Download

1 / 55

620 likes | 1.07k Views

CHAPTER 6 Risk and Rates of Return. Stand-alone risk Portfolio risk Risk & return: CAPM/SML. What is investment risk?. Investment risk pertains to the probability of actually earning a low or negative return. The greater the chance of low or negative returns, the riskier the investment.

E N D

CHAPTER 6 Risk and Rates of Return • Stand-alone risk • Portfolio risk • Risk & return: CAPM/SML

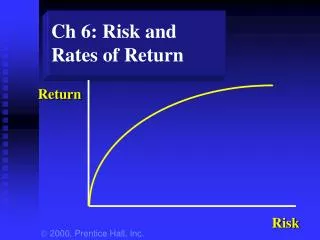

What is investment risk? Investment risk pertains to the probability of actually earning a low or negative return. The greater the chance of low or negative returns, the riskier the investment.

Probability distribution Firm X Firm Y Rate of return (%) -70 0 15 100 Expected Rate of Return

Annual Total Returns,1926-1998 Average Standard Return Deviation Distribution Small-companystocks 17.4% 33.8% Large-companystocks 13.2 20.3 Long-termcorporate bonds 6.1 8.6 Long-termgovernment 5.7 9.2 Intermediate-termgovernment 5.5 5.7 U.S. Treasurybills 3.8 3.2 Inflation 3.2 4.5

Investment Alternatives(Given in the problem) Economy Prob. T-Bill HT Coll USR MP Recession 0.1 8.0% -22.0% 28.0% 10.0% -13.0% Below avg. 0.2 8.0 -2.0 14.7 -10.0 1.0 Average 0.4 8.0 20.0 0.0 7.0 15.0 Above avg. 0.2 8.0 35.0 -10.0 45.0 29.0 Boom 0.1 8.0 50.0 -20.0 30.0 43.0 1.0

Why is the T-bill return independent of the economy? Will return the promised 8% regardless of the economy.

Do T-bills promise a completelyrisk-free return? No, T-bills are still exposed to the risk of inflation. However, not much unexpected inflation is likely to occur over a relatively short period.

Do the returns of HT and Coll. move with or counter to the economy? • HT: Moves with the economy, and has a positive correlation. This is typical. • Coll: Is countercyclical of the economy, and has a negative correlation. This is unusual.

Calculate the expected rate of return on each alternative: ^ k = expected rate of return. ^ kHT = (-22%)0.1 + (-2%)0.20 + (20%)0.40 + (35%)0.20 + (50%)0.1 = 17.4%.

^ k HT 17.4% Market 15.0 USR 13.8 T-bill 8.0 Coll. 1.7 HT appears to be the best, but is it really?

What’s the standard deviationof returns for each alternative? = Standard deviation. = = =

é ù ê ú ê ú ê ú ë û 1/2 (8.0 – 8.0)20.1 + (8.0 – 8.0)20.2 + (8.0 – 8.0)20.4 + (8.0 – 8.0)20.2 + (8.0 – 8.0)20.1 s = T - bills sT-bills = 0.0%. sColl = 13.4%. sUSR = 18.8%. sM = 15.3%. sHT = 20.0%.

Prob. T-bill USR HT 0 8 13.8 17.4 Rate of Return (%)

Standard deviation (si) measures total, or stand-alone, risk. • The larger the si , the lower the probability that actual returns will be close to the expected return.

Expected Returns vs. Risk Expected Risk, s Security return HT 17.4% 20.0% Market 15.0 15.3 USR 13.8* 18.8* T-bills 8.0 0.0 Coll. 1.7* 13.4* *Seems misplaced.

Coefficient of Variation (CV) Standardized measure of dispersion about the expected value: Std dev s CV = = . ^ Mean k Shows risk per unit of return.

B A 0 sA = sB , but A is riskier because larger probability of losses. s = CVA > CVB. ^ k

Portfolio Risk and Return Assume a two-stock portfolio with $50,000 in HT and $50,000 in Collections. ^ Calculate kp and sp.

Portfolio Return, kp ^ ^ kp is a weighted average: n ^ ^ kp = Swiki. i = 1 ^ kp = 0.5(17.4%) + 0.5(1.7%) = 9.6%. ^ ^ ^ kp is between kHT and kCOLL.

Alternative Method Estimated Return Economy Prob. HT Coll. Port. Recession 0.10 -22.0% 28.0% 3.0% Below avg. 0.20 -2.0 14.7 6.4 Average 0.40 20.0 0.0 10.0 Above avg. 0.20 35.0 -10.0 12.5 Boom 0.10 50.0 -20.0 15.0 ^ kp = (3.0%)0.10 + (6.4%)0.20 + (10.0%)0.40 + (12.5%)0.20 + (15.0%)0.10 = 9.6%.

1 / 2 é ù ê ú (3.0 – 9.6)20.10 + (6.4 – 9.6)20.20 + (10.0 – 9.6)20.40 + (12.5 – 9.6)20.20 + (15.0 – 9.6)20.10 ê ú ê ú ê ú p= = 3.3%. ê ú ê ú ê ú ê ú ê ú ë û 3.3% CVp = = 0.34. 9.6%

sp = 3.3% is much lower than that of either stock (20% and 13.4%). • sp = 3.3% is lower than average of HT and Coll = 16.7%. • \ Portfolio provides average k but lower risk. • Reason: negative correlation. ^

General statements about risk • Most stocks are positively correlated. rk,m» 0.65. • s » 35% for an average stock. • Combining stocks generally lowers risk.

