Download

1 / 12

120 likes | 124 Views

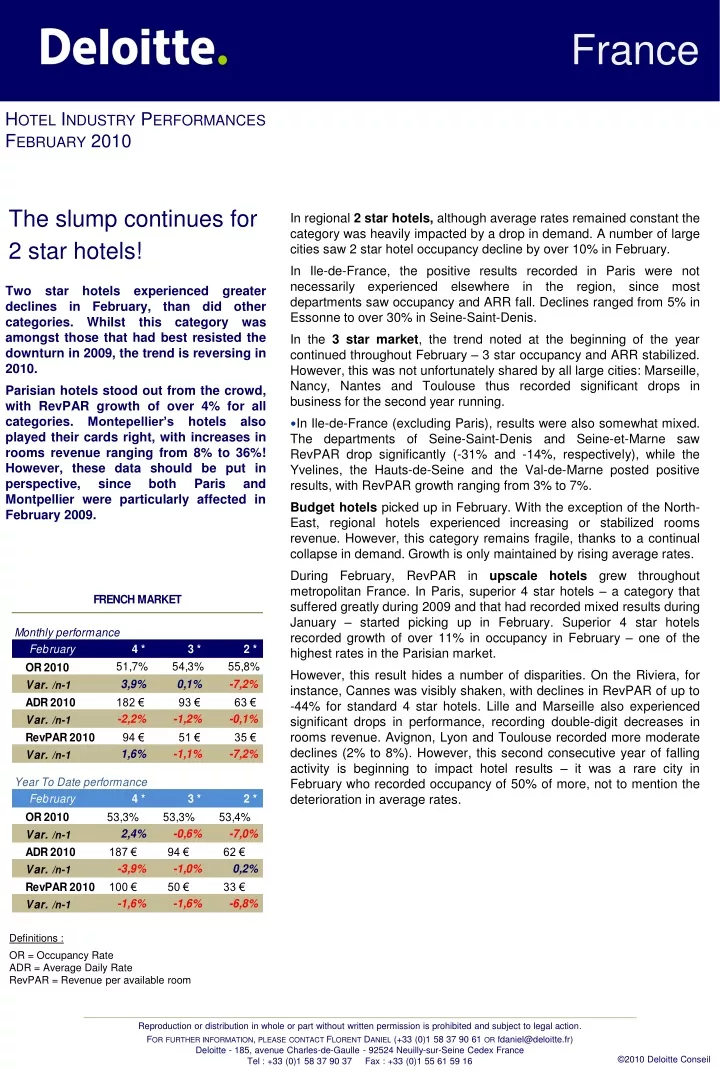

In February, 2-star hotels in France saw a significant drop in demand, leading to a decline in occupancy rates. This trend also affected the 3-star market in certain cities. However, budget hotels experienced growth and upscale hotels in metropolitan France saw an increase in revenue. Parisian and Montpellier hotels stood out with positive growth in RevPAR. This report provides an overview of the hotel industry performances in February 2010.

E N D

France In regional 2 star hotels, although average rates remained constant the category was heavily impacted by a drop in demand. A number of large cities saw 2 star hotel occupancy decline by over 10% in February. In Ile-de-France, the positive results recorded in Paris were not necessarily experienced elsewhere in the region, since most departments saw occupancy and ARR fall. Declines ranged from 5% in Essonne to over 30% in Seine-Saint-Denis. In the 3 star market, the trend noted at the beginning of the year continued throughout February – 3 star occupancy and ARR stabilized. However, this was not unfortunately shared by all large cities: Marseille, Nancy, Nantes and Toulouse thus recorded significant drops in business for the second year running. • In Ile-de-France (excluding Paris), results were also somewhat mixed. The departments of Seine-Saint-Denis and Seine-et-Marne saw RevPAR drop significantly (-31% and -14%, respectively), while the Yvelines, the Hauts-de-Seine and the Val-de-Marne posted positive results, with RevPAR growth ranging from 3% to 7%. Budget hotels picked up in February. With the exception of the North-East, regional hotels experienced increasing or stabilized rooms revenue. However, this category remains fragile, thanks to a continual collapse in demand. Growth is only maintained by rising average rates. During February, RevPARin upscale hotels grew throughout metropolitan France. In Paris, superior 4 star hotels – a category that suffered greatly during 2009 and that had recorded mixed results during January – started picking up in February. Superior 4 star hotels recorded growth of over 11% in occupancy in February – one of the highest rates in the Parisian market. However, this result hides a number of disparities. On the Riviera, for instance, Cannes was visibly shaken, with declines in RevPAR of up to -44% for standard 4 star hotels. Lille and Marseille also experienced significant drops in performance, recording double-digit decreases in rooms revenue. Avignon, Lyon and Toulouse recorded more moderate declines (2% to 8%). However, this second consecutive year of falling activity is beginning to impact hotel results – it was a rare city in February who recorded occupancy of 50% of more, not to mention the deterioration in average rates. Hotel Industry Performances February 2010 The slump continues for 2 star hotels! Two star hotelsexperiencedgreaterdeclines in February, thandidothercategories. Whilstthiscategorywasamongstthosethathad best resisted the downturn in 2009, the trend isreversing in 2010. Parisianhotelsstood out from the crowd, withRevPARgrowth of over 4% for all categories. Montepellier’shotelsalsoplayedtheircards right, withincreases in rooms revenue rangingfrom 8% to 36%! However, these data shouldbe put in perspective, sinceboth Paris and Montpellier wereparticularlyaffected in February 2009. Definitions : OR = Occupancy Rate ADR = Average Daily Rate RevPAR = Revenue per available room

