Download

1 / 20

200 likes | 1.04k Views

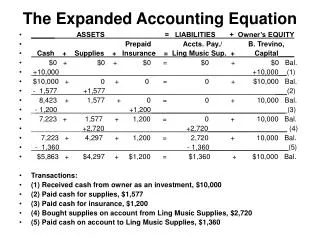

Social Accounting for Economically Targeted Investments: The Expanded Value Added Statement. Laurie Mook, OISE/University of Toronto October 15, 2005. Accounting Reports. A trade union approach to pension fund investing. Create good, unionized jobs

E N D

Social Accounting for Economically Targeted Investments: The Expanded ValueAdded Statement Laurie Mook, OISE/University of Toronto October 15, 2005

A trade union approach to pension fund investing • Create good, unionized jobs • Earn good returns with targeted social, economic and environmental objectives • Promote good corporate behaviour • Limit excesses of corporate executives and inside shareholders • Curb anti-social corporate behaviour such as environmental pollution and child labour (CLC 2004)

Economically Targeted Investments (ETIs) • One type of socially responsible investment which “seeks to obtain risk-adjusted market grade returns while achieving collateral benefits for plan members and their communities” (SHARE, n.d.)

Value Added • Value added is a measure of wealth that an organization creates by adding value to raw materials, products and services through the use of labour and capital. • typically measured by the difference between the market value of the goods or services produced, and the cost of goods and services purchased from other producers (Ruggles and Ruggles 1965)

Example • Raw materials (wood, screws, glue, etc.) • Transformed by labour and capital • Finished table

Example • Raw materials (wood, screws, glue, etc.) $100 • Transformed by labour and capital • Finished table $300

Example • Raw materials (wood, screws, glue, etc.) $100 • Transformed by labour and capital $200 • Finished table $300

Limitations of traditional value added • Focuses only on financial items and pays no attention to intangibles and items that do not pass through the market • Does not account for indirect impacts of an organisation’s activities • Does not make explicit the choices made in obtaining resources

Outputs • Direct outputs: • direct effects of an organization’s activities on its customers/clients • Indirect outputs: • Indirect effects on clients/customers • Indirect effects on those other than clients/customers

Sustainable Building Example Traditional building Marginal cost to build using sustainable design elements Total Benefits to customers Benefits to wider society Combined

Benefits • To customers • Savings due to decreased energy, water, and maintenance costs • Savings due to increased productivity and health of employees (occupants) • To wider society • Reduction in waste and emissions • 5 percent increase in costs resulted in 10 times benefits received over 20 years (Kats et al. 2003)

Key Considerations • Creation of jobs • Contributions to pension funds (deferred wages) • Return on investment to pension fund investors • Impact on residents • Impact on local community • Environmental impact

EVAS • Traditional costs • Marginal costs: • Employee development • Community development • Environmentally sustainable development • Total costs • Benefits • Employees • Customer/Client • Societal • Combined

Next Steps • Further development needed in identifying, measuring, quantifying, standardizing and placing a value on key social and environmental indicators

Further Reading Canadian Labour Congress (2004) A Trade Union Approach to Pension Fund Investing. Available from Internet URL <http://www.canadianlabour.ca> Kats G, Alevantis L, Berman A, Mills, E and Perlman J (2003). The Costs and Financial Benefits of Green Buildings: A Report to California’s Sustainable Building Task Force. Available from Internet URL <http://www.usgbc.org/Docs/News/News477.pdf> Mook L (forthcoming 2005). Integrating and Reporting an Organisation’s Economic, Social and Environmental Performance: The Expanded Value Added Statement. In Schaltegger, S., M. Bennett, J Bouma & R. Burritt (Eds.), Sustainability Accounting and Reporting. Dordrecht: Springer Kluwer Publishers.

Thank you! Contact information: Laurie Mook OISE/University of Toronto Department of Adult Education 252 Bloor St. W., Toronto, Ontario Canada M1L 3S9 Email: Lmook@oise.utoronto.ca Website: http://home.oise.utoronto.ca/~lmook