Download

1 / 29

300 likes | 579 Views

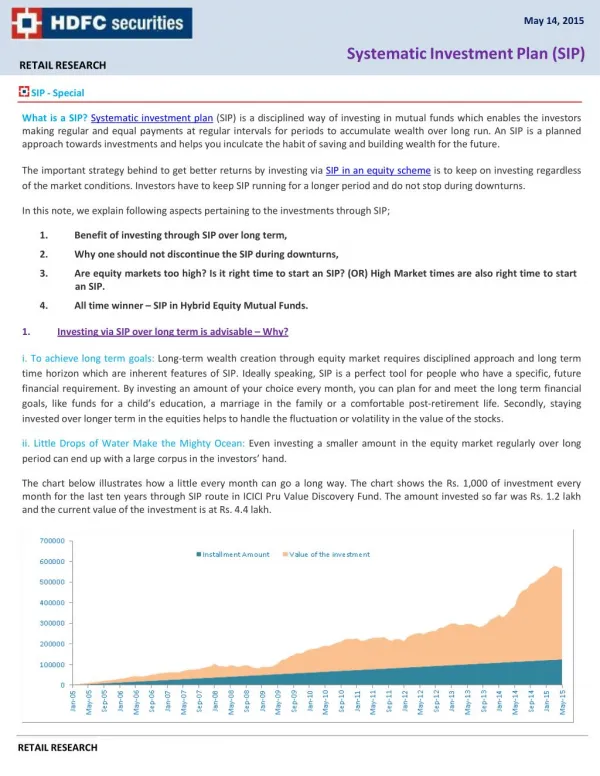

Systematic Investment Plan (SIP) is a smart financial planning tool that helps you to create wealth, by investing small sums of money every month, over a period of time. Investing at an early stage of life lets you enjoy the benefits of two powerful strategies, rupee cost averaging and the power of compounding.

E N D

Systematic Investment Plan (SIPs)(The Smart Investors’ Preference) www.ekarup.com

SIP(Systematic Investment Plan) The Formula for Creating Wealth www.ekarup.com

SIP(Systematic Investment Plan) • Systematic Investment Plan (SIP) is a financial planning tool that helps you • to create wealth, by investing small sums of money every month, over a period of time. • A Systematic Investment Plan (SIP) is a vehicle offered by mutual funds to • help investors invest regularly in a disciplined manner. • SIP works on the principle of legitimate investments. • It is like your recurring deposit where you put in a small amount every month. • It allows you to invest in a MF by making smaller periodic investments • (monthly or quarterly) in place of a heavy one-time investment. • Systematic Investing in a Mutual Fund is to preventing the pitfalls of equity • investment and still enjoying the high returns. www.ekarup.com

Starting Early • It is best advised to start as early and follow these steps: • Categorize the child’s needs and then start saving up to meet each of these goals • While calculating likely cost of education, factor in rate of inflation • Start with a smaller sum • Gain from the power of compounding

Categorize, Prioritise and Invest As there are many child specific goals you would have set, it is important to categorise them and prioritise them. • You will be clear about your investment horizon whenever you invest. • You will have a better picture on the amount of risk you will take towards • completing a goal. • You will be able to choose financial instruments that will help fulfil these • individual goals. • You will be able to stay away from high-risk instruments.

SIP - a good choice • SIP help you participate in the growth of capital markets and at the same time helps you diversify your risk. Thus it is a great option for securing your child's future. • SIP gives you the flexibility to plan your investments depending on what the eventual need is that you are providing for. • In a scenario, • where the investment is for a goal that will require the funds in the next 2-3 years, • Like a wedding or if your kid is in high school and will pursue professionals( Doctors, Engineers..) next - it is best to opt for a debt fund, • Where your corpus is more or less protected and you are able to get some returns on your investment.

