Download

1 / 32

320 likes | 329 Views

LOS 1 Introduction to the Management of Working Capital. Learning Outcome Statement (LOS).

E N D

Learning Outcome Statement (LOS) • Experience shows that the inadequate planning and control of working capital is one of the more common causes of business failure. And yet the management of working capital is a neglected subject which has been all too little investigated or written about. • Major advances have been made in developing new techniques for long-term investment and financial decisions; but far less attention has been paid to the short-term capital requirement. • This chapter demonstrates some of the ways of analyzing the subject and ends with a discussion of the need for an adequate provision of working capital.

Introduction • The financial management of business firms involves three functions: • The management of long-term assets (capital budgeting) • The management of long-term capital (capital structure) • The management of short-term assets and liabilities (working capital management)

The Balance-Sheet Model of the Firm The Capital Budgeting Decision Current Liabilities Current Assets Long-Term Debt Fixed Assets 1 Tangible 2 Intangible What long-term investments should the firm engage in? Shareholders’ Equity

The Balance-Sheet Model of the Firm The Capital Structure Decision Current Liabilities Current Assets Long-Term Debt How can the firm raise the money for the required investments? Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity

The Balance-Sheet Model of the Firm The Net Working Capital Investment Decision Current Liabilities Current Assets Net Working Capital Long-Term Debt How much short-term cash flow does a company need to pay its bills? Fixed Assets 1 Tangible 2 Intangible Shareholders’ Equity

The Role of Working Capital Sales Inv A /R Cash

The Cash Flow Timeline • Order Order Sale Payment Sent Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • Time ==> • Accounts Disbursement • < Payable > < Float > • Invoice Received Payment Sent Cash Disbursed

What is Working Capital? • Working capital refers to the cash a business requires for day-to-day operations, or, more specifically, for financing the conversion of raw materials into finished goods, which the company sells for payment. • Among the most important items of working capital are levels of inventory, accounts receivable, and accounts payable. • The working capital is calculated as: Working Capital = Current Assets – Current Liabilities. • Positive working capital means that the company is able to pay off its short-term liabilities. Negative working capital means that a company currently is unable to meet its short-term liabilities with its current assets.

What is Working Capital? • Current Assets include: • stock or inventory (raw materials + work-in progress + finished goods) • debtors (unpaid bills for which the profit has already been realized) • trade credit (from suppliers) • cash in hand • short-term securities • Current Liabilities include: • monies owing to trade creditors (mainly for raw materials) • bank overdrafts • other short-term loans • outstanding tax, dividend and interest obligations

What is Working Capital? • Current AssetsCurrent Liabilities • Cash Accounts Payable • Marketable Securities Notes payable • Account receivables Accruals • Prepaid expenses Current long-term debt • Other Current assets Other current liabilities Long-Term Assets Long-Term Financing Fixed Assets net of depreciation Long-term accruals Other assets Long-term debt Equity financing Total Assets Total Debt & Equity Capital Fig: A Typical Firm’s Balance Sheet Working capital Accounts

What is Working Capital? • If a company's current assets do not exceed its current liabilities, then it may run into trouble paying back creditors in the short term. The worst-case scenario is bankruptcy. • A declining working capital ratio over a longer time period could also be a red flag that warrants further analysis. • For example, it could be that the company's sales volumes are decreasing, and as a result, its accounts receivables number continues to get smaller and smaller.

What is Working Capital? • Working capital is a measure of a company's efficiency and its short-term financial health. • For example, if a company is not operating in the most efficient manner (slow A/R collection), it will show up as an increase in the working capital. This can be seen by comparing the working capital from one period to another; slow collection may signal an underlying problem in the company's operations.

