Download

1 / 24

240 likes | 250 Views

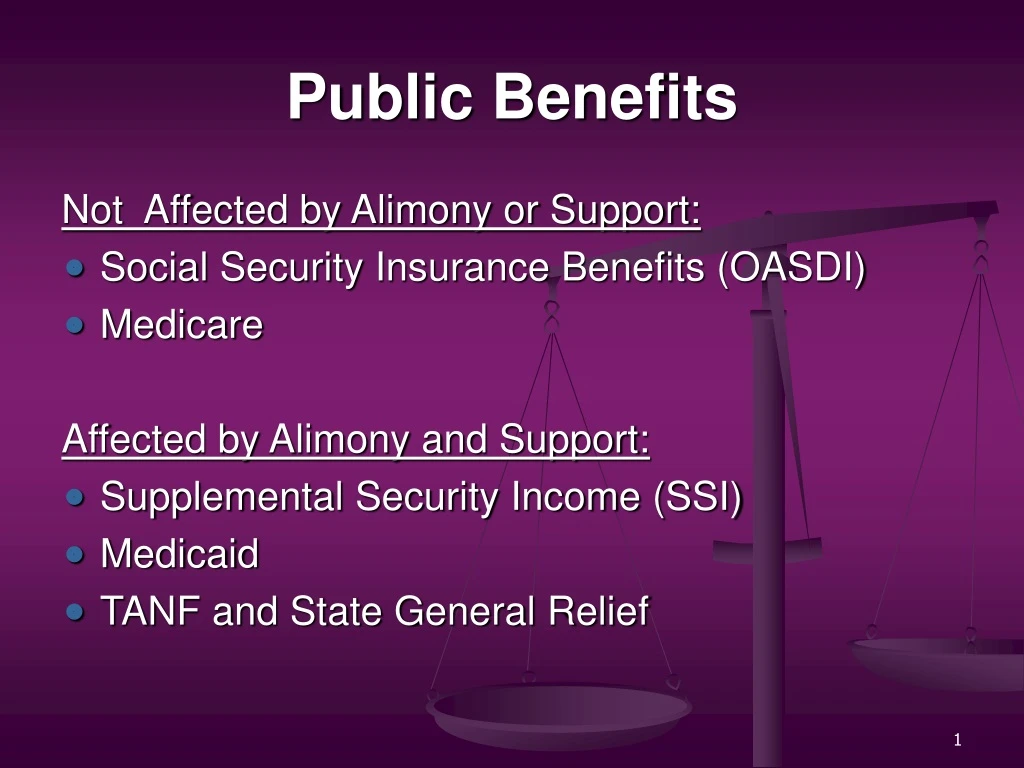

Public Benefits. Not Affected by Alimony or Support: Social Security Insurance Benefits (OASDI) Medicare Affected by Alimony and Support: Supplemental Security Income (SSI) Medicaid TANF and State General Relief. Social Security Insurance. Social Security Retirement (SSRI)

E N D

Public Benefits Not Affected by Alimony or Support: • Social Security Insurance Benefits (OASDI) • Medicare Affected by Alimony and Support: • Supplemental Security Income (SSI) • Medicaid • TANF and State General Relief

Social Security Insurance • Social Security Retirement (SSRI) • Social Security Disability (SSDI) • Social Security Dependents and Survivors Benefits

Social Security Insurance Must Have Insured Status as Worker • Gained by working and paying FICA taxes and earning quarters of coverage. • 40 quarters of credit for full coverage • Retirement Age 62 and over • Disability must begin within proximity to work coverage • Medicare Health Insurance Coverage

Social Security Insurance Dependent’s and Survivors Benefits • Child’s and Disabled Adult Child’s (DAC) Benefits • Disabled Widow or Widower Age 50-60 Benefits • Wife’s, Husband’s, Widow’s, Widower’s, Surviving Divorced Wife and Husband, Parent’s Benefits

Social SecurityDependents’ and Survivors’ Benefits Child’s Benefits • Child can be stepchild, adopted, or grandchild under certain circumstances • Child must be dependent upon parent • Unmarried • Under age 19, in elementary or secondary school • Parent must be currently receiving benefits or insured at time of death

Social SecurityDependents’ and Survivors’ Benefits Disabled Adult Child’s (DAC) Benefits • Same requirements as “child” except that child must have become disabled prior to age 22 and disability not have ended prior to receiving benefits • Unmarried, or married to SS Dependent or Survivor Beneficiary • If disability ends after benefits begin, child can become re-entitled to benefits if child becomes disabled again

Social SecurityDependents’ and Survivors’ Benefits Disabled Widow or Widower Age 50-60 Benefits • Survivor benefits for disabled surviving spouse of deceased worker • Individual must meet standard adult definition of disability • Individual must not be remarried prior to eligibility

SSDI, DAC, Widow(er) or SSI Disability • Inability to do any work based on physical and mental impairments • Must last 1 year or longer or result in death • Age, education, and prior work experience are factors • Five part analysis for disability

