Download

1 / 5

50 likes | 56 Views

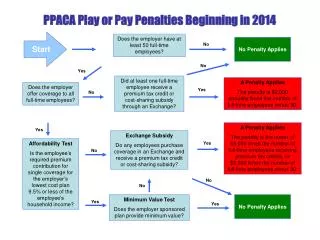

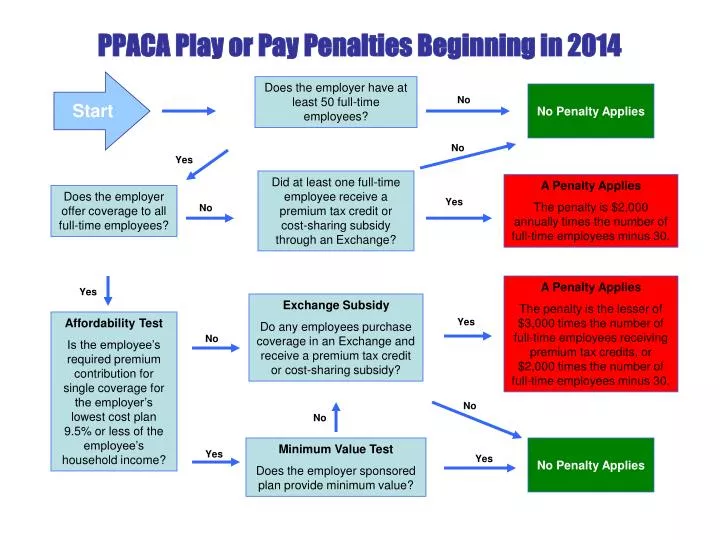

Learn about the Play or Pay penalties under the PPACA and how they apply to employers based on their number of full-time employees, coverage offerings, and employee subsidies. Get clarity on the requirements to avoid penalties.

E N D

Start Does the employer have at least 50 full-time employees? No Penalty Applies No No Yes PPACA Play or Pay Penalties Beginning in 2014 Did at least one full-time employee receive a premium tax credit or cost-sharing subsidy through an Exchange? A Penalty Applies The penalty is $2,000 annually times the number of full-time employees minus 30. Does the employer offer coverage to all full-time employees? Yes No A Penalty Applies The penalty is the lesser of $3,000 times the number of full-time employees receiving premium tax credits, or $2,000 times the number of full-time employees minus 30. Yes Exchange Subsidy Do any employees purchase coverage in an Exchange and receive a premium tax credit or cost-sharing subsidy? Affordability Test Is the employee’s required premium contribution for single coverage for the employer’s lowest cost plan 9.5% or less of the employee’s household income? Yes No No No Minimum Value Test Does the employer sponsored plan provide minimum value? No Penalty Applies Yes Yes

PPACA Play or Pay Penalties Beginning in 2014 Affordability Test Is the employee’s required premium contribution for single coverage for the employer’s lowest cost plan 9.5% or less of the employee’s household income?

PPACA Play or Pay Penalties Beginning in 2014 Did at least one full-time employee receive a premium tax credit or cost-sharing subsidy through an Exchange? No Does the employer offer coverage to all full-time employees? Yes Yes Exchange Subsidy Do any employees purchase coverage in an Exchange and receive a premium tax credit or cost-sharing subsidy? Affordability Test Is the employee’s required premium contribution for single coverage for the employer’s lowest cost plan 9.5% or less of the employee’s household income? No Yes No Minimum Value Test Does the employer sponsored plan provide minimum value? Yes

Rick Franklin, CLU, RHU, REBC Chief Executive Officer 5005 N Lincoln Oklahoma City, OK 73105 P.O. Box 296001 Oklahoma City, OK 73126 Office: (405) 290-5744 800-850-7155 ext. 5744 E-mail: rfranklin@clfrates.com