Download

1 / 25

250 likes | 382 Views

Electronic Funds Transfer EFT Overview. MHC Software, Inc. Jenny Mattson jennym@mhccom.com (800) 588-3676 ext. 227 (952)882-3327 (DID). Privately held, established in 1980 Located in Burnsville, MN Lawson, Oracle, Microsoft Business Solutions Business Partners.

E N D

Electronic Funds TransferEFT Overview MHC Software, Inc. Jenny Mattson jennym@mhccom.com (800) 588-3676 ext. 227 (952)882-3327 (DID)

Privately held, established in 1980 Located in Burnsville, MN Lawson, Oracle, Microsoft Business Solutions Business Partners. Provides Document Express, a payment solution with document printing and distribution capabilities. Also provides Image Express a document imaging and retrieval system. Over 600 client installations Local users include: Piper Jaffray, Holiday Companies, Lifetouch, Famous Daves, Allina, and many more. MHC Software, Inc.

Why Electronic Payments? Electronic payments are a smart business strategy. Save time and increase efficiency: Direct deposit helps you eliminate the manual, labor-intensive process of disbursing checks and improves the efficiency of your payment operations. Reduce costs: Fewer reissued checks Less accounting work - reconciliation is easier Lower production and administrative costs, reduced distribution and delivery expenses. Negotiate better terms with vendors Strengthen your cash management practices: Control the deposit date Elimination of delivery delays Reduced costs can make up for the loss of check float Improve employee benefits: On average, employees paid by check spend between eight to 24 hours each year going to the bank to deposit their paychecks. No delays accessing pay when employee is out sick or on vacation. Less of a disaster recovery concern

Payment Facts Provided by NACHA • Trend Info - in 2002, an estimated 80% of all business-to-business payments were still made by check. • The trend is moving more rapidly toward electronic payments • Approximately 14 billion payments were made in 2005 growing the ACH Network by 16.2% over 2004.

Consumer’s Beat out Business in EFT Consumer Direct Deposit Payments Alone were 4.4 billion paymentsin 2005. Business Payments The total number of business-to-business ACH payments grew to 2.0 billion in 2005, up 11.3 percent over 2004. Financial electronic data interchange - the electronic exchange of payment-related information or financial-related documents in standard formats between business partners on the ACH Network - grew by 19.8 percent in 2005. In 2005 there were 915 million EDI-formatted remittance records accompanying ACH payments. The number of financial EDI payments in 2005 was 255.6 million, up 20.3 percent over 2004.

Why is Business behind? • Payment related detail • New process – checks are familiar • How do I set it up? • What is the benefit? • Controls on the ACH Process • Check Float – the old argument – Check 21 changes that.

Payment Technologies Overview • Checks • Negotiable documents which include a MICR Line (Magnetic Ink Character Recognition). • Positive Pay • Check fraud prevention method offered by most banks where customer transmits a file of checks to the bank. • Advent of positive pay plus allows payee name to be transmitted to the bank • Ineffective if not transmitted on a regular basis • ACH (Automated Clearing House) • Electronic payments or credits completed in a standardized format that allow these payments to be made anywhere. • ACH payments include Direct Deposit of payroll, Social Security benefits and tax refunds, Direct Payment of consumer bills, e-checks, business-to-business payments, and Federal tax withholdings. • Wires • Electronic payments that are not revocable and can be done immediately (i.e. Real Estate Closings). Less exposure to risk than ACH for large dollar amount payments. https://www.nacha.org/OtherResources/riskmgmt/CORisk.pdf#search=%22wires%20vs.%20ach%22 Secure Seal – next slide

Secure Seal Used by the US Treasury for all payments – signature contains the seal.

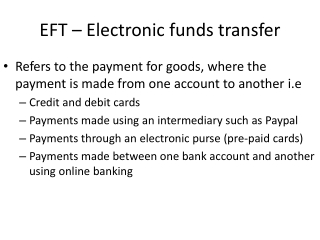

Definitions - EFT “Electronic Funds Transfer” is a generic name for electronic payments EFT International or Domestic • Settlement time is 1-2 days • ACH payments may be revoked for up to 60 days • NACHA Standards • Example: Direct Deposit ACH • International or Domestic • Usually require 5 days for settlement • Non-revocable payments • Example: Real Estate Closings Wires

EFT Components - Steps • Format payment files into NACHA layout. • Transmit payment files to the bank - ODFI (Originating Depository Financial Institute) • Send electronic remittance advices via email, fax, or web posting. Additional Features: • Provides reports • Accepts a return/confirmation file from the bank • File combining to reduce transaction costs. • Emails payment totals to funding department or bank.