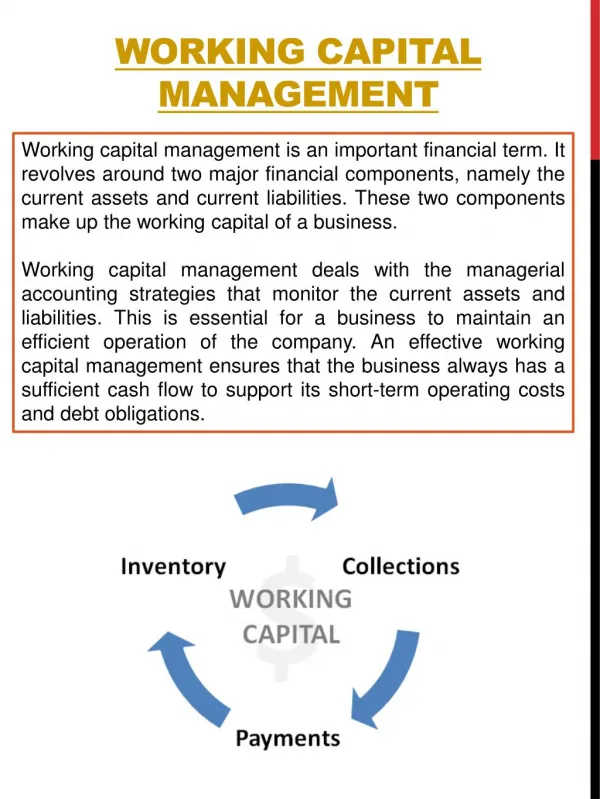

What is Working Capital Management? • Working capital management is a managerial accounting strategy focusing on maintaining efficient levels of both components of working capital (current assets and current liabilities) in respect to each other. • Working capital management ensures a company has sufficient cash flow in order to meet its short-term debt obligations and operating expenses. • A few key performance ratios of a WCM system are: working capital ratio, inventory turnover and the collection ratio. These ratio analysis will lead management to identify areas of focus such as cash management, accounts receivable management, inventory management, and account payable management.

What is Working Capital Management? • The management of working capital is concerned with the management of the assets and liabilities in the top half of the balance sheet. • We will analyze decisions such as: • How should the firm manage its cash? • To whom should the firm grant credit? • How much inventory should the firm keep? • What should be the composition of the firm’s current debt?

Objectives of Working Capital Management • The two main aims to be satisfied by the working capital manager are profitability and liquidity. • Investments, in current as well as long-term assets, should be undertaken if they will offer the most satisfactory returns to shareholders – measured by net present values discounted at the cost of capital. • The goal of liquidity is designed to ensure that the firm can satisfy its financial obligations and continue as a going concern.

Objectives of Working Capital Management • The two goals of profitability and liquidity frequently conflict with one another. Attempts to produce the maximum profitability out of the various elements of the working capital can create severe liquidity problems. At the same time, over-concentration on liquidity can water down profits. • A major function of decision making for working capital is the management of the various working capital accounts with regard to the firm’s level of liquidity: NOT TOO MUCH LIQUIDITY AND NOT TOO LITTLE LIQUIDITY. • Management means establishing the best possible trade-off between the profitability of the net current assets employed and the ability to pay current liabilities as they fall due. This latter implies a clearly defined risk policy to determine the required liquidity level.

Importance of Working Capital Management • There would be no need of holding cash for working capital other than for the initial costs, because it could be possible to make the payment from every receipt of sales. • Likewise, there would also be no need for receivables and payables if customers pay cash immediately and the firm would also make its payments promptly. • However, problems of working capital exist because these ideal assumptions are never realistic and therefore working capital levels make a significant part of a firm’s investment in assets and these assets have to be financed implying that investments may have benefits as well as costs.

Importance of Working Capital Management • The management of working capital plays an important role in maintaining the financial health of the firm during the normal course of business. • The following figure portrays the flow of resources through the firm. By far the major flow, in terms of its yearly magnitude, is the working capital cycle. • The loop starts at the cash and marketable securities account, goes through the current accruals accounts as direct labor and materials are purchased to produce the inventory, which is in turn to sold and generates accounts receivable, which are finally collected to replenish cash. • In the following figure, a square is a balance sheet account and an arrow indicates a flow.

Importance of Working Capital Management Used in Production process Used in Working Capital Cycle Used to purchase Generates Used to purchase Via Sales Generates Collection Processes External Financing Used to purchase Returns to capital Accrued Direct labor and material Accrued Fixed Operating Expenses Cash and Marketable Securities Inventory A/R Fixed Assets Suppliers of capital

Importance of Working Capital Management • Implementing an effective working capital management system is an excellent way for many companies to improve their earnings. • Working capital consists of a large portion of a firm’s total investment in assets. It amounts usually to 40 percent in manufacturing industries and 50% - 60% in retailing and wholesales (Moyer, Mcguigan and Kretlow, 1995). • By minimizing the amount of funds tied up in current assets, firms are able to reduce financing costs and/or increase the funds available for expansion. • Therefore, the importance of efficient working capital management is indisputable in business.

Importance of Working Capital Management • By implementing best practices in working capital, companies can strengthen strong cash flow levels, improve profitability, budgeting and forecasting process, predictability and manageability of results, heighten risk visibility and reduce reaction time. • Scherr (1989) considering the importance of WC found that managers spend much of their time in activities directly or indirectly related to working capital investments and short-term debts. Survey evidence shows that 60% of a financial manager’s time is spent on decisions related to working capital management. • The management of working capital plays an important role in maintaining the financial health of the firm during the normal course of business.

