Download

1 / 14

140 likes | 292 Views

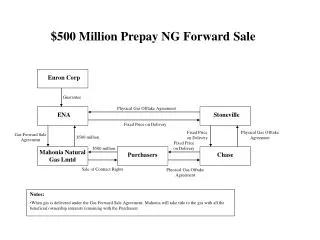

Mahonia Commodity Prepay Restructuring Proposal. 7/17/2000. Restructure Overview. Existing forward sale agreements are based on prices significantly lower than current market Posting margin against the forward sale and the financial swap will tie up significant capital

E N D

Restructure Overview • Existing forward sale agreements are based on prices significantly lower than current market • Posting margin against the forward sale and the financial swap will tie up significant capital • Chase wants to rebook physical forward under new physical master agreement • Restructure existing agreements by: • Amending forward sale agreement to revise the volumes due, and pay the market value of the volumes removed from the agreement • Terminate and cash settle existing financial and physical hedges with Chase • Execute new financial and physical hedges under existing and new master agreements • Obtain letters of consent from surety bond providers acknowledging the change in the structure of the forward sale agreements • Zero P&L effect Forward Sale Mahonia Prepay $ Volumes Fixed $ Enron Chase Index $ Financial Swap Index $ Volumes Chase Physical forward

P&L effects • Basic prepay structure hedges price movement of a physically delivered cash flow with a financial contract • Cash delivered under the financial contract occurs 5 days after the beginning of the month; the physical contract cash settles 55 days after the first of the month • When market prices are equal to the financial hedge strike price, the financial swap pays nothing and all cash flows are settled on day 55 • When market prices increase, Chase pays Enron the difference between the market price and the strike price on day 5 under the financial hedge • Enron doesn’t return that money until day 55, when the cash is delivered under the physical settlement • Therefore, Enron has been booking earnings on the 50 days of “float” while market prices have been rising over contract strike prices • The value of the financial contract is defined to be greater than the value of the physical contract assuming that the time value of money is positive • The difference between the cash value of the financial contract and the cash value of the physical contract is really a cash settlement of earnings that were made on a mark-to-market basis as the financial and physical contracts were revalued during the market price increase • If prices had decreased, this gain would have been a loss

Restructuring Proposals • 6 prepays are currently outstanding with Chase • Sep-95 $225MM - Natural Gas • This prepay will expire in Sep-00 and therefore is not proposed to be restructured • Dec-97 $300MM - Natural Gas • Jun-98 $250MM - Natural Gas • Dec-98 $250MM - Crude Oil • Jun-99 $500MM - Natural Gas • Jun-00 $650MM - Natural Gas • This prepay was recently executed and therefore is not proposed to be restructured • Basic prepay restructure strategy • Reduce volumes required to be delivered under the forward sale agreement • Increase fixed prices in the financial hedge so that periodic cashflows are nearly the same as under the previous arrangement • Given similar periodic fixed cash flows, the outstanding prepayment obligation will amortize similarly without requiring alteration to the fixed/floating interest rate hedges

December ‘97 $300MM • Balances as of July 31, 2000 • Existing forward sale volumes • Transco Sta. 65 45,000 MMBtu/d • TGT/SL 40,000 MMBtu/d • Columbia Gulf La. 30,000 MMBtu/d • Forward sale remaining volumes MTM value: $(218,596,625) • Existing financial hedge fixed prices • Transco Sta. 65 $2.2244/MMBtu • TGT/SL $2.1794/MMBtu • Columbia Gulf La. $2.1394/MMBtu • Financial hedge MTM value: $96,211,925 • Existing daily cash flow: $251,456.00 • Restructure existing forward sale agreement by: • Proposed volumes would be: • Transco Sta. 65: 26,000 MMBtu/d • TGT/SL: 17,000 MMBtu/d • Columbia Gulf La.: 22,000 MMBtu/d • Margin reference price would be: $3.898/MMBtu on 65,000 MMBtu/d • Applicable delivery dates would be: August, 2000 through December, 2001 • Value of the volumes removed from the FSA: $95,032,291

