Download

1 / 27

270 likes | 475 Views

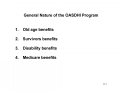

General Nature of the OASDHI Program. 1. Old age benefits 2. Survivors benefits 3. Disability benefits 4. Medicare benefits. Eligibility and Qualification. 1. Quarter of coverage 2. Fully insured status 3. Currently insured status. Financing.

E N D

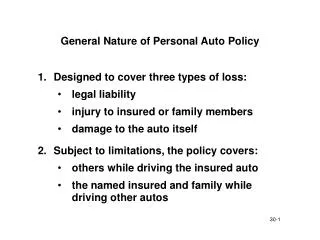

General Nature of the OASDHI Program • 1. Old age benefits • 2. Survivors benefits • 3. Disability benefits • 4. Medicare benefits

Eligibility and Qualification • 1. Quarter of coverage • 2. Fully insured status • 3. Currently insured status

Financing • 1. FICA tax: originally 1%, 7.65% by 1998 (payable by employer and employee). • 2. The tax base: originally $3,000, $64,800 by 1998. • 3. Self-employment tax: originally about 1.5 times employee tax. Now equals combined tax for employees, but self employed may deduct one-half self-employment tax paid.

Amount of Benefits • 1. All benefits are based on Primary Insurance Amount (PIA). • 2. PIA is amount to which worker would be entitled for retirement at age 65. • 3. PIA is based on worker’s average earnings during period of employment, subject to certain adjustments.

Computing the PIA • 1. Computation period: • year worker reaches age 22 until year before worker reaches age 62, dies, or is disabled. • 2. Up to 5 years may be dropped. Minimum 2 years in computation. • 3. Recorded earnings are indexed to determine Average Indexed Monthly Earnings (AIME). • 4. Primary Insurance Amount is computed from AIME by formula.

Retirement Benefits • 1. Worker at age 65 (reduced benefit at age 62) • 2. Spouse of a retired worker • 3. Children’s benefit (child of retired worker) • under age 18 • under age 19 if a student • over 18 if disabled prior to age 18 • 4. Mother’s or father’s benefit to parent with child under 16 in care

Survivor Benefits • 1. Lump sum benefit $255 • 2. Children’s benefit • 3. Mother’s or father’s benefit • 4. Widow’s or widower’s benefit • 5. Parent’s benefit

Disability Benefits • 1. Disabled worker • 2. Child of a disabled worker • 3. Mother’s or father’s benefit

Summary of Qualification Requirements • Benefit Insured Status • Survivor Benefits • Children’s benefit Fully or currently • Mother’s/father’s benefit Fully or currently • Dependent parent Fully insured • Widow or widower Fully insured • Lump-sum death benefit Fully or currently • Retirement Benefits • Retired worker’s benefit Fully insured • Spouse of worker’s benefit Fully insured • Child’s benefit Fully insured • Mother’s or father’s benefit Fully insured

Summary of Qualification Requirements Insured Status Required 20 of the last 40 quarters fully insured or 6 of last 12 quarters if under age 24 1 of every 2 quarters since age 21 if between ages 23 and 31 • Benefit • Disability Benefits • Disabled worker • Spouse of disabled worker • Child of disabled worker • Mother’s/father’s benefit

Benefits as Percent of Worker’s PIA • Retired worker at age 65 100.0% • Disabled worker under 65 100.0% • Retired worker at age 62 80.0% • Spouse of retired worker age 65 50.0% • Spouse of retired worker age 62 37.5% • Child of retired/disabled worker 50.0% • Spouse under 65 with 1 child 50.0% • Widow or widower at age 62 80.0% • Widow or widower at age 60 71.5% • Disabled widow or widower age 50 71.5% • One surviving child 75.0% • Widow or widower with 1 child 150.0%

Loss of Benefits - General • 1. Divorce from person receiving benefits • 2. Attainment of age 18 by a child • 3. Marriage • 4. Adoption • 5. Disqualifying income

Loss of Benefits - Disqualifying Income • 1. Disqualifying income is not a “needs” test but a retirement test. • 2. Different amounts of exempt earnings apply to beneficiaries of different ages • Under age 65 $9,120 in 1998 • Over 65 but under 70 $14,500 in 1998 • Over age 70 No limit • 3. Exempt income for persons over 65 scheduled to increase to $30,000 by 2002.

