Download

1 / 23

1.11k likes | 2.64k Views

A Non-Banking Financial Company (NBFC) incorporated under Companies Act, 2013 or Companies Act, 1956 (Old). The main business of NBFC is providing loans and advances, acquisition of shares, debentures and other stocks issued by Government or other local authorities, insurance business, leasing, hire-purchase, etc.<br><br>For quick service click: https://enterslice.com/nbfc-registration<br><br>GET FREE CONSULTANCY <br>Helpline: 91 9069142028 <br>Email: info@enterslice.com <br>Website: www.enterslice.com<br>

E N D

WHAT IS NON-BANKING FINANCIAL COMPANY( NBFC) ? Award Winning CA and Legal Technology Company Enterslice is Award Winning Legal Technology Company that helps entrepreneurs start and manage their business in India.

What is Non-Banking Financial Company (NBFC) • A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act, 1956 engaged in : • The business of loans and advances • acquisition of shares/stocks/bonds/debentures/securities issued by Government or local authority or other marketable securities of a like nature, leasing, hire-purchase, insurance business, chit business • But does not include any institution whose principal business is that of: • agriculture activity • industrial activity, purchase or sale of any goods (other than securities) or • providing any services and sale/purchase/construction of immovable property. • A non-banking institution which is a company and has principal business of receiving deposits under any scheme or arrangement in one lump sum or in installments by way of contributions or in any other manner, is also a non-banking financial company which is known as Residuary non-banking company.

WHAT ARE THE DIFFERENT TYPES AND CATEGORIES OF NBFC REGISTERED WITH RBI

NBFC 1. Asset Finance Company (AFC) 4. Infrastructure Finance Company 2. Investment Company (IC) 3. Loan Company (LC): 5. Systemically Important Core Investment Company 7. Micro Finance Institution 6. Infrastructure Debt Fund 8. NBFC-Factors 9. Mortgage Guarantee Companies 10. NBFC- Non-Operative Financial Holding Company

NBFC REGISTRATION • As per Section 45-IA of the RBI Act, 1934, no company can commence or carry on business of a non-banking financial institution: • without obtaining a certificate of registration and without having a Net Owned Funds of Rs. 200 lakhs. • Net owned funds is the balance of “owned funds” minus the amount of investment in shares of subsidiaries, companies in the same group and all other NBFCs, book value of debentures, bonds, outstanding loans and advances including hire purchase and lease finance made to and deposits with subsidiaries and companies in the same group. • Owned funds is the aggregate of paid-up equity capital , preference shares which are compulsorily convertible into equity, free reserves , balance in share premium account and capital reserves representing surplus arising out of sale proceeds of asset, excluding reserves created by revaluation of asset, after deducting therefrom accumulated balance of loss, deferred revenue expenditure and other intangible assets. • Application for becoming an NBFC must be made in the requisite form to Regional Office of the Reserve Bank of India.

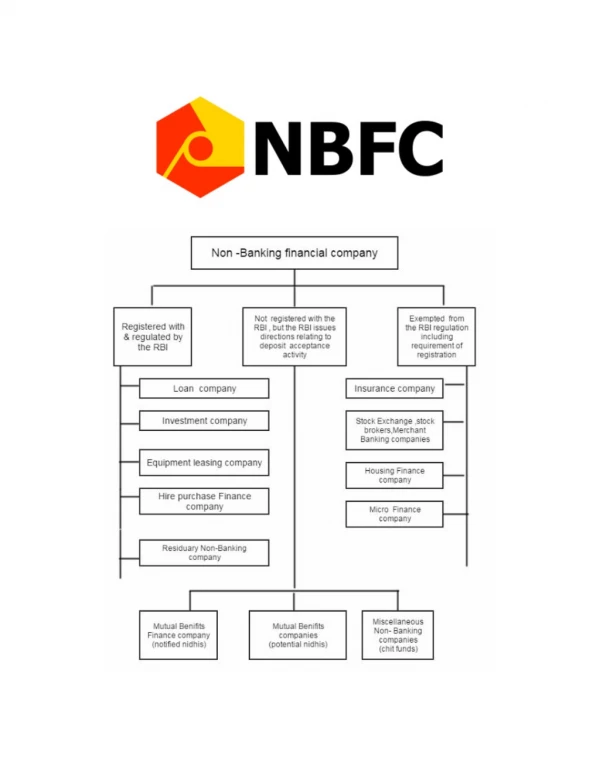

Loan Company. • Investment Company. • Equipment Leasing Company. • Hire purchase Finance Company. • Residuary Non- Banking company. Registered and Regulated by RBI • Mutual Benefit finance Company.(Notified Nidhis) • Mutual Benefit Company’s ( Potential Nidhis) • Miscellaneous Non- Banking Company. (Chit Funds) NBFC Not Registered and regulated by RBI but RBI issues directions relating to deposit acceptance activity. • Insurance Company. • Stock Exchange, stock brokers, merchant banking company. • Housing finance company. • Micro Finance Company. Exemptions from RBI regulations including requirement of registration.

