Download

1 / 17

170 likes | 328 Views

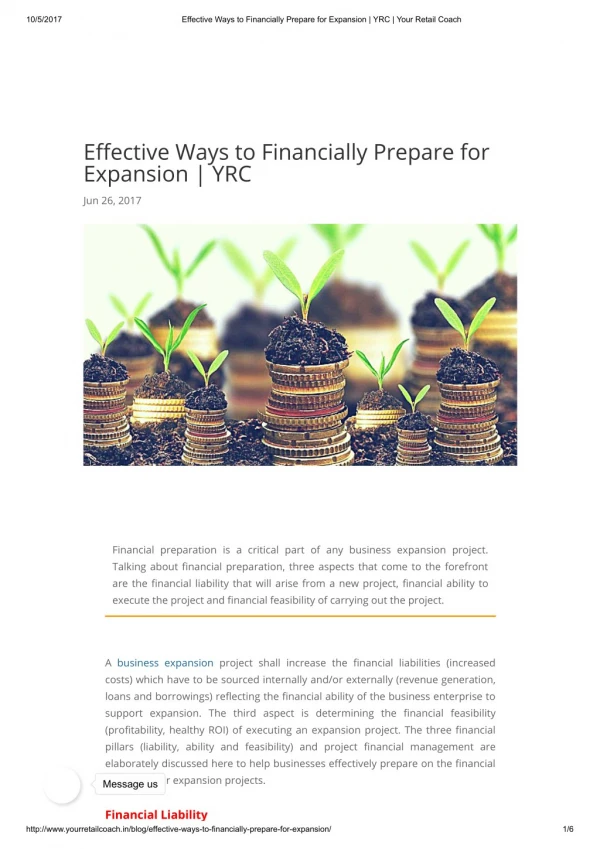

Ways to Prepare for an Audit. Legislative Division of Post Audit. Statewide Single Audit. Two parts to the SWSA Statewide Financial Audit Statewide A-133 Federal Compliance Audit LPA oversees the audit, but contracts with an external CPA firm. Know the Rules.

E N D

Ways to Prepare for an Audit Legislative Division of Post Audit

Statewide Single Audit • Two parts to the SWSA • Statewide Financial Audit • Statewide A-133 Federal Compliance Audit • LPA oversees the audit, but contracts with an external CPA firm

Know the Rules • Department of Administration Policies, Processes and Procedures • Generally accepted accounting principles

Know the Rules • Financial accounting resources • Codification of Governmental Accounting and Financial Reporting Standards by GASB • Audit and Accounting Guide: State and Local Governments by AICPA • Governmental Accounting, Auditing, and Financial Reporting by GFOA

Know the Rules • Grant award document • Applicable CFR • OMB Circular A-87 Cost Principles for State, Local, and Indian Tribal Governments • OMB Circular A-102 Grants and Cooperative Agreements with State and Local Governments (common rule)

Know the Rules • OMB Circular A-133 Audits of States, Local Governments, and Not-for-Profit Organizations • Compliance supplement

Complete the Forms Timely, Accurately, and Thoughtfully • Read the instructions carefully • Don’t add or delete columns – loads up into a database • Call if you have questions • Start early

SEFA Form • Report and correctly classify: • Non-monetary expenditures • Transfers to other state agencies • Awards to subrecipients • Clusters of programs • CFDA numbers • Reconcile the SEFA survey to the general ledger and to the reports

Work with the Auditors • Know who the key personnel in your agency are and have them available • Have documents ready • Answer questions fully and timely • If you don’t understand who or what the auditors want, ask • If you don’t think the auditors understand, persist in explaining to them • Err on the side of over-communicating.

Respond to the Findings • Read your findings carefully • Verify the accuracy of your findings • Share the findings with key stakeholders (program personnel, agency head) • Do the above as soon as you get your findings. Don’t wait until the corrective action plan is due

Respond to the Findings • If you disagree with the findings, think some of the information is inaccurate, or does not correctly characterize the situation, notify the auditors and Legislative Post Audit immediately • Thoughtfully craft your corrective action plan

Why Is This Important? • The state has received a material weakness for the past two years for not being able to accurately report capital assets

Why Is This Important? • The state had to re-issue the 2011 CAFR and related financial audit report because it did not include around $475 million in non-monetary revenues and expenditures

Why Is This Important? • The state has received a material weakness for the past two years for not being able to compile an accurate SEFA – reissued 2011 federal audit report • Missing non-cash items in 2011 • Missing and misreported information resulted in13 different versions of the 2012 SEFA

Why Is This Important? • Re-works take up your time • Auditors charge for time spent re-working because of mis-reported information • Because of SEFA problems, auditors worked hundreds of extra billable hours • Agencies pay for additional charges

Contact Information – Department of Administration • Martin Eckhardt (financial) martin.eckhardt@da.ks.gov 785-296-2661 • Gail Barnhart (financial and SEFA) gail.barnhart@da.ks.gov 785-296-3404 • Roger Basinger (SEFA) roger.basinger@da.ks.gov 785-296-8083

Contact Information – Legislative Post Audit • Legislative Division of Post Audit 800 SW Jackson St, Ste 1200 785-296-3792 • Julie Pennington, CPA, CIA, CFE Financial-Compliance Audit Manager julie.pennington@lpa.ks.gov 785-296-5817