Download

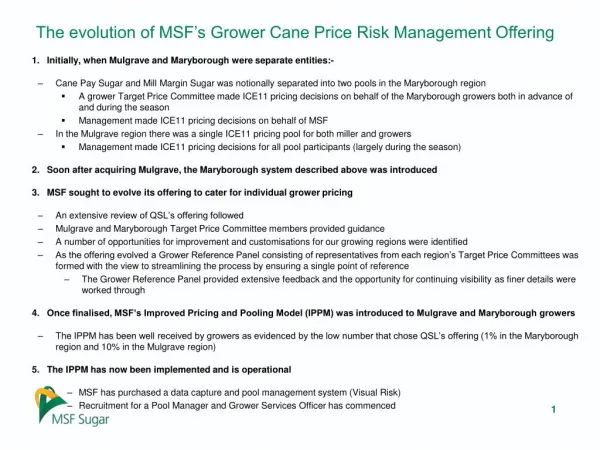

1 / 14

140 likes | 240 Views

ABN AMRO. Price of Risk. Ton Vorst Global Head of Quantitative Risk Analytics October 7, 2005. Quantitative Risk Analytics. Staff: 56(roughly 50% Ph-D’s) Most in Amsterdam (roughly 25% foreign). Some in London and New York

E N D

ABN AMRO Price of Risk Ton Vorst Global Head of Quantitative Risk Analytics October 7, 2005

Quantitative Risk Analytics • Staff: 56(roughly 50% Ph-D’s) • Most in Amsterdam (roughly 25% foreign). Some in London and New York • Activities: Validation of Trading Models, Credit Portfolio and Counterparty Risk Models, Quantitative consultancy • After a while people move to other positions within ABN AMRO

Other Positions within ABN AMRO • Development teams for trading models • Asset Management and Asset Allocation • Department of Economics • Developers of rating models

ABN AMRO Career Career Development Programs. • Introduction Course (+/- 6 weeks) • Industry conferences / courses

Financial instruments Product Analysis within QRA Equity (stock: KPN, Shell, IBM,…; indices: AEX, DJ, Nikkei) • Currency (Foreign Exchange, FX) • Interest rates (Bonds, LIBOR) • Commodities • Derivatives: Futures, Options

ABN AMRO Wereldwijd KoopkrachtGarantie Note 2005-2015 EUR 100,000,000 Capital Protected Securities Linked to the Performance of an Inflation Index and Basket of Indices, due 2015 • 125% of your investment • Equal purchasing power of your investment • 75% of market rise + your investment back Best of

ABN AMRO Wereldwijd KoopkrachtGarantie Note 2005-2015 • The purchasing power of your investment HICP - Harmonised Index of Consumer Prices excluding Tobacco 20%

ABN AMRO Wereldwijd KoopkrachtGarantie Note 2005-2015 • 75% of Market Rise Basket value

Option Option payoff Gain/loss Option 100% Stock Stock value Stock value 100 100 -100% Three types of financial instruments: • Bank account (virtually risk-less) • Share (moderate risk) • Option (very risky)

Risk neutral valuationOne step binomial model S(1)=110 V(1)= 5 S(0)=100 V(0)= ? S(1)=90 V(1)= 0 • We create a portfolio: • A number of shares, Δ • Sell one option with strike 105 and unknown value V(0) • The value of the portfolio P(t) = Δ·S(t) – V(t) • Find Δ such that value of portfolio, P(1), is independent of the stock value • Stock goes UP: P(1) = Δ·110 – 5 • Stock goes DOWN: P(1) = Δ·90 – 0 • UP = DOWN follows Δ·110 – 5 = Δ·90 and Δ = 0.25 • P(1) = 22.5 • Risk-less portfolio must earn the risk-free interest rate, say 5% per year • Portfolio value today is P(0) = 22.5/e0.05×1 = 21.4 • Option value today V(0) = 0.25·100 – 21.4 = 3.6

Risk neutral valuationRisk neutral world • Risk neutral valuation can be generalized: • We can assume that all assets grow with the risk-free interest rate, if we can hedge all risks • Mathematically, this corresponds to using a “risk free measure” • Put it in a mathematical form where r is the risk free interest rate. The risk free interest rate is used to calculate a future value and to discount them.

Mathematical methods • Trees (binomial, trinomial) S(1)=121 V(1)=16 • Monte Carlo S(1/2)=110 V(1/2)= 9.8 S(1)=99 V(1)= 0 S(0)=100 V(0)= 6.0 S(1/2)=90 V(1/2)= 0 • Partial differential equations S(1)=81 V(1)= 0 • Analytical solutions (Black-Sholes equation, for example)

References • Probability theory • Stochastic calculus • Measure theory • C++, MATLAB,… • John Hull, Options, Futures, and Other Derivatives • http://www.wilmott.com (Forums)

ABN AMROQuantitative Risk Analytics Group Market Risk Management Quantitative Risk Analytics Ton Vorst Market Risk Modelling & Product Analysis Credit Risk Modelling & Product Analysis Quantitative Consultancy & Operations Research