Download

1 / 6

60 likes | 217 Views

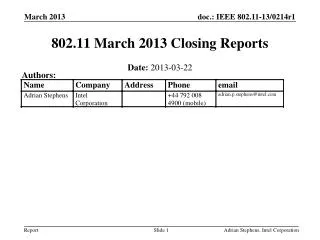

TRIA Timeline For Expiration – Closing In. Currently, mixed political backing for extending TRIA beyond 12/31/2014

E N D

TRIA Timeline For Expiration – Closing In • Currently, mixed political backing for extending TRIA beyond 12/31/2014 • Absent an extension of TRIA, policyholders have begun to see “Conditional Endorsements” or “Sunset Endorsements” or “Terrorism Exclusions” from many of the property markets (varies by client and capacity) • Impacts embedded TRIA coverage, Standalone Terrorism pricing and TRIA Captive placements • Options: • Reliance on Standalone Terrorism Markets for multi-year term, long-term policies • TRIA Captive “Flip” Product introduced by Aon in 2004 • Contingent Capital Standalone Product • Embed as much terrorism coverage with markets willing to offer the cover beyond 2014 • Reduce terrorism limits (or decline coverage)

Potential Changes to TRIA – Impact on Industry TBD • Current TRIPRA 2007 Retentions likely to change if TRIA is extended • Scope of suggested changes vary • TRIA Deductible – increase from current 20.0% to 25.0% or 30.0% and vary by line of business • Program Trigger –increase from $100 mm to $10 Billion or higher • Coinsurance - increases on varied level based upon line of business • Scope – possibly amend to only cover certain lines – e.g., Worker’s Compensation • Duration – permanent ? 5 – 7 years? • Recoupment – increase or possible pre-event surcharge • Timeframe for certification • Clarification on cyber

Does the Property Market Have the Capacity to Respond Absent TRIA? • TRIA Property capacity for Embedded product tied to available Per Risk Property capacity – theoretical Per Risk capacity of USD10 to 14 Bn on a pure AOP basis – drops considerably for CAT placements • Standalone Terrorism at average theoretical Per Risk capacity of USD2.2 Bn, but higher and lower limits based upon aggregate exposures • Bottom line is that Standalone Per Risk can’t match capacity for Embedded TRIA 85% Drop in Per Risk Property Terrorism Capacity

Pro’s: “per occurrence” for embedded terrorism lines, full following form coverage, no reliance on a captive – for non target risks can be most cost effective Con’s: restricts available “all risk” property capacity, no pricing consistency by layer, no NBCR/CNBR coverage Pro’s: coverage certainty, no Captive fronting or retained exposure Con’s: expensive, limited loss limit availability, no NBCR/CNBR coverage, aggregated coverage Property markets still have “fire following concerns” if not reinsuring a captive Pro’s: increased limits, premium cost savings, NBCR coverage for 85% of limits, can “wrap” captive for non US exposures and hedge up to Non Certified loss limit for Wrap Con’s: TRIA is an untested product, US Treasury “gaming concerns”, requires increased capitalization for retentions that are not reinsured Reliant on TRIA being extended (but can hedge via standalone “wrap” limits) Terrorism Risk Transfer Options for Insureds • 1 Embedded TRIA and Non Certified Terrorism coverage • 2 Open market standalone terrorism coverage • 3 Captive fronted program with direct access to TRIA and standalone reinsurance Can combine all three options

What can risk managers do to manage the uncertainty of TRIA extension? • Communicate potential changes to your management and stakeholders • Start your renewal discussions early • Write and/or call your congressional representatives • Communicate with your Government Affairs staff • Be active with the RIMS External Affairs Committee • Attend the RIMS Legislative Summit on June 9-10 • Communicate with your trade associations