Download

1 / 20

200 likes | 293 Views

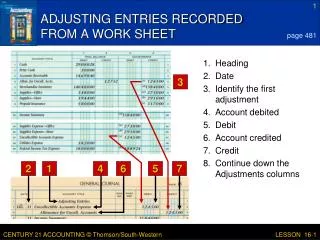

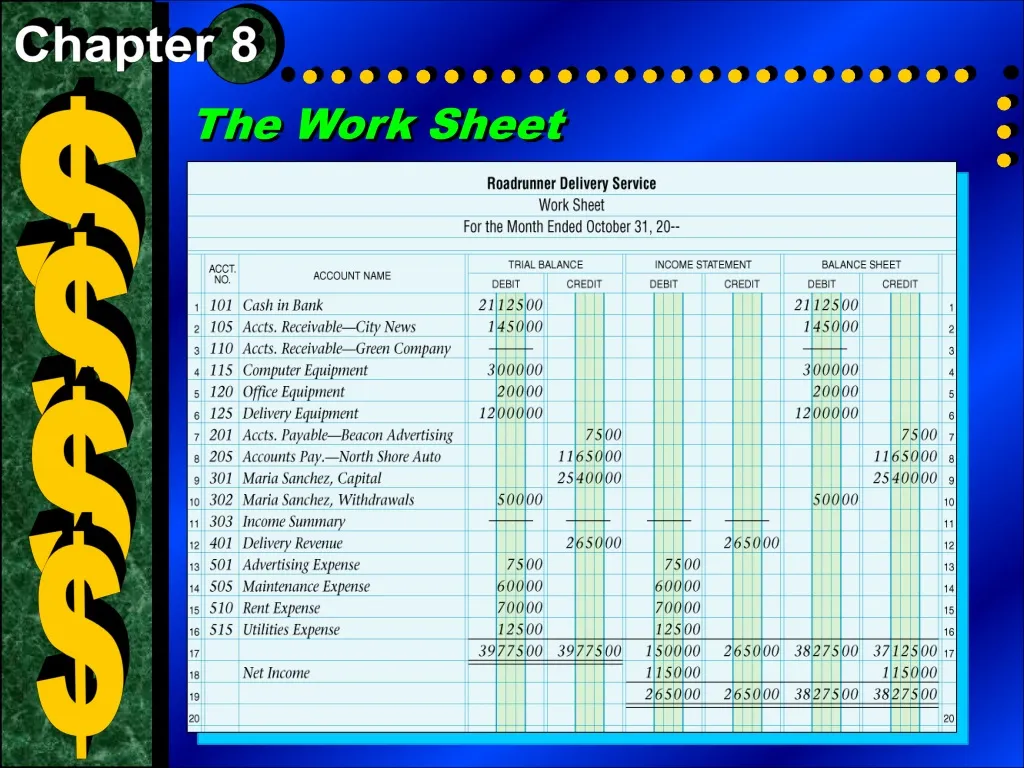

Chapter 8. $. The Work Sheet. $. $. $. The Sixth Step of the Accounting Cycle: The Work Sheet. The worksheet is used to: Collect information from the general ledger accounts into one place. Prepare the end-of-period formal financial statements Prepared:

E N D

Chapter 8 $ The Work Sheet $ $ $

The Sixth Step of the Accounting Cycle: The Work Sheet The worksheet is used to: • Collect information from the general ledger accounts into one place. • Prepare the end-of-period formal financial statements Prepared: • At the end of the accounting period • After all journal entries have been posted • In pencil – YOU CAN ERASE!!!!

Chapter 8 $ The Heading $ $ $

The Heading • Who? The name of the business • What ? Name of accounting form • When Fiscal period covered by the work sheet Example: For the quarter ended March 31, 2011

Chapter 8 $ The Account Name and Trial Balance Sections $ $ $

The Account Name and Trial Balance Sections • Account numbers and account titles are listed on the work sheet in the same order as they appear in the general ledger: A, L, OE, R, E • Account balances are entered under the appropriate debit or credit column. • If an account has a zero balance – the account is included. • The zero balance is shown with a dash in the normal balance column. • Income Summary does not have a normal balance – put dashes in both columns

Chapter 8 $ Ruling and Totaling the Trial Balance Section • Total debits must equal total credits. $ $ $

Ruling and Totaling the Trial Balance Section • Single rule drawn under a column(s) • This indicates math is to be performed. • When totaling the debit column and the credit column they must equal. • Double rule drawn under a column(s) • This indicates the amounts just above are totals and that no other entries will be made in the columns. • Totals must equal before moving onto next section. If they do not equal, you must locate and correct any errors before proceeding.

Chapter 8 $ The Balance Sheet Section $ $ $

The Balance Sheet Section • To extend the balance sheet accounts to the appropriate section is to physically transfer the amounts • Balance sheet accounts include: A, L & OE accounts without the Income Summary. • Withdrawals is extended as it has a direct impact on the Capital account. • Work from the top of the worksheet to the bottom of the worksheet when extending figures – be careful to move to the appropriate column. • This section will be used later to prepare a formal financial statement.

Chapter 8 $ The Income Statement Section $ $ $

The Income Statement Section • To extend the income statement accounts to the appropriate section is to physically transfer the amounts • Income statement accounts include: Revenue, Expense and the Income Summary account,. • The Income Summary account is used to serve as a clearing account for the temporary revenue and expense accounts. • Extended after the accounts are extended to the BS section – be careful to move to appropriate column. • This section will be used later to prepare a formal financial statement.

Chapter 8 $ Totaling the Income Statement and Balance Sheet Sections $ $ $

Totaling the Income Statement and Balance Sheet Sections • Draw a single rule across the four debit and credit columns. • The debit and credit columns in each section will not be equal • The difference in each section will represents the net income/loss.

Chapter 8 $ Showing Net Income on the Work Sheet $ $ $

Showing Net Income/Net Loss on the Work Sheet • Skip a line after the last account title and then write the words “Net Income” in the Account Name column • On the same line, enter the: • net income amount in the IS debit column • net loss amount in the IS credit column • On the same line, enter the: • net income account in the BS credit column • net loss amount in the BS debit column

Chapter 8 $ Completing the Work Sheet $ $ $

Completing the Work Sheet • Draw a single rule across all four columns on the line under the net income/loss amount • Calculate new totals for IS section. • Total debits should equal total credits • Calculate new totals for BS section. • Total debits should equal total credits. • Draw a double rule under the column totals and across all four columns. • The double rule indicates that no more amounts will be entered and the totals agree.

Chapter 8 Completing the Work Sheet with a Net Loss Expenses are greater than Revenue

Chapter 8 $ The Matching Principle Matching expenses incurred against the revenue earned for the same period. This allows a business to see the cost of producing the revenue. Calculate the difference between the revenue and expenses: Revenue greater than expenses = Net income Expenses greater than revenue = Net loss $ $ $