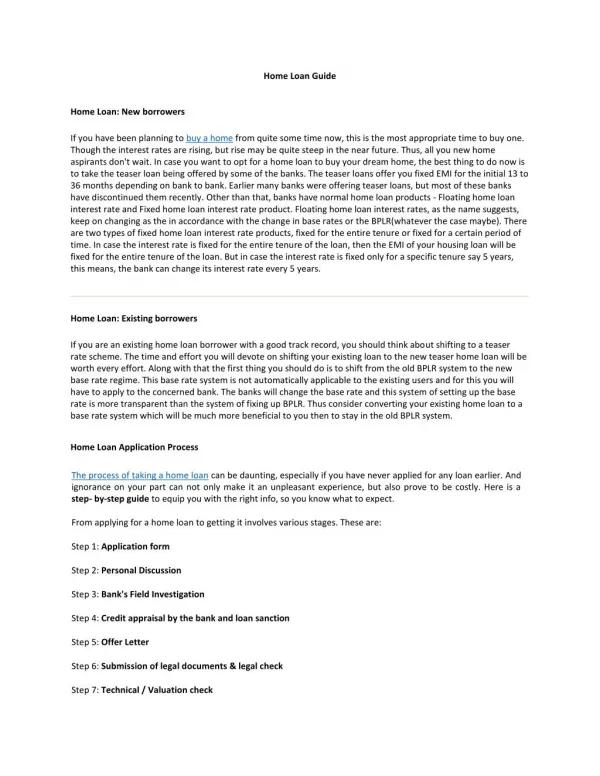

Download

1 / 18

180 likes | 191 Views

Finance the payment on buying a new flat through home loan. http://ladderkerala.com/

E N D

A GUIDE TO HOME LOAN PROCESS flats and apartments in calicut

Amendments These are mostly on the interest of the institution that lends the loan and the right to alter the terms of agreement in the event of difficulty in repayment, lies with them. The borrower should ensure that their written consent is mandatory for any changes in the terms of agreement.

2. Fluctuating Interest Rates This clause enables the bank to change the payable interest rates as per the fluctuations in the applicable base rates. This also allows them to increase the rate in the future according to the increase in the market rate. Therefore, the borrower must ensure that the interest rates negotiated by him are clearly stated in the agreement.

3. Security Cover The lender can ask the borrower to provide additional security as a protection for the outstanding home loan amount.

4. Balance Amount A clause mentioning that the payments made by the borrower should be first adjusted against any outstanding dues as on the date.

5. Notification Clause The lender is entitled to information about any change to the employment, profession, income, business or residential address of the borrower

6. Describing Default The condition upon which the borrower is considered to have defaulted should be stated in the agreement. The implications he is bound to face should also be clearly described.

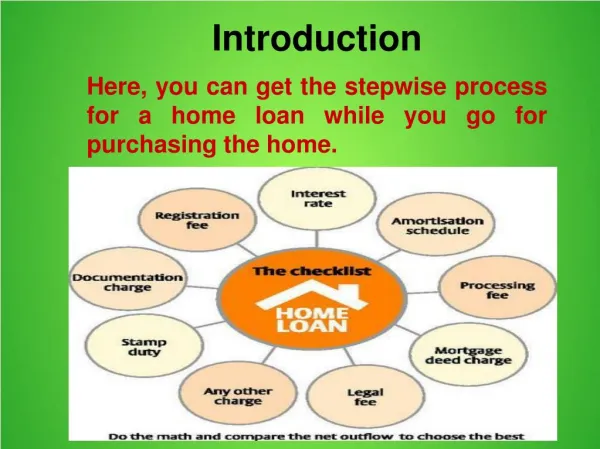

1. Eligibility Repaying capacity is a determining factor in deciding total eligibility for a home loan. The monthly disposable income which is based on monthly expenses, partner’s income, assets, other liabilities, etc. is evaluated to judge the repaying capacity. Also, liabilities like another existing loan can bring down the eligibility

2. Amount Eligible For The applicant is mostly expected to pay about 10 -20% of the purchase price of the house or apartment as down payment. The remaining costs including registration, transfer and stamp duty charges are financed by the bank or financial institution.

3. Loan Type There 2 common types of home loans based on interest rate include fixed rate loan and floating rate loan. In a fixed rate, the interest rate doesn’t change with market fluctuations, but a floating interest loan varies according to the present market conditions. For long-term loans like home loans, floating interest rated are considered ideal as interest rates are expected to come down after a period of time.

4. Co-applicant A co-applicant is considered highly beneficial while applying for a home loan as it enables the financial burden to be shared thus ensuring smooth repayment without having to affect the monthly budget if the family. A co-applicant can be an immediate family member who is a salaried individual.

5. Documents Making a check-list of the required documents for loan application will help organise everything at the time of submission. Proof of identity and address, recent salary slips, bank statements from the last 6 months along with documents of collateral security are asked to submit by most banks.

1. Age and Income The income determines the borrower’s ability for home loans. Also, the age of the borrower is also a contributing factor to overall loan amount eligibility. For salaried applicants, 60 years is considered as the retirement age and the maximum loan tenure is calculated based on the remaining years of service.

2. Age of Property As the property is pledged as security for obtaining the home loan, the age of the property is also a determining factor. The tenure of the loan is calculated based on the residual life of the property and it cannot be longer than the age of the building. If the tenure is lesser than the property age, there is a risk of the lender losing his security if the property is destroyed.

3. Leasehold Properties If the property is constructed on a leasehold land, the loan tenure cannot be more than the lease period. Even though if the property is in good condition, the lender will not risk losing the security when the lease is renewed.