Download

1 / 24

240 likes | 438 Views

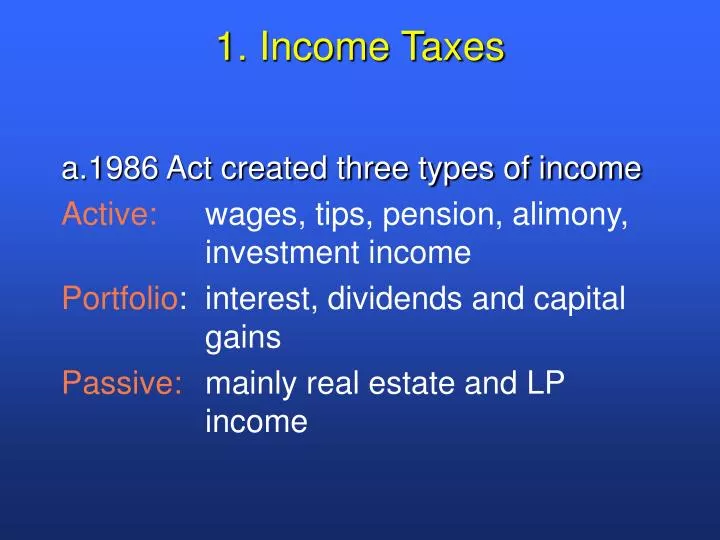

1. Income Taxes. a.1986 Act created three types of income Active: wages, tips, pension, alimony, investment income Portfolio : interest, dividends and capital gains Passive: mainly real estate and LP income. b. Income versus Capital Gains.

E N D

1. Income Taxes a.1986 Act created three types of income Active: wages, tips, pension, alimony, investment income Portfolio: interest, dividends and capital gains Passive: mainly real estate and LP income

b. Income versus Capital Gains * Each year, marginal income tax brackets are indexed based on changes in the CPI. * Bracket increases now are the lowest since adjustments began in mid-80’s * Beyond 20% rate, aim for LTCG

e. 1997, 2001Tax Revisions:Major Elements That AffectedIndividual Investors 1) Capital Gains: a) reduced top rate to 20 % b) reduced holding period to12 months c) 18 % rate applies to assets bought after 2000 and held for 5 years

d) collectible gains still hit @ 28% e) 10 % rate for taxpayers in the 14.5 % bracket. The rate falls to 8 % on assets held more than 5 years

3) Home Sales: a) Exempts up to $500K of profit for married, filing jointly. ($250K for singles) b) Full exemption available once every two years * must be personal residence for 2 out of previous 5 years prior to sale - if used as rental, tax benefits can be reduced

* exemption to reduce or eliminate tax is available even if in the house < 2 years in the case of: death, divorce, unemployment, in some cases even if owner can no longer afford the mortgage, “labor” induced sale – those who sell because of multiple births from the same pregnancy 12/19/02 WSJ by Tom Herman Personal Financial Management

c) Real estate investors are hurt vis-à-vis stocks and bonds since maximum tax rate of 25 % applies to depreciation recapture Ref: "Tax package: Double-Edged Sword for Homeowners”

4) Retirement Savings a) ROTH IRA * Benefits • Fed tax avoidance (not deferral) on all gains (equivalent to municipal bond except one can buy equities with higher expected returns) - no requirement to begin distributions by age 70 ½ - contributions can be made after 70 ½ - money passes income-tax free to heirs Ref: “Converting to Roth IRA…”

* Eligible Persons - eligibility phases out by $150K- $160K for couples ($95K - $110K for singles) - contributions are deductible for higher earners not covered by a company plan * Contribution Limits - $3,000 in 2002 rising to $5,000 in 2008, (including non-working spouses); indexed after that - beginning in 2002, person over 50 can add extra $500 to contribution - contributions can be split between traditional and Roth IRA