BUSINESS WHICH CANNOT BE REGISTERED AS NBFC • Following businesses cannot be registered as NBFC: • Any institution whose principle business is of agriculture. • Or any business who is engaged in industrial activity. • Or any institution which is engaged in purchase or sale of any goods (other than securities). • Or which is providing any services. • Or which is engaged in sale/purchase/construction of immovable property. • Or any company whose principle business is receiving deposits under any scheme or arrangement in one lump-sum or in instalments by way of contributions or in any other manner.

REASON WHY FORMATION OF NBFC BECAME AN INTEGRAL PART OF THE SOCIETY • They complemented the Banking Sector in reaching out credit to the unbanked sector of the society i.e. micro, small, medium enterprises. • They have a sector specific expertise that allows them to have edge over there competitors. • Less time-consuming process of registration of NBFC. • Their ground-level understanding of their client’s credit needs. • Low cost of establishing the NBFC as compared to other financial institutions. • They provide support for economically weaker sections of the society. • They play a critical role in development of infrastructure, transport and employment generation.

CLASSIFICATION OF NBFCs BASED ON ACTIVITIES UNDERTAKEN : FY: 2017-18

CLASSIFICATION OF NBFCs BASED ON ACTIVITIES UNDERTAKEN : FY: 2017-18

FUTURE OF NBFC IN INDIA FUTURE OF NBFC IN INDIA

FUTURE OF NBFC IN INDIA With the ongoing stress on Public Sector Banks due to increase in bad debts, their ability to lend is deteriorating their demand and providing an opportunity to NBFC to increase their presence. The success of NBFC can be seen by their effective risk management capability, wider reach to the clients, control over the bad debts, better and understanding of the customer segment. The latent credit demand of emerging India will allow NBFC’s to fill the gap especially where traditional banks are unable to serve. Additionally to improve micro-economic conditions, high credit penetration, increase in consumption will allow NBFC’s to grow at a healthy rate. As per the report of the CAGR it has been estimated that NBFC’s will grow at the rate of 25%-33% over the next five years. Strong urban demand, high credit penetration, will drive the growth in consumer finance segment. Partnership with Payment Banks, Bill payment provider and other financial institutions such as insurance and asset management companies will help in their growth. With the reach of NBFC with the strong understanding of the market will them in proving themselves to be a better alternative as compared to traditional ways of banks. The number of start-ups in India has grown significantly from merely 2 in 2013 to 40 in 2017. These firm either operate as NBFC’s /intermediaries for banks and NBFC’s or P2P lending marketplace for connecting the individual borrowers and lenders directly. Rapid increase in the number of customers over the past few years, speed, simplicity, convenience and timely credit to borrowers which are regarded as ineligible as per the Bank criteria has increased the demand of NBFC. The growing importance of NBFC segment in Indian Financial system has led to a change the framework of NBFC on continuous basis. The regulations of NBFC has gone through a cyclical phase from simplified regulations to stringent regulations and finally now towards rationalisation.

DIFFERENCE BETWEEN NBFCs AND BANKS BANKS NBFC • NBFC’s cannot accept demand deposit. • NBFC’s cannot issue drawn cheque on itself. • Deposits done with NBFC’s are not insured. • Controls over NBFCs are relatively lesser stringent. • A Bank can accept demand deposit. • A Bank can issue drawn cheque on itself. • Deposits done in Banks are insured by Deposit Insurance and Credit Guarantee Corporation. • BR Acts and RBI Acts lay down stringent control over Banks.

WHAT IS NBFC TAKEOVER? What is Takeover? • The term takeover can be defined as to purchase of one company by the other company. The takeover can take place only when the two of the companies are already registered. In this process two companies are involved i.e.: • Target company. • Acquirer Company. Acquirer Company: Acquirer Company is said to be that company which is acquiring the target company. Target Company: Target Company is the company which is being targeted to be acquired by the other company which is already existing.

TAKEOVER CAN BE DONE IN 2 WAYS Hostile Takeover : Hostile takeover is totally different from friendly takeover. In this process the acquirer company secretly tries to acquire the acquirer company. Generally this kind of takeover takes place only when the management of the acquirer company is not willing to accept the offer of takeover. Friendly takeover : friendly takeover as the name insists is the takeover which takes place between the companies with their mutual consent. Acquirer Company gives offer to the target company for being acquired and the same offer is being accepted by the target company and the process of takeover take place. What is NBFC Takeover? Likewise, takeover of any other company takeover of NBFC can also take place. All the rules and regulations regarding the takeover of NBFC is governed & regulated by Reserve Bank of India. In simple words takeover can be said to be takeover of NBFC when any other NBFC acquires the other NBFC. Similarly it can also be done in two different ways i.e. friendly takeover and hostile takeover. • CONS: • The amount paid for goodwill is often less as compared to its actual price. • Conflict in new management. • Cultural clashes in two companies. • Reduce of employees’ morale. • Hidden liabilities of Target Company. • PROS: • Increase in profitability of Target Company. • Decrease in competition. • Increase in sales/revenue. • Expansion in distribution network. • Economies of scale. Pros and Cons of Takeover:

