Download

1 / 19

190 likes | 222 Views

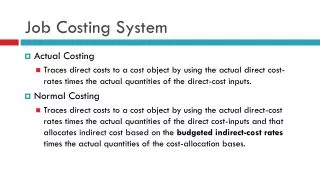

JOB COSTING SYSTEM. Presented by: GROUP # 5 Michael A. Aceves Kiet T. Diep Alan E. French Shasha Guan Noela Ieong Sara Zarineh. Job Costing System . a Job is an individual product or batch for which a company needs cost information.

E N D

JOB COSTING SYSTEM Presented by: GROUP # 5 Michael A. Aceves Kiet T. Diep Alan E. French Shasha Guan Noela Ieong Sara Zarineh

Job Costing System • a Job is an individual product or batch for which a company needs cost information. • Companies that produce individual products or batches of products that are unique use a job costing system. • Example : Boeing Company

Symbols means… • A document or report: the document may be prepared by hand or printed by a computer. • The online keying: data entry by online devices such as a terminal or personal computer. • Magnetic disk: data stored permanently on a magnetic disk; used for master files and databases.

Continuous… • Off-page connector: An entry from, or an exit to, another page. • Computer processing: A computer-performed processing function; usually results in a change in data or information. • Display: Information displayed by an online output devise such as a terminal, monitor, or screen. • Auxiliary operation: A processing function done by a device that is not a computer.

Section 1: Direct Labor Cost • The document which is used to trace direct labor cost to production is called a time ticket. The time ticket indicates how much time was spent on which job by which employee. Note that when several employees all work on the same job, the time card data will be aggregated and then applied to each job. Direct Material Cost • The document used to request the release of materials to production is called a materials requisition. This requisition indicates the type, quantity and cost of material as well as the job number to which it will be assigned.

The Production labor transaction file contains payroll information (information from the time cards or labor tickets). • The Materials issuance transaction file is made up of information from materials that are requested and ordered. • In step 2, the Production labor transaction file, and the Materials issuance transaction files are merged, to create the Production cost transaction file. The information in the Production cost transaction file is based on actual cost and not estimated cost.

The costs from the actual production cost transaction file are printed and displayed as information on two separate documents. These documents are (1) the materials and labor usage report, and (2) the scrap and lost time report. • These reports will give its reader (probably a supervisor or someone in a managerial capacity) an idea of what materials were used, how much labor was used, the amount of scrap that came out of the project during its construction, and the amount of time lost during the building phase. Also, the scrap and lost time report should say why time was lost, how much was lost, and why there was scrap material.

Section 4: The computer accesses the production cost transaction file, which includes all production costs, and distributes the costs amongst the manufacturing overhead file and the open-job file.

Section 5: Manufacturing Overhead File:Includes all costs necessary for the production of goods, but which cannot be tied to specific goods themselves. This includes indirect labor, indirect materials, property tax, insurance, heat and light. Determining of factory overhead costs is more complicated because the cost accountant cannot calculate total actual factory overhead costs for an accounting period until it ends.

Applied overhead is the amount of overhead assigned to WIP as a result of incurring the activity that was used to develop the application rate. Application is made using the predetermined rates and the actual level of activity.

Overhead Analysis: Analyzing the individual overhead cost factors will show all cost factors in terms of the fixed and variable values. Such a detailed analysis can be summed and restated as a total cost flexible budget formula that would allow total costs at all activity levels to be computed.

Section 6: The files from the open job file (working in progress) database can be displayed or accessed on an online output devise such as a terminal, monitor, or screen through job status query. Also, the files from the open job file database can be printed which will produce a document called job status report, which can be viewed by the management.

Section 7: The actual production cost transaction files database and budgeted standard cost file database are both accessed in order to perform standard cost variance analysis, which is a process in order to produce a document called standard cost variance reports. The standard cost file database is also been accessed along with actual manufacturing overhead file database to perform the over head application process.

Using Variance Analysis to Control Costs Compute Variance No No Corrective Action Needed Is the Variance Result Significant? Yes Determine Cause(s) of Variance Identify, and Analysis Performance Measures to Determine Corrective Action Take Corrective Action

Conditions can lead to improper job costing: • Misstating the stage of completion. • Charging costs to the wrong Job. • Misrepresenting the cost of jobs. • Intentional misrepresentation in contracts

Ways to improve inventory subprocess • Barcodes: is a pattern of parallel bars and spaces carrying information in the relative widths of these features. Bar codes represent data in a machine-readable form, and are one of the most efficient means of capturing data automatically. • Real Time Locating System (RTLS):uses battery-operated radio tags that lasts 5 years and a cellular locating system to detect the presence and location of the tagsanywhere from 50 to 1000 ft • Acousto-Magnetic (AM) tags:small, self adhesive labels with simulated barcode to deceive shoplifters which can be deactivated at the point of sale at the counter; used to protect any non-metallic products • Radio Frequency (RF) labels: paper thin, self adhesive labels with simulated barcode which can be deactivated at the point of sale at the counter, like AM tags but much more preferred by retailers due to more system choices to compliment store layouts, more label choices than and a lower investment • Radio Frequency Identification (RDIF): consists of an antenna, an transponder (RF tag) and transreceiver (decoder); the antenna emits radio signals to activate tag and read and write data onto it, transreceiver and transponder acts as a reader which emits radio waves ranging from 1 inch to 1000ft or more so when tags pass through electromagnetic zone it detects the readers signal, and reader decodes data in silicon chip then passes to host computer for processing

The End Special Thanks to: Michael A. Aceves Kiet T. Diep Alan E. French Shasha Guan Noela Ieong Sara Zarineh