Human Life Cycle Phase I Phase II Phase III Child’s Marriage Child’s Education Housing Child birth Marriage 38 yrs 10- 20 yrs 22 yrs Earning Years Post Retirement Years Education Age- 22 yrs Age- 60 yrs www.ekarup.com

Here are some model portfolios Depending upon when you begin investing for your child, 1. Age of the child: Newborn to 5 years • Investment horizon : 13 to 18 years • If you start investing at this stage, • you allow your savings the maximum time to build up assets for your child's education. • With time on your side, you can take higher risk and go for equity funds. • However, if you choose to invest on a regular basis, try and increase the amount every year.

Cont… 2. Age of the child: 6-12 years • Investment horizon : 6 to 12 years While a part of the portfolio may still focus on aggressive investment options like equity funds, • you will do well to include balanced funds also to reduce risk. • The attempt should be to move money to lesser volatile investment options, as the child grows older.

Cont… 3. Age of the child: 13- 18 years • Investment horizon : 1 to 5 years • At this stage, it would be advisable to invest in funds that are least volatile and overall the focus should be on preserving capital. • Also, liquidity should be an important consideration while working out the strategy. • While the open-ended mutual funds will ensure that the money is available to you as and when you require it, the key is to make the money grow at a reasonable rate. www.ekarup.com

Rupee Cost Averaging • Most investors want to buy stocks when the prices are low and sell them when prices are high. • But timing the market is time consuming risky. • A more successful investment strategy is to adopt the method called Rupee Cost Averaging. • Systematic investing can help put the power of compounding on your side. www.ekarup.com

Market timing is irrelevant www.ekarup.com

Invest for Long Term Data Source : Bloomberg Hence longer your SIP Period • Lower the risk • Greater the effect of compounding • More predictable average returns www.ekarup.com

Case Study – Real Life Situation • Assume • You are 30 yrs of age ; have a wife and kid • Current Annual expenditure of Rs. 5,00,000 • Retirement expected at age 60 yrs • More • Average prices (i.e. inflation) will rise by 7% pa • After 30 yrs when you retire, the low risk rate of return will be 6% pa (Considering you put all your accumulated corpus post retirement in a bank deposit) • You will live for more 20 years post retirement • You have invest from Rs.500 • So let’s see what will be the corpus required at the time of your retirement to maintain the same current lifestyle additionally with enhanced medical expenses www.ekarup.com

Cont… Current Expenditure Rs.5,00,000 p.a. Inflated at 7% p.a. for 30 years Expenditure at the time of Retirement 36,00,000 p.a. Therefore to generate this income every year post retirement you need to accumulate a corpus Income to be generated post Retirement Rs. 36,00,000 p.a. But then there is a solution… Corpus Required at the time of Retirement Your first reaction Impossible! It cannot be achieved www.ekarup.com

Cont... So what’s the Solution… Just one simple thing For Example… Subscribe for an SIP of Rs.15,000 per month in a good diversified equity fund for 30 years and forget it You still don’t believe it that it can be that simple; let us validate our conviction with actual returns generated in a equity fund over the years *conditions apply From the table it is crystal clear that if an investor did an SIP of Rs.15000 per month in Equity Fund for 15years, he would have invested 27 Lakhs and that would have grown to a whopping number of 3.4 croreas on date; in spite of so many pitfalls in equity markets in last 15 years. www.ekarup.com

Tips to how to make safe investments • Besides, since building up assets for your child's education is a long term objective, • It is important to ensure that you invest in those options that have the potential to give you better real rate of return i.e. returns minus inflation. • This factor is crucial considering the escalating costs of higher education. • Mutual funds can provide an excellent investment vehicle for your child's education. • Besides, investing through a tax efficient vehicle like mutual funds can help you accumulate more for your child's education. www.ekarup.com

Cont… Remember, the way you save as well your investment strategy will depend on many factors like, • how much you wish to save, • how long until the money is needed, • And whether you have a lump sum or will be saving out of your current income. They offer.., • diversification • flexibility • simplicity.

Debt Oriented Child Plans • In addition to, • equity oriented child plans, • debt oriented child plans • are also available in the market. • These plans have a more conservative portfolio mix and are suitable for investors with moderate risk profiles and time horizons.

Cont… The chart below shows annualized returns for equity oriented child plans over a one, three and five year time periods (based on Feb 20 NAVs).

