Download

1 / 22

220 likes | 536 Views

The Evolution of the CMBS Market. CRE Annual Convention – Maui, HI October 23-26, 2006. I. Historical Overview. Historical Overview - CMBS. First recorded CMBS transaction – 1985 CMBS prominence grew following RTC transactions in the early 1990s

E N D

The Evolution of the CMBS Market CRE Annual Convention – Maui, HI October 23-26, 2006

Historical Overview - CMBS • First recorded CMBS transaction – 1985 • CMBS prominence grew following RTC transactions in the early 1990s • S&L crisis in early ’90s RTC formed to liquidate assets • Liquidity shortage – Wall Street steps in to pool performing and non- performing loans • In 1995, total CRE loans outstanding was $1.014T and CMBS represented 5.4%. • In 2005, total CRE loans outstanding was $2.618T and CMBS represented 19.9%. CMBS represented 37% of all CRE loans originated in 2005 ($460B). • Types of transactions – conduit, fusion, single borrower / asset, floating rate, agency. Conduit and fusion made up approximately 72.7% of all CMBS transactions in the US in 2005. Source: Commercial Mortgage Alert, Wachovia Securities and Mortgage Bankers Association

Historical Overview - CMBS Source: Commercial Mortgage Alert

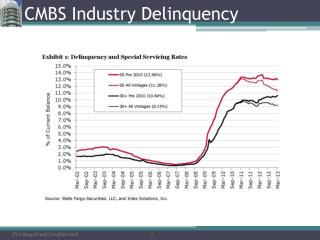

Historical Overview - CMBS • Investors – B-piece buyers and Investment grade • B-piece buyer – CRE savvy – first loss position • Investment grade – Institutional investors, insurance companies, money managers, pension funds, banks • Typically, European investors are more focused on floating rate transactions / bond classes and US investors purchase more fixed rate product • Short duration – match assets to funding sources • Utilize currency hedges and would rather not put on interest rate swaps in addition to currency hedges • Delinquency performance over the last 10 years has been strong with a current delinquency rate across all CMBS deals of 0.51%. • Reasons for low delinquencies despite higher IR and market fundamentals being weaker • Strong capital flows • Borrowers willingness to accept lower cap rates

Historical Overview - CMBS Source: Lehman Brothers – Lehman Live

Historical Overview - CMBS Source: Lehman Brothers – Lehman Live

Historical Overview - CDO • Re-REMICs and CDOs have been utilized for the past 10+ years on corporate bonds. • CRE Re-REMICs were first utilized in the mid 1990s • The first CRE CDO was in 2001. Since 2001, CRE CDO and other CDO products (synthetics) have exploded with popularity and have heavily impacted credit in the CRE origination market. • Re-REMIC v CDO • Re-REMIC: tax efficient structure, REMIC bonds only, static structure, US issuer only, very inflexible • CDO: all types of collateral permitted, off shore issuer, static or managed pool, ramp allowed, reinvestment allowed, call options allowed, very flexible

Historical Overview - CDO Source: Commercial Mortgage Alert

CMBS Process • CMBS loan versus a portfolio loan • Pricing versus flexibility • Overview of CMBS Process • Originate commercial mortgage loans on properties – typically non-recourse lending • Accumulate a pool of loans • Present pool to rating agencies to obtain bond structure • Present pool to B-piece investors for bid and select B-piece investor for due diligence • Finalize pool with B-piece investor and rating agencies and circulate prospectus to investors • Sell investment grade bonds • Contributors include commercial banks, investment banks, insurance companies, finance companies

CMBS Process • Contributors team up to: • Grow the size of the deal • Enhance market liquidity • Serve as market benchmarks • Increase turn over velocity to increase ROE. • Prepayment risk reduced with YM and defeasance. • Benefits to Issuer • Move loans off balance sheet and free up capital • Increase ROE by selling loans on a regular basis • Provide another loan product to meet clients needs

CMBS Process • Challenges in today’s market • Lack of amortization • Lack of structuring • Increased leverage • Return of esoteric property types • Increased loans in tertiary markets • Single tenant loans • Increased hospitality concentrations • TICS and DST borrower structures • Cap rate and interest rate disconnect • “Believe in the upside story”

CDO Process • Overview of CRE CDO Process • Originate or acquire various types of collateral • CMBS bonds, mezzanine debt, B-notes, whole loans, synthetics • Accumulate collateral to meet specific / desired diversification targets • Present pool to rating agencies to obtain bond structure • Static versus managed pool • Pools are static or managed, with or without ramp periods and reinvestment allowed • Negotiate with rating agencies to obtain the desired coverage test requirements • Determine the asset manager – normally the issuer • Sell investment grade bonds, issuer usually retains the equity piece • Contributors include commercial banks, investment banks, insurance companies, finance companies, REITs, etc.

CDO Process • Investors of CDOs include financial institutions, insurance companies, money managers and “others” • Through 2005, there were over 100 institutional investors in the US and abroad • 55% of investors are domestic and 45% are overseas – primarily UK and Germany • Benefits of CDOs • Match term funding • No mark-to-market risk • Cheaper source of financing • Increase assets under management and fees

CDO Process • Other attributes of CDOs • Motivation typically either: • Assets Under Management (AUM) - fee driven motivation, lower credit leverage collateral assets, sell portion of the preferred shares. Typically done by Money Managers. • Financing – seek match term funding, non-market to market (alternative to repo), retain preferred shares. • Issuers are typically RE Funds, Mortgage REITs, and B-piece buyers. • All collateral assets are rated or shadow rated • Generally limited to current pay assets Source: Wachovia Securities

CDO Process • Capital structure determined by rating agency–expected default and recovery values on collateral • Typical leverage of 20-25x for AUM deals, 3-10x for Financings • Other issues: on or off balance sheet, QSPE or SPE; may impact ability to manage Source: Wachovia Securities

CDO v CMBS • CDO: • Issuer: Cayman Island Trust • Able to hold non-mortgage assets: • Unsecured debt (e.g. REIT debt) • Mezz, Preferred Equity • Derivatives (e.g., swaps, caps, CDS) • Able to issue classes as fixed or floating • First, second or multiple re-securitization of assets • Offers manager flexibility (e.g., static vs. managed, mixed sector, ability to take views on credit), may or may not be fully ramped at closing • Collateral quality tests (if managed) • Excess spread goes to equity • Structural protections: • Subordination • OC and IC Triggers (no principal write-downs) • Collateral quality tests • Offers ongoing management fees • Global buyer base • First loss class: • Excess cash flow class • No principal write-downs • Cash flow can turn on, off and on CMBS: • Issuer: Real Estate Mortgage Investment Conduit (REMIC) • Trust required to hold only mortgage loans: • No unsecured debt • No derivatives contracts, no substitution of assets • Generally issues debt of similar basis as assets (e.g., fixed – fixed; floating – floating) • First securitization of asset • Static pools only, 100% ramped at closing, no manager involvement post closing • Excess spread sold as Interest Only (IO) Bond • Structural protections: • Only subordination (principal write-downs) • No ongoing management fees • Primarily domestic buyer base (fixed rate) • First loss class: • Fixed coupon • Principal write-downs via: • Appraisal reductions • Realized losses • Cash flow shuts off permanently upon 100% write-down. Source: Wachovia Securities

Future of CMBS & CDO • CMBS FASB issues • Liquidity • Origination • Investments • CDO replacing CMBS? • Synthetic CDOs • Continued growth • United States / Canada • Europe • Stock market