Loss of Benefits - Disqualifying Income • 4. If earnings exceed exempt amounts, a part of the social security benefit will be lost. • 5. Amount of benefits lost depends on the age of the beneficiary: • Age of Benefits Lost for Earnings BeneficiaryAbove Exempt Amounts • Under age 65 $1 for each $2 in earnings • Age 65 to 70 $1 for each $3 in earnings • Over age 70 No loss of benefits

Taxation of Social Security Benefits • 1. Amount of benefits subject to tax depends on combined income and filing status. • 2. “Combined income” is the sum of adjusted gross income, tax exempt interest, and one-half the social security benefit. • 3. If combined income is between $25,000 and $34,000, up to 50% of social security benefits may be taxed. • 4. If combined income is over $34,000, up to 85% of the benefits may be taxed. • 5. For those filing joint returns, break points are $32,000 and $44,000.

Soundness of the Program • 1. FICA tax has increased from a maximum of $30 each for employer and employee in 1936 to $4,941 each 1998. • 2. Periodic crises have required legislated increases in contribution rates to “save” the system. • 3. Increasing tax and anticipated financial difficulties result from • increasing number of beneficiaries • increasing level of benefits.

Soundness of the Program • FUTURE PROJECTIONS • 1. Trust funds have increased from about $45 billion in 1982 to $656 billion in 1998. • 2. Based on intermediate assumptions, trust funds will peak at about $3 trillion in 2018. • 3. After 2018, deficits will deplete the trust funds by 2032.

Soundness of the Program • Trust fund investment in government bonds • government is borrowing from trust funds to cover current operations. • bonds will have to be redeemed when trust funds are depleted. • the question is “where will the money come from?”

Proposals for Change • 1. Changes in financing - opposing proposals • higher taxes instead of higher base • apply tax to all earned income • 2. Changes in benefits • return to “Floor of Protection” concept • Increase retirement age (now scheduled to increase from 65 to 67 by 2022. • 3. Allow workers to avail themselves of private alternatives to social security through increased contribution limits for IRAs

Workers Compensation • 1. Social insurance program that protects covered workers and their dependents against work-related disability and death. • 2. The system is based on statutes that exist in all states, which require employers to provide benefits specified by the law to covered workers and their dependents. • 3. Workers compensation laws were enacted in response to dissatisfaction with Employers Liability law.

Employers Common Law Obligations • Under common law, employers were obligated • 1. To provide a safe place to work • 2. To provide safe tools • 3. To provide sane and sober fellow employees • 4. To set up and enforce safety rules • 5. To warn worker of any dangers

Employers Common Law Defenses • If a worker was injured, the employer could interpose the following defenses • 1. Contributory negligence • 2. Fellow servant doctrine • 3. Assumption of risk

Principles of Workers Compensation • 1. Negligence is no longer a factor in determining liability. • 2. Indemnity is partial but final. • 3. Periodic payments are made to workers. • 4. Cost of the program is made a cost of production. • 5. Insurance is required.

Overview of Workers Compensation Laws • 1. Persons covered • None of the laws cover all employees. • Most frequently excluded classes are agricultural and domestic employees. • Laws permit employer of persons excluded to bring these workers under the law voluntarily.

Overview of Workers Compensation Laws • 2. Injuries covered • Coverage applies to injuries arising out of and in the course of employment. • All states also provide coverage for occupational disease.

Overview of Workers Compensation Laws • Workers Compensation Benefits • 1. Medical Expenses • 2. Total Temporary Disability • 3. Partial Temporary Disability • 4. Total Permanent Disability • 5. Partial Permanent Disability • 6. Survivors’ Death Benefit • 7. Rehabilitation Benefits

Second Injury Funds • 1. Under most laws, loss of both arms, feet, legs, eyes, or any two of these constitutes total permanent disability. • 2. A worker who has lost an arm, leg, or eye and returns to work could be totally disabled by a second accident. • 3. Second injury funds--designed to encourage employment of previously disabled workers--pay the difference between the partial disability and total disability. • 4. Funding comes mainly from insurers.