Medicare Health Insurance • Federal Health Insurance Program • Social Security Retirement age 65 and over • Social Security Disability 24 months and more • No waiting period for ALS and renal dialysis with disability • Part A, Part B, Part D • Monthly Premium for Part B ($93.50 in 2007) • Limited Coverage of Medical Services • Secondary To Private Health Insurance, but primary to Medicaid

Aged, blind, disabled No prior work record required Can be eligible for SS Insurance also Resource and income test Resources and income deemed to spouse or children under 18 living in household Automatic Medicaideligibility Supplemental Security Income

SSI Difference Between Resources and Income • Income is anything received from any source in the month being considered • A resource is anything that the individual owns or retains from one month to the next after the month of receipt

SSI Resource Limits • Resource limits: $2,000.00 for an individual $3,000.00 for a couple • Many resources are excluded from being countable.

Excluded Resources for SSI Examples of excluded resources include a personal residence, a vehicle, special items or devices needed due to medical condition, clothing, household items and personal affects of ordinary value, burial plot and burial contract, $1,500. in life insurance, retained retroactive SS benefits, and many more

SSI Definition of Income • Income is any item an individual receives each month in cash or on his or her behalf that could be used to meet needs for food or shelter • Countable income reduces the monthly benefit dollar for dollar unless it is specifically excluded

SSI Countable Income Examples • Wages or Royalties • Social Security Insurance • Annuity and Pension • Alimony • Two-thirds of Child Support • Dividends or interest • Prizes and gifts • Trust distributions • In-kind shelter or food • Income deemed from a parent or spouse

SSI Deemed Income • Income of parent living in household countable for eligibility until: • As soon as a child reaches age 18, parental deeming no longer occurs. • One-third of child support disregarded until age 18, or if the child remains a full time student in school up to age 22

Parent-to-Child Deeming – 2007 PARENTS’ INCOME TREATMENT: Allocation for non–SSI-eligible children living in the same household as the SSI-eligible child is $311. for calendar year 2007. Allocations are reduced by the non–SSI eligible child’s own income and the allocation is not available to a child who receives public maintenance assistance payments. In calendar year 2007, the federal benefit rate (FBR) for an individual is $623.

SSI In-Kind Income “In-kind” income is the provision of goods or services by a third party In-kind income providing food or shelter reduces the benefit up to a maximum limit of $227.67 (in 2007) each month

Court Process and Public Benefits • Court ordered divisions of property do not create benefit eligibility transfer penalties • Court separation or child support order, or divorce decree, not required to create division of households for benefit eligibility purposes • SSI follows state law in interpreting judicial orders for lawful division of property and countability • Court order putting income and resources into a SNT for benefit of recipient creates exclusion of countability until distributed

Effect of Child Support and Alimony on SSI Benefits • 100% of alimony is countable as income to spouse, and can also be deemed to eligible child • 2/3 of child support provided by an absent parent to child is countable until age 18, and 100% thereafter • In-kind alimony and child support for food and shelter reduces benefits up to $227.67 max. • Child support to ineligible sibling is not countable • If child relocates with other parent, benefits must be recalculated

Strategies for Benefit Eligibility with Child Support and Alimony • Facts are important! Each case is different • Only income and resources of recipient’s household are counted • All needs based benefit programs use income made directly to the recipient as an eligibility factor • Consider “in-kind” income distributions as generally being more favorable to program eligibility • Supplemental needs trusts can convert countable income and resources to a more favorable use • Medicaid and SSA could have different interpretations even though both use the same law

Additional Strategies • Home, vehicle, and household goods are not countable resources for any program • SSI rules allow transfers without penalty to spouse not living in household even though spouses income and resources not deemed to recipient • “In-kind” payments only cause limited reduction • Payment of loans reduce countable assets • Gifts only cause max. SSI 3 year disqualification

CASE EXAMPLE 1 • Robert, a 17 year-old child on SSI, recently became a child of divorce. The parents’ divorce decree orders the father to pay $726/month child support, but stipulates a dollar-for-dollar offset between SSI and child support. (We think the lawyers and court didn’t know that SSI was means-tested). So Dad intends to pay $103 per month ($726 - $623). • When mom reported the child support last August to SSI, SSI was initially reduced by $49. Reducing the SSI, of course, increased the dad’s support obligation by $49 which reduced SSI by another $32. In January, the caseworker asked to see the court order and counted the entire amount ordered and reduced the SSI by $464. ($726 – $242(one third) - $20 (disregard) = $464 countable income). Robert was assessed an overpayment of $2,400. • Robert’s mother wants the most money she can get to help raise her disabled child, regardless of the source. She wants her ex-husband to be assessed an arrearage for the full amount of $726/month back to August, and to pay the full amount of $726 going forward. • What alternatives do you present to her? Would you present different alternatives if Robert were 23 years old?