France Performances – Paris February 2010 Paris-City Paris suburbs (excluding Paris) * Excluding La Défense and Roissy

France Performances – Regions February 2010 Regions Regions (Excl. French Riviera) FRENCH RIVIERA

France Performances – suburbs February 2010 Paris suburbs (excluding Paris) 3 STAR MARKET 2 STAR MARKET 0/1 STAR MARKET Departments in Paris suburbs : 77 : Seine et Marne; 78 : Yvelines; 91 : Essonne; 92 : Hauts-de-Seine; 93 : Seine St-Denis; 94 : Val de Marne; 95 : Val d’Oise

France Performances – North-East February 2010 North-East & Cities Departments in the North-Eastern set : Aisne; Allier; Ardennes; Aube; Cher; Côte-d'Or; Doubs; Jura; Loiret; Marne; Haute-Marne; Meurthe-et-Moselle; Meuse; Moselle; Nièvre; Nord; Oise; Pas-de-Calais; Bas-Rhin; Haut-Rhin; Haute-Saône; Saône-et-Loire; Vosges; Yonne; Territoire-de-Belfort

France Performances – North-West February 2010 North-West & Cities Departments in the North-Western set : Calvados; Côtes; Eure; Eure-et-Loir; Finistère; Ille-et-Vilaine; Indre; Indre-et-Loire; Loir-et-Cher; Loire-Atlantique; Maine-et-Loire; Manche; Mayenne; Morbihan; Orne; Sarthe; Seine-Maritime; Deux-Sèvres; Somme; Vendée; Vienne

France Performances – South-East (Excl. French riviera) February 2010 South-East (excl. French Riviera) & Cities Departments in the South-Eastern set :: Ain; Alpes; Hautes-Alpes; Alpes-Maritimes; Ardèche; Aude; Aveyron; Bouches-du-Rhône; Cantal; Drôme; Gard; Hérault; Isère; Loire; Haute-Loire; Lozère; Puy-de-Dôme; Pyrénées-Orientales; Rhône; Savoie; Savoie; Haute-Savoie; Var; Vaucluse

France Performances – French Riviera February 2010 French Riviera French Riviera Cities Cannes Nice Monaco* * Monaco set includes include the following cities: Monaco, Roquebrune and Cap d’Ail

France Performances – South-West February 2010 South-West & Cities Departments in the South-Western set : Ariège; Charente; Charente-Maritime; Corrèze; Creuse; Dordogne; Haute-Garonne; Gers; Gironde; Landes; Lot; Lot-et-Garonne; Pyrénées-Atlantiques; Hautes-Pyrénées; Tarn; Tarn-et-Garonne; Haute-Vienne

France Performances – Main cities in regions February 2010 Main cities in Regions – 4* and 3*

France Performances – Main cities in regions February 2010 Main cities in Regions – 2* and 0/1*

France Informations Definitions • Occupancy Rate (OR): Rooms sold divided by rooms available multiplied by 100. • RoomsAvailable : The number of rooms times the number of days in the period. • Average Daily Rate (ADR) : Room revenue divided by rooms sold. • Revenue per Available Room (RevPAR) : Room revenue divided by rooms available. • ADR and RevPAR are expressed in Euros, excluding VAT Deloitte About Deloitte in France Deloitte & Associés is the Deloitte Touche Tohmatsu member firm in France and the professional services are delivered by Deloitte & Associés, its subsidiaries and affiliates. Deloitte calls on diversified expertise to cover the scope of services required by its clients of all sizes from all sectors - major multinationals, local micro-companies and medium-sized enterprises. Our 6,000 professionals and partners embody the vigor and success of the Firm in their commitment to clients and their constant concern for service excellence. Deloitte offers a very comprehensive range of services: audit, consulting and risk services, tax and legal, accounting and corporate finance, in accordance with its multidisciplinary strategy and ethical approach. For more information, visit www.deloitte.fr Tourism, Hospitality & Leisure Desk Deloitte is one of the leading advisors in Tourism, Hospitality and leisure industries worldwide. We provide many consulting services for different stakeholders of the tourism industry. MARKET AND FEASIBILITY STUDIES VALUATION OF HOTEL AND TOURIST ASSETS URBAN TOURISM DEVELOPMENT PLANS HUMAN CAPITAL OTHERS SERVICES • Detailed market study • Operational recommendations to respond to the requirements of potential clients • Determination of the product-service concept • Determination of client target the price positioning • Revenue estimations (accommodation, food and beverage, other…) • Operating forecasts over several years : establishment of expense items to determine the project’s profitability (GOP, cash-flows • A detailed market study • Product analysis (strengths, weaknesses, necessary renovations and refurbishments • Forecasts over several years • The application of the discounted cash-flow method, completed by market references (recent and comparable transactions) and the use of the others methods, specially adapted to each case (multiple of turnover or GOP, approaches linked to the real estate market, etc). • Dynamic review of existing supply • Analysis of the impact of development factors (economy, transportation, tourist markets, etc.) • Analysis of supply/demand situation • Assessment of development ambitions and objectives • Recommendations on strategy • Aligning Human Resources with the strategic goals of the company • Mastering operational risks in terms of HR and abiding by the regulations • Incorporating the human dimension in all your reorganization and transformation processes • Developing an attractive and incentive remuneration policy • Hotel benchmark survey • Identification of operators and investors • Optimize your information systems • Marketing audits • Quality control • Organizational audits and management support • Etc.