 / 32

320 likes | 425 Views

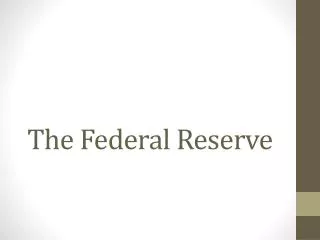

Economic & Industry Update March 8, 2011 Bob Costello Chief Economist & Vice President American Trucking Associations. Manufacturing Output. Seasonally Adjusted Level of Output; Index (2007=100). Forecast (annual average). 2000-2013. 3.8%. 3.2%. 4.7%. Sources: Federal Reserve & ATA.

E N D

Economic & Industry UpdateMarch 8, 2011Bob CostelloChief Economist & Vice PresidentAmerican Trucking Associations

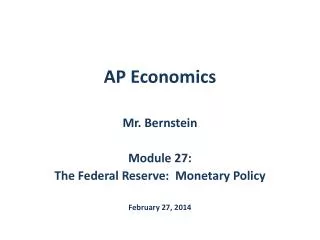

Manufacturing Output Seasonally Adjusted Level of Output; Index (2007=100) Forecast (annual average) 2000-2013 3.8% 3.2% 4.7% Sources: Federal Reserve & ATA

Retail Sales Billions Billions Seasonally Adjusted Annual Rates; Billions of Dollars Forecast (annual average) 2000-2013 2.6% 3.0% 3.5% Sources: Census Bureau & ATA

Wages Fell, but are Rising Again Private wages & salary disbursements; billions US$, annual rate Sources: Bureau of Economic Analysis and ATA

Household Net Worth Millions 1980 – Q3: 2010 Sources: Federal Reserve and ATA

Household Debt Service Ratio Percentage of Disposable Personal Income 1980 – Q3 2010 Sources: Federal Reserve and ATA

Housing Starts Millions Millions Seasonally Adjusted Annual Rates 2000-2013 Forecast (annual average) 31% 61% 16% Sources: Census Bureau & ATA

Total Business Inventories-to-Sales Ratio (Includes retail, wholesale, and manufacturing; Through December 2010) Sources: Census Bureau and ATA

Retail Inflation Measures Seasonally Adjusted; Year-over-Year Percent Change Through January 2011 Inflation is not a near-term threat, but something to watch in the longer-run. Sources: Department of Labor and ATA

Businesses are Cash Rich Millions 1952 – Q3 2010 Percentage of Liquid Assets to Total Assets Liquid Assets Sources: Federal Reserve and ATA

Real Gross Domestic Product (Real GDP, Annual percent change, 2005 dollars) 2008 – 2011 Long-run Average (3%) Annual GDP Numbers 2009: -2.6% 2010: +2.9% 2011: +3.2% 2012: +2.9% Sources: IHS Global Insight and ATA

The Biggest Concern: Oil Prices

Oil Prices (WTI) Price Per Barrel Source: Wall Street Journal

On-Highway Diesel Prices Price Per Gallon Source: Energy Information Administration

Billions Industry Diesel Expense Forecast Forecasts are derived from EIA diesel price forecasts and ATA truck freight volume forecasts. Sources: ATA, EIA, and Highway Statistics

Motor Carrier Trends Demand

For-Hire Truck TonnageAnnual Percent Change Includes TL & LTL Source: ATA’s Monthly Truck Tonnage Report

ATA’s For-Hire Truck Tonnage Index Seasonally Adjusted; 2000 = 100 Through January2011 Source: ATA’s Monthly Truck Tonnage Report

For-Hire TL LoadsAnnual Percent Change Source: ATA’sTrucking Activity Report

ATA’s For-Hire TL Loads Index Seasonally Adjusted; 2000 = 100 Through December 2010 Source: ATA’sTrucking Activity Report

Loads by TL Sector2010 Compared with 2009 Source: ATA’s Trucking Activity Report

ATA’s For-Hire TL & LTL Revenue Indexes Seasonally Adjusted; 2000 = 100 TL average Revenue/Mile LTL average Revenue/Ton Through December 2010 Source: ATA’sTrucking Activity Report

Motor Carrier Trends Supply Capacity Additions or Replacements?

U.S. Class 8 TrucksAverage Age 1995-2010 Sources: ACT Research & ATA

U.S. Class 8 Truck Sales Monthly Retail Sales; Through January 2011 • Annual Figures • 2005: 253k • 2006: 284k • 2007: 151k • 2008: 133k • : 95k • : 106k • : 111k • (rate from Jan only) Source: Wards

Illustration: Trade Cycle of a 2005 OTR Tractor Normal Mileage vs Actual and Projected Mileage Trade Point: 550,000 Miles Normal Mileage: 115,000/Year Actual Mileage based on average miles per truck per year from fleet surveys. Projected Mileage: 100,000 in 2010 and 115,000 in 2011. Source: ATA

Maintenance Costs per Mile Sources: TMC, Motor Carrier Annual Reports, and ATA

Truck Purchase Decision This example is for illustration purposes only. Actual numbers may vary. 2006 2010

Trucking Failures Failures only includes fleets with at least five trucks Source: Avondale Partners, LLC

For-Hire TL Supply vs Demand 2005 = 100 TL Loads Index TL Tractor Count Index Oversupply Through December 2010 Source: ATA

Thanks! Questions?