Download

1 / 17

230 likes | 522 Views

6.b Purchasing Power Parity. Price levels should be roughly the same in different countries with different currencies.

E N D

6.b Purchasing Power Parity Price levels should be roughly the same in different countries with different currencies.

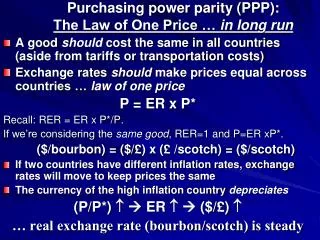

Purchasing Power Parity (PPP) suggests when going to a foreign country, a person should be able to exchange his currency for the foreign currency, and buy roughly the same number of goods he was able to buy at home. Letting P$ denote the price level of a basket of goods in the USA, and P£ the price level of the same basket of goods in the UK, PPP suggests For example, if the same basket of goods costs $2.00 in the USA and £1.50 in the UK, the spot rate should be S($/£) = 2.00/1.50 = 1.333. S($/£) = P$/P£

Absolute Purchasing Power Parity (PPP) Illustrated $2.00 £1.33 S($/£) = 1.33 * The spot rate that makes shopping cost the same.

Relative PPP Absolute PPP: S($/£) = P$/P£ Let π$ and π£ represent the inflation rates and Define e = %∆S($/£) as the rate of change in the relative price levels. Then for PPP to hold over time as the price levels change….. Relative PPP: e = (π$ - π£)/(1 + π£) ≈ π$ - π£

Relative Purchasing Power Parity Illustrated (RPPP also referred to as future PPP or FPPP) US prices up… Suppose USA experiences inflation, but UK prices unchanged. US $ down! π$ = 50% π£ = 0% $3.00 $2.00 £1.50 S($/£) = 2.00/1.50 = 1.33 • New S($/£) = 3.00/1.5 = 2.00. • %∆ S($/£) = 2.00/1.33 – 1 = 50% = π$ -π£

Real Exchange Rates We’re asking here if relative price changes (inflation) are being exactly offset by exchange rate changes. If not, then one country is getting “cheaper”; the other more “expensive. If relative PPP holds true, it should be that 1 + e = (1 + π$)/(1 + π£) or 1 should = (1 + π$/[(1 + π£)(1 + e)]. But this might not be true! Define the Real Exchange Rate q as q = (1 + π$/[(1 + π£)(1 + e)] If q = 1 then competiveness is maintained. If q < 1 then competitiveness is improving. If q > 1 then competiveness is deteriorating.

The Fisher Effect (FE) The FE holds that an increase (decrease) in the expected inflation rate will lead to a proportionate increase (decrease) in the nominal interest rate. Economist Fisher separated out observed “nominal” interest rates i$ into a “real” component ρ$ and an expected inflation component E(π$). 1 + i$ = (1 + ρ$)x(1 + E(π$)) i$ = ρ$ + E(π$) + (ρ$xE(π$)) ≈ ρ$ + E(π$) Or E(π$) = (i$ - ρ$)/(1 + ρ$) ≈ i$ - ρ$

The Fisher Effect (cont.) The IFE suggests that the (observable) nominal interest rate differential reflects the expected change in the exchange rate. Continuing, Fisher assumed that (a) this relationship holds true for all countries, and (b) that the real interest rates would be the same in all countries; i.e. ρ$ = ρ£ = ρ. Therefore… E(π$) = (i$ - ρ)/(1 + ρ) ≈ i$ - ρ E(π£) = (i£- ρ)/(1 + ρ) ≈ i£- ρ Recall relative PPP: e = (π$ - π£)/(1 + π£) ≈ π$ - π£ Combined with relative PPP we get the International Fisher Effect (IFE): IFE: E(e)= (i$ - i£)/(1 + i£) ≈ i$ - i£

Forward Expectations Parity (FEP) FEP states that the forward exchange rate premium/discount is equal to the expected change in the exchange rate. (Just as previously suggested!) When the IFE is combined with IRP IFE: E(e)= (i$ - i£)/(1 + i£) ≈ i$ - i£ IRP: e = We get Forward Expectations Parity: = E(e)

Forecasting Future FX Rates • EMH • The efficient markets hypothesis (EMH) states that today’s rate (or the forward rate) is the market’s best guess of future rates. • Fundamentals • Statistical analysis based upon relative economic fundamentals, such as money supply, GDP growth, current account, etc. • Technicals • Unscientific predictions based upon charts showing past exchange rate movements.

Forecasters’ Performance Not So Good (*Below, value < 1 implies forecaster beat the forward rate) It appears that FX forecasters are not worth the money!