ACH - Automated Clearing House • ACH: Electronic payments or credits completed in standardized formats that allow these banking transactions to be sent anywhere in the United States. • NACHA: The National Automated Clearing House Association – The trade association for the electronic payment associations, which establish the rules, industry standards, and procedures governing the exchange of commercial ACH Payments by depository financial institutions. • ACH Network: Funds transfer system governed by NACHA rules which provides the clearing of electronic entries for participating financial institutions.Virtually every major bank is affiliated with NACHA or works with a local clearinghouse.

The ACH Network • Five Participants in ACH Process: • Originator company or individual • ODFI • ACH Operator (FED) • RDFI • Receiver

ACH Types • PPD (Prearranged Payment and Deposit) • Designed for consumer accounts. • Used for Payroll, Pensions, Electric Bill, etc. • Allows for one Addenda Record • CCD (Cash Concentration or Disbursement) • Designed for simple electronic payments. • Allows for one Addenda Record. • When an addenda record is included this format is called the CCD plus. • Child Support payments are either CCD+ or CTX • CTX (Corporate Trade Exchange) • Designed for companies with trading partnership or used when sending payments to the government (I.e. child support payments). • Allows for 9,999 addenda records per ACH payment. • CBR (Corporate Cross-Border Payment) • This Standard Entry Class Code is used for the transmission of corporate cross- border ACH credit and debit entries. Allows cross-border payments to be readily identified so that financial institutions may apply special handling requirements for cross-border payments, as desired. • The CBR format accommodates detailed information unique to cross-border payments (e.g., foreign exchange conversion, origination and destination currency, country codes, etc.). • Addenda Records • Optional and they supply additional information about the Entry Detail Records or payment related detail. • The addenda record detail is machine-readable (EDI-Electronic Data Interchange). Each addenda record can be up to 80 characters. If the addenda record exceeds 80 characters than the data will wrap to the next addenda record. This allows for 800,000 bytes of data for each ACH payment in the CTX format.

File Transmission • Payment Files are sent to the ODFI (Originating Depository Financial Institution) • Modem • FTP with file encryption • Internet Transfer • Transmission options are bank dependent and may also be dictated by internal IT preferences. • MHC can provide any option. • Receipt of bank confirmation file. • Automatic email notifications available to funding department (i.e. Treasury, Accounting, etc.) • File combining to save on transaction costs.

ACH Automation ACH Process Bank CompliantNACHA ACHelectronic filetransmitted to bank Payment File Document Express can provide additional formatting (addenda records, headers, log in information, etc.) or simply automate the transmission process. Transmission options include: Modem, FTP or Internet Transfer

Document Express Remittance Delivery • Document Format • Document Security • User Controls • Reporting file import Printing Fax • Allows users to keep Financial System vanilla • MHC provides continuing compatibility with your Financials • Automatic interface to Financial System Email Web Posting

Document Express e-mail • Document Format • Document Security • User Controls • Reporting file import Email • E-mail to individual recipients • Encryption option for sensitive docs • SMTP and MAPI compatibility • Pulls current e-mail address from the Vendor Tables or a separate database.

Document Express Faxing • Document Format • Document Security • User Controls • Reporting file import Fax • Send reformatted documents to Fax Server. • Fax number comes from output file, Vendor Tables, or alternate database.

Document Express Web Posting • Document Format • Document Security • User Controls • Reporting file import Web Posting • Post documents to a Web Site, restrict access to documents via username/ password, customized filters and search criteria.

Company Considerations Prior to Implementing EFT • Business terms • Payment methods • Remittance information distribution • Security of transactions • Notice of change handling • Vendor data collection • Audit trails • Accountability • Process management

International ACH Considerations • Internationally not all countries have an ACH-like clearing system, and those with clearing systems have different settlement times and formats. So know the rules. • Foreign Bank Accounts are no longer required. • What currencies are you dealing with? Are multiple currencies used? • Are ACH reversals allowed? • Is pre-notification available? • Be aware of that different bank holidays can affect the dates the money is deposited into foreign accounts. • Make sure to understand the MICR Line or account information when setting up the Customer account information in the ERP system. • Additional resources at: http://www.frbservices.org/Retail/intfedach.html

The Future of Payment Technologies • Steady increase in ACH business to business payments • EDI becoming more standardized and mainstream • Increased cost of check processing as electronic business grows • Expanded ACH offerings including International ACH payments • XML emerging to supplement EDI • Increased government requirements – Child Support.

Child Support Payments • Employers provide 70 percent of all child support collections, states encourage employers to remit those payments electronically. In fact, Illinois, Indiana, Florida, and Massachusetts have passed legislation requiring specific employers (of a certain size or remitting a certain number of payments) to remit electronically. • Ohio is mandating electronic payments this fall. • States may also set up a Web-based payment service to attract the small- to medium-sized employer who otherwise would continue to remit by paper check. • Options run through PR with Customized Process run interface to AP.

Questions Document Express Software Demonstration Electronic Payments Jenny Mattson (800)588-3676 Ext. 227 Jennym@mhccom.com