Download

1 / 9

140 likes | 229 Views

Redemption of preference shares. Introduction— redemption of preference shares means return of share money to the shareholder & it’s possible only through issue of preference shares. Conditions for issue of preference shares- Authorised by articles Redemption of fully paid shares Contd.

E N D

Redemption of preference shares • Introduction—redemption of preference shares means return of share money to the shareholder & it’s possible only through issue of preference shares. • Conditions for issue of preference shares- • Authorised by articles • Redemption of fully paid shares • Contd.

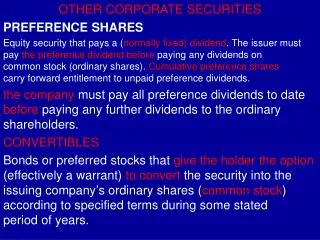

Conditions contd. • Redemption out of profit or by issuing new shares- • Preference shares can be redeemed either out of profits available for dividend or out of proceeds of fresh issue of shares • Out of profit- an amt.equivalent to the face value of shares is tranferred to ‘capital redemption reserve a/c’.the advantage of such transfer is that the pref. sh.cap.redeemed would be replaced by cap.red. Reserve. • Profits available for dividend means those profits which can be paid as dividend by the co.--

Redemption by issuing new shares • New issue of equity or preference shares may used for the purpose of redemption. If the co. issues debentures or loan taken from bank,for this purpose, it will not be used for redemption of pref. shares. • Redemption partly out of profit and partly by issuing new shares—

Conditions contd. • Utilisation of capital redemption reserve a/c—for fully paid shares only • Redemption within one month from issue of new shares • Redemption at premium-either out of securities premium a/c or out of profits • Registrar to be informed within 30 days

Bonus shares • If the co. has accumulated more reserves than normally necessary, it may distribute this excess reserve in the form of bonus shares.bonus shares means the shares without cost for which nothing is paid by the shareholders. • -by making partly paid shares as fully paid • -by issue of free fully paid new shares

Guidelines of SEBI • The co. shall forward a certificate signed by it’s c.a. or c.s. to the effect that the rules regarding this have been complied with. • No bonus issue will be made which will dilute the value or rights of holders of debentures, convertible fully or partly. • Bonus issue is made out of free reserves built out of genuine profits or securities premium collected in cash only. • Reserves created by revaluation of fixed assets are not capitalised. • Declaration of bonus issue is not made in lieu of dividend.

Contd. • The proposal must be implemented within 6 months from the date of approval by board of directors. • The co. has not defaulted in the payment of statutory dues ,interest in respect of fixed deposits,& interest on debentures. • If provision is not there in articles regarding capitalisation of reserves, the co. shall pass a resolution in its general body meeting. • If authorised or subscribed cap. Increases due to this ,a resolution shall be passed in general body meeting to increase the capital. • ------------------------------///////////------------------