Download

1 / 14

140 likes | 149 Views

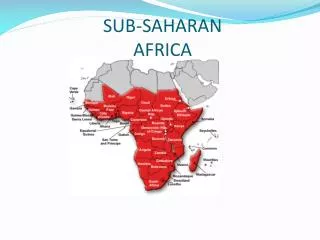

This report examines the main trends and scenarios for Sub-Saharan Africa's reliance on oil as a source of government revenue and its growing oil trade with China. It discusses the potential impacts on government revenues, economic growth, and the likelihood of domestic unrest. The report also explores flashpoints, such as domestic unrest and fuel subsidy reduction, that could further affect oil production and regional stability.

E N D

Main Trends I • Commission on Energy and Geopolitics, Oil Security 2025, Sub-Saharan Africa Scenarios • Key Fundamental Trends • Trend 1 • Reliance on oil as a source of government revenue will persist through 2025 and extend beyond established oil producers like Angola and Nigeria to additional Sub-Saharan African countries • All countries will remain highly exposed to negative impacts of oil price volatility.

Main Trends II • Trend 2 • Sub-Saharan Africa’s Growing oil trade with China will • Deepen bilateral economic ties, and • Could have long-term geopolitical implications, particularly if there is a receding U.S. presence in the region • Sub-Saharan Africa’s oil trade has already begun shifting away from demand centers in the West and toward emerging markets in Asia, particularly China

Scenario Impacts Scenario Impacts • Core concern for oil-exporting countries in sub-Saharan Africa is their ability to generate revenues necessary to • Meet budgetary needs and • Facilitate economic growth • Region is also considered a relatively high risk security environment for the IOCs to operate there • Disruptions to oil production are commonplace • U.S. boom is forcing established countries to seek new markets • Across sub-Saharan Africa the four scenarios could have very significant impacts on • government revenues, • economic growth, and employment and • consequently the likelihood of domestic unrest

Scenario A Scenario A Reference – Baseline Demand/Constrained Supply • Prices remain close to breakeven levels • Stressing government budgets and • Economic growth is constrained • Moderate levels of investment in new oil production capacity • Oil export volumes are increasingly oriented toward Asia • Transition is challenging as new relationships must be built

Scenario B • Scenario B Flush – abundant supply/baseline demand • Prices fall below fiscal breakeven levels • Public spending needs are likely not met • Economic growth is significantly impaired • Low levels of investment in new oil production capacity as projects are either cancelled or deferred • Finding new markets even more difficult than reference scenario due to strong growth in Middle East supplies although eastward shift for exports still expected • With reduced government revenues, Nigeria’s ability to participate in peace and stability operations on the continent could be diminished • -- or at lease become a lower priority in comparison to addressing domestic concerns

Scenario C • Scenario C Grind High Demand/Constrained supply • High prices generate government revenues and promote strong economic growth • Perhaps paradoxically, possible increased potential • for unrest as movements seek a greater share of resource wealth • And or remain frustrated by ongoing corruption • Highest level of investment in new oil production capacity – although disagreements over contract terms will likely persist • Countries face little difficulty finding new markets • Primarily Asian but also domestic and other Sub-Saharan Africa ones for displaced U.S. bound exports • Government fuel subsidies become costly • However economic growth and increased revenue from oil exports could aid their gradual removal

Scenario D • Scenario D Hyper growth – abundant supply/high demand • Although prices once again remain closer to fiscal breakeven levels • Higher sales help generate higher revenues and promote moderate economic growth • Moderate levels of investment in new oil production capacity • As in Grind Scenario high prices and high growth mean less difficulty finding new buyer markets than in either the Reference or Flush Scenarios

Flashpoint I • Flashpoint I • Domestic unrest prompted by • economic challenges and or • grievances about corruption, oil revenue-sharing or • environmental degradation • Develops into greater political instability further reducing oil production and potentially leading to regime change

Flashpoint II • Flashpoint II • Governments in Sub-Sahara attempt to remove fuel consumption subsidies to help them reduce fuel vulnerabilities • When successful fuel subsidy reduction has been accomplished it has been gradual with a commensurate increase in government support to the poorest

Flashpoint III • Flashpoint III • China’s increased regional influence could result in the reorientation of oil exports eastward in the event of supply disruption to meet Chinese demands, potentially creating shortages in other markets.