Cont… • ICICI Prudential Child Care Plan - Study Plan: • This scheme was launched in 2001 and has Rs 36 Crores of AUM. The portfolio mix is weighted to debt, with equities comprising only 24%, debt 73% and cash equivalents 3%. • The quality of the debt portfolio is good, comprising of G-Secs and highly rated corporate bonds • Tata Young Citizens Fund: • This is one of the oldest child plans, launched in 1995. It has nearly Rs 175 Crores of AUM. • This fund has a slightly higher allocation to equities compared to its peers. • Equity accounts for 49% of the portfolio mix, while fixed income securities (debt and money market) comprise about 44% of portfolio value. The balance is in cash equivalents

Cont… • HDFC Children's Gift Fund Savings Plan: • This scheme, launched in 2001, has Rs 73 Crores of AUM. • In terms of portfolio composition debt is 51%, equity 19% and cash equivalents in close to 30%. • The quality of the debt portfolio is good, comprising of G-Secs and highly rated corporate bonds. • SBI Magnum Children Benefit Plan: • Thus scheme was launched in 2002 and has AUM base on Rs 23 Crores. • In terms of portfolio mix, equity comprises 24%, while fixed income securities (debt and money market) 74% of the portfolio, with debt accounting for 48%. • The balance is in cash equivalents. The quality of the debt portfolio is good, comprising of G-Secs and highly rated corporate bonds

Goals Each instrument in the market fits a particular need and to select the best investment plan for your child, • You don't have a ready capital to invest directly right-away. The capital needs to be built in terms of savings over the years. • You have sufficient time – your child is just in pre-school and you have close to 15-18 years to build a good sum of money.

Cont… • And since we have time, we could also be a bit aggressive in our portfolio selection and bet a part of the yearly savings in equity instruments. • However, a fair share needs to be invested in asset classes too like gold for example. • We would also need to factor-in the ever increasing cost of education. Each year, the cost of education especially, higher education breaks new limits. • With the rising inflation, we need a vehicle which will factor in the inflation and give you returns over and above that.

Futures Child Mutual Fund plans are exactly built around these needs, Diversified Allocation: Your funds are invested across various asset and equity classes providing you the right mix of risk exposure. Low Cost: Mutual Funds charge less than 2.25% per annum as expenses which is way better than spending as high as 6% on ULIPs. Liquidity: Unlike ULIPs, one is not penalised for exiting a child mutual fund plan prematurely. In case one is in dire need of liquid money, one can always stop and exit which makes Mutual Fund SIPs highly liquid.

Cont… • Professional Portfolio Management: • With Mutual Funds, you get the assurance that your money is in the hands of professionals. • You can get them to take up the cumbersome and tricky task of timing the market and deciding the right mix for investing your money. • The best possible investment plan for your child's bright future is to invest in your child's education and taking all these factors into consideration, Mutual Funds are the best possible way which will help you give him that.

Benefits • Discipline : • The cardinal rule of building your corpus is to stay focused, invest regularly and maintain discipline in your investing pattern. • Power of compounding: • Investment gurus always recommend that one must start investing early in life. One of the main reasons for doing that is the benefit of compounding • Rupee cost averaging: • This is especially true for investments in equities. When you invest the same amount in a fund at regular intervals over time, you buy more units when the price is lower.

Cont… • Convenience: • This is a very convenient way of investing. You have to just submit cheques along with the filled up enrolment form. • Other advantages .., • There are no entry or exit loads on SIP investments. • Capital gains, wherever applicable, are taxed on a first-in, first-out basis. • Volatile market is good for SIP investor. • Flexibility in investment.

Ekarup Coimbatore (Corporate Office) Landline No :0422-4354700 P.H No: +91 9894447881 Mail : ekarupcbe@gmail.com Chennai Landline No :044-43204700 P.H No: +91 9894447882 Mail : ekarupchennai@gmail.com Madurai Landline No : 0452-4354700 P.H No: +91 9894447883 Mail: ekarupmadurai@gmail.com Pondicherry : Landline No : 0413-4304700 P.H No: +91 9894447884 Mail : ekaruppondy@gmail.com Formore information visit on www.ekarup.com