RBI REGULATIONS REGARDING TAKEOVER OF NBFC: • The RBI has specified some norms when takeover takes place which are required to be followed by NBFC’s and they are: • Takeover or acquisition of any NBFC requires the prior approval of RBI whether there is change in management or not. • The approval taken from RBI should be a written approval. • If on acquisition there is a transfer on shareholding for more than 10% of NBFC then prior approval of RBI will be required. • If there is change in shareholding for more than 26% for the reason of buyback/reduction in share capital then no approval of RBI is required, but this reduction/buyback should have been approved by the competent authority. • If there is change in the directors of the company i.e. more than 30% change is taking place in directors then the prior written approval shall be required. • Any change in director of the company requires a prior public notice is at least 30 days prior to the announcement of such change.

GOLD LOAN BY NBFC As the NBFC is being regulated by the Reserve Bank of India. The Reserve Bank of India has now provided a stringent guideline for NBFC for governing the loan provided by these NBFC against the Gold Jewellery. These guidelines will be helpful in bringing transparency between the Lenders and borrowers. Views of Industry Experts: Industry Experts are of the view that it will be more beneficial if the borrowers borrow the money from Banks rather than borrowing from Non-Banking Financial Intuitions. As gold loan companies. As the Banks provide gold loan at the rate of 12-16% but the interest rate provided by NBFC’s are 20-26% which is much higher than the rate provided by the Banks. As on 17th March, 2017 RBI in consultation with the Income Tax Department has clarified that No NBFC shall be allowed to give more than ₹ 20,000/- as a loan against the gold. Earlier this limit was of ₹1, 00,000 but now this limit has been reduced to ₹ 20,000. The main aim behind reducing this threshold limit is to make the economy cashless and more focus should be paid on digital payment.

RBI GUIDELINES: • NBFC before opening branch for more than 1000 should take prior approval of Central Bank. • And if any existing NBFC which is already in existence and having more than 1000 branches shall take prior approval of RBI before opening any further branches. • NBFC’s should have a proper security system for the pledged gold’s of the customers, if no proper security systems have been made no further branches can be opened. • In case if the pledged gold is more than 20 grams by a single owner at once or on cumulative basis then the NBFC is required to keep records of owner verification. • NBFC’s cannot give misleading advertisements. • RBI stated that NBFC cannot allow loan for more than 60% of the gold value pledged with the NBFC.

FOREIGN DIRECT INVESTMENT IN NBFC EVOLUTION OF FDI In 1997, guidelines were introduced for permitting foreign investment in the nonbanking financial services sector under FIPB approval route including norms subject to compliance with minimum capitalization requirement ranging from USD 5 million to USD 60 million based on percentage of foreign investment. However, the same was introduced only as a new sector classification without specific list of business activities covered therein. Subsequently, the Government prescribed the list of 14 activities that would be covered under the said ‘non-banking financial services’ sector. In the year 2000, a paradigm shift occurred in the FDI policy regime, wherein, except for a negative list, all the remaining activities were placed under the automatic route and caps were also gradually raised in a number of sectors / activities.

Extant FDI Regulatory Framework For NBFCs • Fund based activities • Merchant Banking • Underwriting • Portfolio Management Services. • Stock Broking. • Asset Management. • Venture Capital. • Custodian Services. • Factoring. • Leasing & Finance. • Housing Finance. • Credit Card Business. • Micro Credit . • Rural Credit • Non-fund based activities • Investment Advisory Services. • Financial Consultancy. • Forex Broking . • Credit Rating Agencies. • Money Changing Business

COMPLIANCES BY NBFC Regulations Transparency Policies Rules COMPLIANCES Law Requirements Standards

Annual Compliances 1. Unaudited March Monthly Return - On or before 30th June. 2. Audited March Monthly Return - Upon completion. 3. Statutory Auditor Certificate on Income & Assets - On or before 30th June. 4.Information about Company having FDI/Foreign Funds - On or before 30th June. 5.Resolution for non-acceptance of Deposit Fund - Before commencement of new financial year. 6.File Annual Audited Balance Sheet and P&L Account - One month from the date of sign off. 7. Declaration from the Auditors to act as Auditor of the Company - Annual basis.

Monthly Compliances Monthly Return - By 7th of every month. Periodical Compliances Appointment of the Director - Within 30 days of appointment of the Director. 2. Resignation of the Director - Within 30 days of resignation of the Director. 3. Adoption of any notification in the ensuing Board Meeting & filing the certified copy with RBI.