Maxing Out IRA/Roth IRA Personal Financial Management

* Withdrawals • contributions can be withdrawn anytime w/out penalty (1st $ out are deemed to be contributions) • no tax on gains if money remains in account for at least 5 years and then pulled for education, 1st home purchase (or past age 59 1/2) * Who Should Consider Roth IRA- generally tax free growth beats a tax deduction today followed by tax at ordinary income rates later. So, put new $ in Roth (if expected retirement MTR is lower, the traditional IRA probably makes more sense)

* Who Should Consider Roth IRA (Continued) - people who are cash short may favor tax deductible IRA because out-of-pocket funding cost is lower • higher income earners who were ineligible for traditional IRA • For help on deciding which one (Roth versus traditional IRA) is right for you, try http://www.quicken.com/retirement/RIRA/planner/ Ref: “Washington Gives IRA Gift…”

b) Traditional IRA’s: * $3,000 in 2002 rising to $5,000 in 2008, indexed after that (beginning in 2002, person over 50 can add extra $500 to contribution) * income limits rise for tax deductibility (to $80K for couples, to $50K for singles - by 2004) * penalty free withdrawals before 59 1/2 for educational purposes and 1st time home purchases

c) 401(k) • tax deferral on contributions and build-ups • tax deferral on matches ( 50c to $1, often the match is made up to 6%) • maximum contribution: for individual: Lesser of $11,000 ($12K if 50+ or 25% of pay (latter % is reduced by employer’s % match) for you and your employer: Lesser of $40,000 or 100% of earned income. Personal Financial Management

d) 403(b), 457 * contributions are reductions in reported gross income * tax deferral on build-up * laws changed effective 1/1/02 - deferral limits on 457 and 403 were uncoupled. Employees now can contribute the maximum to both accounts. * 2002 pre-tax deferral limit is $11,000 ($12K if 50+) “Economic Growth and Tax Relief Reconciliation Act of 2001” Personal Financial Management

Maxing Out – 401 (k), 457 (b) and 403 (b) Personal Financial Management

e)Self-Employed Plans: • New (2002) Solo(k) plans, SEP and SIMPLE IRA’s are said to dominate Keogh plans. For information on Solo plans try: http://online.wsj.com/article/0,,SB1037203959459702068,00.html?mod=article-outset-box • Keogh plans offer provide greater tax shelter (maximum: lesser of $35,000 or 25% of earned income), but carry greater administrative and reporting requirements. Personal Financial Management

5) Education Savings a) IRA. * Contribution limit is $2,000 per child in 2002. (This is in addition to IRA/RothIRA limit) * No deduction but tax free earnings * Funds must be withdrawn by time child reaches age 30

* Eligibility: (Phase-out range 2001) single: AGI $95K to $110K married, filing jointly: AGI $150K to $160K * Unlike IRA and Roth IRA, no earned compensation requirement for a person to open an EIRA. Therefore, person with excess AGI can finesse the rule by gifting and then donee can open an EIRA Personal Financial Management

2. Estate and Gift Taxes • Overview Thanks to the 1969 Tax Reform Act and the 1997 Act, every U.S citizen and resident can transfer—during life or at the time of death—up to $1,000,000 in 2002 to any beneficiary without any federal estate or gift tax. This is accomplished by applying a unified tax credit to the tax due. The 2001 tax legislation ended the unified tax concept because property transfers are no longer tax neutral in life versus death. “New Era For Estate Planning”, July 1, 2001

b. Gifts 1) Up to $11,000 tax free in 2002 a) No gift tax liability for donor and no income tax liability for recipient b) Recipient should cash check in gift year just to be safe, 2) Donors can give more than $11K per year by directly paying someone else's qualified tuition or medical expenses 3) The 2001 Act added a lifetime exemption of $1,000,000 (tax on amounts above this start at 41% so it may be cheaper to delay a sizable gift and transfer the $ at death) Personal Financial Management

c. Estates - 2001 Revisions and eventual (maybe) repeal Personal Financial Management