Returns Distribution for Two Perfectly Negatively Correlated Stocks (r = -1.0) and for Portfolio WM Stock W Stock M Portfolio WM . . . . 25 25 25 . . . . . . . 15 15 15 0 0 0 . . . . -10 -10 -10

25 25 15 15 0 0 -10 -10 Returns Distributions for Two Perfectly Positively Correlated Stocks (r = +1.0) and for Portfolio MM’ Stock M’ Portfolio MM’ Stock M 25 15 0 -10

What would happen to theriskiness of an average 1-stockportfolio as more randomlyselected stocks were added? • sp would decrease because the added stocks would not be perfectly correlated but kp would remain relatively constant. ^

Prob. Large 2 1 0 15 Even with large N, sp» 20%

sp (%) Company Specific Risk 35 Stand-Alone Risk, sp 20 0 Market Risk 10 20 30 40 2,000+ # Stocks in Portfolio

As more stocks are added, each new stock has a smaller risk-reducing impact. • sp falls very slowly after about 10 stocks are included, and after 40 stocks, there is little, if any, effect. The lower limit for sp is about 20% = sM .

Stand-alone Market Firm-specific = + risk risk risk Market risk is that part of a security’s stand-alone risk that cannot be eliminated by diversification, and is measured by beta. Firm-specific risk is that part of a security’s stand-alone risk that can be eliminated by proper diversification.

By forming portfolios, we can eliminate about half the riskiness of individual stocks (35% vs. 20%).

If you chose to hold a one-stock portfolio and thus are exposed to more risk than diversified investors, would you be compensated for all the risk you bear?

NO! • Stand-alone risk as measured by a stock’s sor CV is not important to a well-diversified investor. • Rational, risk averse investors are concerned with sp , which is based on market risk.

There can only be one price, hence market return, for a given security. Therefore, no compensation can be earned for the additional risk of a one-stock portfolio.

Beta measures a stock’s market risk. It shows a stock’s volatility relative to the market. • Beta shows how risky a stock is if the stock is held in a well-diversified portfolio.

How are betas calculated? • Run a regression of past returns on Stock i versus returns on the market. Returns = D/P + g. • The slope of the regression line is defined as the beta coefficient.

_ ki Illustration of beta calculation: Regression line: ki = -2.59 + 1.44 kM ^ ^ . 20 15 10 5 . Year kM ki 1 15% 18% 2 -5 -10 3 12 16 _ -5 0 5 10 15 20 kM -5 -10 .

If beta = 1.0, average stock. • If beta > 1.0, stock riskier than average. • If beta < 1.0, stock less risky than average. • Most stocks have betas in the range of 0.5 to 1.5.

List of Beta Coefficients Stock Beta Merrill Lynch 2.00 America Online 1.70 General Electric 1.20 Microsoft Corp. 1.10 Coca-Cola 1.05 IBM 1.05 Procter & Gamble 0.85 Heinz 0.80 Energen Corp. 0.80 Empire District Electric 0.45

Can a beta be negative? Answer: Yes, if ri, m is negative. Then in a “beta graph” the regression line will slope downward. Though, a negative beta is highly unlikely.

_ b = 1.29 ki HT 40 20 b = 0 T-Bills _ kM -20 0 20 40 -20 Coll. b = -0.86

Expected Risk Security Return (Beta) HT 17.4% 1.29 Market 15.0 1.00 USR 13.8 0.68 T-bills 8.0 0.00 Coll. 1.7 -0.86 Riskier securities have higher returns, so the rank order is OK.

Use the SML to calculate therequired returns. • Assume kRF = 8%. • Note that kM = kM is 15%. (Equil.) • RPM = kM – kRF = 15% – 8% = 7%. SML: ki = kRF + (kM– kRF)bi . ^

Required Rates of Return kHT = 8.0% + (15.0% – 8.0%)(1.29) = 8.0% + (7%)(1.29) = 8.0% + 9.0% = 17.0%. kM = 8.0% + (7%)(1.00) = 15.0%. kUSR = 8.0% + (7%)(0.68) = 12.8%. kT-bill = 8.0% + (7%)(0.00) = 8.0%. kColl = 8.0% + (7%)(-0.86) = 2.0%.

Expected vs. Required Returns ^ k k HT 17.4% 17.0% Undervalued: k > k Market 15.0 15.0 Fairly valued USR 13.8 12.8 Undervalued: k > k T-bills 8.0 8.0 Fairly valued Coll. 1.7 2.0 Overvalued: k < k ^ ^ ^

SML: ki = 8% + (15% – 8%) bi . ki (%) SML . HT . . kM = 15 kRF = 8 USR . T-bills . Coll. Risk, bi -1 0 1 2

Calculate beta for a portfolio with 50% HT and 50% Collections bp= Weighted average = 0.5(bHT) + 0.5(bColl) = 0.5(1.29) + 0.5(-0.86) = 0.22.

The required return on the HT/Coll. portfolio is: kp = Weighted average k = 0.5(17%) + 0.5(2%) = 9.5%. Or use SML: kp= kRF + (kM– kRF) bp = 8.0% + (15.0% – 8.0%)(0.22) = 8.0% + 7%(0.22) = 9.5%.

If investors raise inflation expectations by 3%, what would happen to the SML?

Required Rate of Return k (%) D I = 3% New SML SML2 SML1 18 15 11 8 Original situation 0 0.5 1.0 1.5 Risk, bi