Download

1 / 7

70 likes | 110 Views

It’s important for borrowers to stay educated about the moral issues emerging in the hard money sector of the mortgage industry. Cory Ruppersberger aggregated a list of some key consideration that MUST be made before choosing the right type of mortgage loan. <br><br>For more details :- http://coryruppersberger.com/

E N D

Cory Ruppersberger Choose Right Mortgage Loan

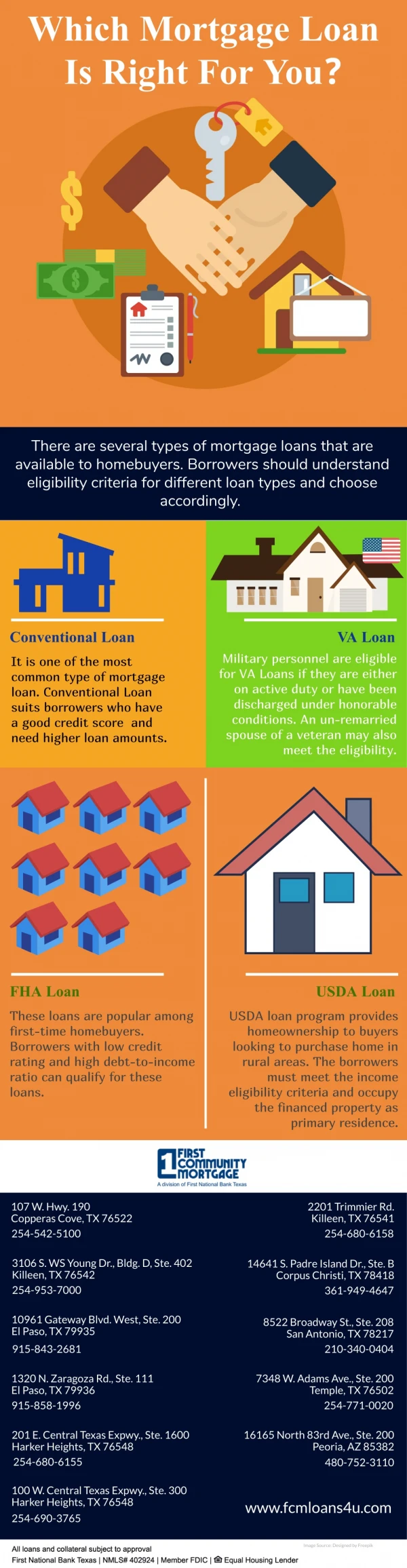

Right Mortgage Loan The mortgage industry has persevered through some turbulent times as of recent years and the current climate of the real estate lending keeps on creating worry among borrowers. Some private lending investors which are considered hard money lenders specialists, for instance, give an extraordinary return on investment to market investors, yet without proper verifying a borrower’s credentials. Furthermore, one can undoubtedly discover that not all lenders have their borrower’s best interest in mind. It’s important for borrowers to stay educated about the moral issues emerging in the hard money sector of the mortgage industry. Cory Ruppersbergeraggregated a list of some key consideration that MUST be made before choosing the right type of mortgage loan,

Licensing Requirements for Mortgage Lenders In today's business world, anybody can assemble a site, print some business cards, and open a company. Unfortunately, it’s become easier for lenders to offer such predatory loan products. Some hard money lenders and private capital investors have been offering real estate investors, promising financing capital for investment opportunities, in spite of not having the necessary licenses to do so. Before picking a hard money lender, always make sure to check your state's applicable department or the NMLS (National Mortgage Licensing System) for license information. If the money lender can't produce this required license information, look for a qualified professional! While you may have received an extremely luring offer, there's typically a catch – and you may lose application and appraisal fees by using a fraudulent lender.

Predatory Lending Practices - Check the Fine Print! Numerous borrowers especially the elderly, have received offers for home loans that tout "no installments for 12 months". These loans were commonly referred to as “negative amortization loans“. These loans looked to be appealing at first, as they clearly give the mortgage holder a "teaser payment period" to move in and adjust to the current monthly payment. In any case, what the lender neglects to disclose is that once the “teaser period” is over, the monthly payments adjust to an amount in excess of the borrower’s monthly budget. The borrowers may struggle to make the monthly payments, and within months, are falling into an undesirable foreclosure situation. Avoiding such consequences are simple, however, it requires a financial understanding to evaluate these fraudulent loan products. Most of these products have been eliminated by state and federal loan regulations but it is still important to evaluate the terms of your loan with the following questions. Can afford to make the payment if the loan will adjust? How many years is the fixed interest rate period for your loan? Make sure your loan originator provides you clear answers regarding your loan terms or find a lender that can summarize this information for you in a concise way.

Be Careful of Unscrupulous Tactics A lender offers you a loan to get a home. The payment on this home loan appears somewhat out of your monthly budget, yet you are so excited about owning your own home that you trust the loan originator when they say "We've investigated your financial accounts, and you can DEFINITELY qualify for this property." Why wouldn't you trust them? After All, it's precisely what you wanted to hear, isn't that so?

Loan goes to settlement and everything is great, right? Not so fast What you didn't know is that the loan originator KNEW that you couldn't afford the payment for this home. Many of these lenders have designed a loan program that forces you into foreclosure so they can retain the home for a profit!! State and federal regulators have been successful in prohibiting such lending practices in recent years, but it is important for you to ask for clear information from your lender on the terms of your loan so you can avoid this costly mistake. Before signing your name on a hard money loan, make sure to refer to these tips.