Importance of Working Capital Management • Besides this basic and continuing reason for the importance of working capital management to the firm, several developments in the late 1970s and early 1980s led to increasing concern for the management of these accounts. • For example, level of interest rates that climbed extremely high by historic standards, caused the financing of investments to become more costly. Deregulated money markets provided financial managers with access to many instruments for short-term financing and investment. • Together, these developments kept corporate treasurers seeking new and better ways of managing individual working capital accounts to balance the firm’s overall liquidity position.

Managing Working Capital Crisis • Present-day industrial organizations are confronted more and more with a shortage of working capital with which to run their units at an economical level of operation. • With the ever increasing rate of inflation, associated with an increase in the cost of capital and more demands for resources due to rapid industrialization, with a consequent credit squeeze policy adopted by the banks and financial institutions, the management of working capital has assumed great significance recently. • In many organizations the technology adopted may not be so advanced, resulting in lower operational efficiency, uneconomical costs and a longer manufacturing cycle time.

Managing Working Capital Crisis • The working capital needs of an organization depend on a multitude of factors, such as operating level, level of operational efficiency, service level, inventory policies, book debt policies, etc. • Financing is based on the extent of internal cash generation, the availability of credit limits, minimum margin stipulations, the relative cost effectiveness of different sources of financing, etc. • All factors are time dependent and are dynamic in nature. To deal with many interacting variables of a dynamic nature in an integrated manner, cause and effect analysis using a system dynamics technique could be of great assistance in formulating strategies for effectively managing working capital to overcome the crisis.

Formulating Appropriate Strategies • To tide the organization over the working capital crisis and to further improve its financial position some short- and long-term strategies need to be adopted. • Short-term strategies should meet the immediate challenge of the working capital crisis. However, the scope of such strategies may be restricted. • To manage working capital more effectively, long-term strategies may have to be adopted to reduce the working capital needs of the organization, to increase its level of operation and, consequently, to generate more and more funds, to finance working capital requirements.

Short-Term Strategies • Gearing up book debt collection efforts by adopting more stringent follow up methods, offering discount to the customers against prompt payment. • Restricting credit policy • Operating more and more with customers‘ materials, thereby reducing the inventory level • Reducing the service level • Slashing developmental expenditure over the short-term — cutting back on its R&D budget, training and development budget or product promotional expenditure, etc. • Improving profitability through short-term measures like improving capacity utilization through letting out facilities, exploiting demand by subcontracting, negotiating with the bank for softer terms and higher credit limits. • Negotiating with the creditors like deferring payment to creditors, converting the loan into equity, etc.

Long-Term Strategies • Reducing the working capital needs • Reducing the inventory holding requirement • Improving product quality & then demanding restricted credit terms • R&D efforts leading to improved operational efficiency • Cost reduction through higher capacity utilization • Improving capacity utilization • Removing input constraints • Plant modernization and improvement for higher plant availability • Capacity expansion • Quality control efforts • Product promotion

Working Capital Management Practices in Bangladesh • There are a few studies on working capital management in Bangladesh covering both public and private sectors including several multinational companies (MNCs). • Mohiuddin (1983) has conducted a study on cash budget and concluded that effective cash budgeting minimizes the liquidity problems. • Islam and Rahman (1994) have identified the working capital trends of some selected enterprises in Bangladesh.

Working Capital Management Practices in Bangladesh • Sayaduzzaman (2006) has conducted study on British American Tobacco Bangladesh Company Ltd. and found that the working capital management practices of the company is highly satisfactory due to efficient management of inventory, debtors, cash balances and working funds. • Chowdhury and Amin (2007) has conducted a study on pharmaceutical industry and concluded that pharmaceutical firms operated in Bangladesh are efficiently deal with their liquidity preferences and investment criteria and this is due to the competitive nature of this industry.

Working Capital Management Practices in Bangladesh • The studies conducted in Bangladesh on working capital management is either company specific (Islam and Rahman, 1994; Sayaduzzaman, 2006) or at best industry specific (Zaman, 1976; Zaman, 1991b; Zaman, 1991c; Chowdhury and Amin, 2007). • There is no such study of evaluating working capital management performances of a large sample of manufacturing ventures in Bangladesh. • One such study has been conducted by Siddiquee and Khan (2009) covering 83 companies (total 414 observations) from different sectors enlisted with the Dhaka Stock Exchange (DSE) Ltd. during the stipulated period of 2003-2007.

Working Capital Management Practices in Bangladesh • Another study on the working capital management practices, commissioned by Siddiquee and Hossain (2009) is underway covering a large sample size of 243 manufacturing companies from different sectors. • The sample includes companies from the sectors: Cement, Ceramics, Engineering, Food and Allied, Fuel & Power, ICT, Jute, Leasing, Leather, Miscellaneous, Paper & Packaging, Pharmaceuticals & Chemicals, Services & Real Estate, and Textile.