Download

1 / 15

160 likes | 177 Views

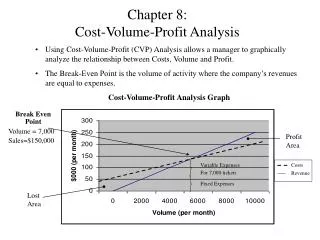

Chapter 3 Cost-Volume-Profit Analysis Breakeven point…. Effects of Sales Mix on CVP :.

E N D

Chapter 3Cost-Volume-Profit Analysis Breakeven point…. Dr.Mohamed Mousa

Effects of Sales Mix on CVP : • Sales Mix is the quantity or proportion of various products or services that constitute a company’s total unit sales. It is often the case that the various products or services have different contribution margins. • Up to this point, we’ve assumed a single product; more realistically, we’ll have multiple products with different costs and different margins. Dr . Mohamed Mousa

Effects of Sales Mix on CVP : • We can use the same formula in our CVP calculations but must use an average contribution margin for the products. • This technique assumes a constant mix at different levels of total unit sales. Dr . Mohamed Mousa

Example no 1: • Magi Industrial Company produces the products( x & y & z )and you have the following data: Dr . Mohamed Mousa

Example no 1: • If you know that the fixed costs of the company is 19600 $. • Required : 1. Determine the quantity and value of the B.E.P of each product. 2 - What is the sales number required to achieve a target profit capacity of 49000 $? Dr . Mohamed Mousa

Solution 1.Determine the weighted average return on contribution of the unit: Dr . Mohamed Mousa

Solution 2 - The Value of B.E.P To the company as a whole: B.E.PR =F. C / Total Average Contribution = 19600 / 0,245 = 80000 $ • the value of B.E.P per product: = The value of B.E.P To the company as a whole× sales mix ratio. Dr . Mohamed Mousa

Solution • B.E.P RTo Product x = 80000 x 30% = 24000 $. • B.E.P uTo Product x = 24000 $ / 30 (s.p) = 800 Unit. • B.E.P RTo Product y = 80000 x 50% = 40000 $. • B.E.P uTo Product y = 40000 $ / 20 (s.p) = 2000 Unit. • B.E.P RTo Product z = 80000 x 20% = 16000 $. • B.E.P uTo Product z = 16000$ / 16(s.p) = 1000Unit. Dr . Mohamed Mousa

Solution 3 – The B.E.P R that earn a profit of 49000 $ : =(F. C + O.I ) / Total Average Contribution = (19600 + 49000 ) / 0,245 = 280000 $ • the value of sales that earn a profit per product: = The B.E.P R that earn a profit To the company as a whole × sales mix ratio. Dr . Mohamed Mousa

Solution • V.S.PTo Product x = 280000 x 30% = 84000 $. • N.S.P To Product x = 84000 $ / 30 (s.p) = 2800 Unit. • V.S.PTo Product y = 280000 x 50% = 140000 $. • N.S.P To Product y = 140000 $ / 20 (s.p) = 7000 Unit. • V.S.PTo Product z = 280000 x 20% = 56000$. • N.S.P To Product z = 56000$ / 16(s.p) = 3500Unit. Dr . Mohamed Mousa

Exercises:( Case Study ) • ZAAT Industrial Company produces the products( K & L & M )and you have the following data: Dr . Mohamed Mousa

Exercises : • If you know that the fixed costs of the company is 166800 $. • Required : 1. Determine the quantity and value of the B.E.P of each product. 2 - What is the sales number required to achieve a target profit capacity of 133200 $? Dr . Mohamed Mousa

CVP for Service and Not-For-Profit Organizations : • CVP isn’t just for merchandising and manufacturing companies. • Service and Not-For-Profit businesses need to focus on measuring their output which is different from the units sold that we’ve been dealing with. • For example, a service agency might measure how many persons they assist or an airline might measure how many passenger miles they fly. • What measure might a hotel use? A restaurant?

Contribution Margin versus Gross Margin : • Recall from Chapter 2 that Gross Margin = Revenue – Cost of Goods Sold. • In Chapter 3, we learned about Contribution Margin which is Revenue – All Variable Costs. • Gross Margin measures how much a company charges for its products over and above the cost of acquiring or producing them. • Contribution Margin indicates how much of a company’s revenue is available to cover fixed costs. • This is especially significant in the manufacturing sector where businesses carry inventory.

The Next Lecture Chapter 6 “ The Master Budget and Responsibility accounting “ Dr . Mohamed Mousa