December ‘97 $300MM (con’t) • Restructure financial and physical hedges by: • Existing hedges would be terminated • New financial hedge proposed volumes and prices would be: • Transco Sta. 65: 26,000 MMBtu/d @ $3.8500/MMBtu • TGT/SL: 17,000 MMBtu/d @ $3.7755/MMBtu • Columbia Gulf La.: 22,000 MMBtu/d @ $3.9626/MMBtu • New physical hedge would be struck under new physical master with Chase • Applicable delivery dates: August, 2000 through December, 2001 • Value of the proposed financial hedge: $520,650 • Restructured daily cash flow: $251,456.30 • Transaction steps: • Enron restructures forward sale agreement with Mahonia, reducing volumes to be delivered according to the above proposal - in consideration, Enron would wire to Mahonia $95,032,291.00 • The financial and physical hedges between Enron and Chase would be terminated - in consideration, Chase would wire to Enron $95,691,275.00 • Enron and Chase would enter into new financial and physical hedges at the proposed volume and prices • The surety companies would provide a letter of consent agreeing to the amendments to the original transaction. Supporting letters of credit would remain in effect unchanged.

June ‘98 $250MM • Balances as of July 31, 2000 • Existing forward sale volumes • Transco Sta. 65 40,000 MMBtu/d • TGT/SL 25,000 MMBtu/d • Columbia Gulf La. 25,000 MMBtu/d • Forward sale remaining volumes MTM value: $(220,941,369) • Existing financial hedge fixed prices • Transco Sta. 65 $2.35065/MMBtu • TGT/SL $2.30065/MMBtu • Columbia Gulf La. $2.25315/MMBtu • Financial hedge MTM value: $86,607,756 • Existing daily cash flow: $207,871.00 • Restructure existing forward sale agreement by: • Proposed volumes would be: • Transco Sta. 65: 25,000 MMBtu/d • TGT/SL: 15,000 MMBtu/d • Columbia Gulf La.: 15,000 MMBtu/d • Margin reference price would be: $3.79/MMBtu on 55,000 MMBtu/d • Applicable delivery dates: August, 2000 through June, 2002 • Value of the volumes removed from the FSA: $85,908,953

June ‘98 $250MM (con’t) • Restructure financial and physical hedges by: • Existing hedges would be terminated • New financial hedge proposed volumes and prices would be: • Transco Sta. 65: 25,000 MMBtu/d @ $3.7610/MMBtu • TGT/SL: 15,000 MMBtu/d @ $3.7553/MMBtu • Columbia Gulf La.: 15,000 MMBtu/d @ $3.8345/MMBtu • New physical hedge would be struck under new physical master with Chase • Margin reference price: $3.79/MMBtu on 55,000 MMBtu/d • Applicable delivery dates: August, 2000 through June, 2002 • Value of the proposed financial hedge: $109,586 • Restructured daily cash flow would be: $207,872.00 • Transaction steps: • Enron restructures forward sale agreement with Mahonia, reducing volumes to be delivered according to the above proposal - in consideration, Enron would wire to Mahonia $85,908,953.00 • The financial and physical hedges between Enron and Chase would be terminated - in consideration, Chase would wire to Enron $86,498,070.00 • Enron and Chase would enter into new financial and physical hedges at the proposed volume and prices • The surety companies would provide a letter of consent agreeing to the amendments to the original transaction.

December ‘98 $250MM • Balances as of July 31, 2000 • Existing forward sale volumes • ARCO Cushing 391,000 Bbl/month • Forward sale remaining volumes MTM value: $(269,651,460) • Existing financial hedge fixed prices • ARCO Cushing $16.08/Bbl • Financial hedge MTM value: $103,730,044 • Existing monthly cash flow: $6,287,280.00 • Restructure existing forward sale agreement by: • Proposed volumes and prices (delivery point is ARCO Cushing): • Aug-00 to Jul-01: 222,000 Bbl/mo @ $28.33/Bbl • Jul-01 to Dec-02: 260,000 Bbl/mo @ $24.19/Bbl • Margin reference price: Same as above • Applicable delivery dates would be: August, 2000 through December, 2002 • Value of the volumes removed from the FSA: $102,393,904

December ‘98 $250MM (con’t) • Restructure financial and physical hedges by: • Existing hedges woul be terminated • New financial hedge proposed volumes and prices (delivery point is ARCO Cushing): • Aug-00 to Jul-01: 222,000 Bbl/mo @ $28.33/Bbl • Jul-01 to Dec-02: 260,000 Bbl/mo @ $24.19/Bbl • Physical hedge would be struck under new physical master with Chase • Margin reference price: Same as above • Value of the proposed financial hedge: $287,398 • Restructured monthly cash flow: $6,287,450.00 • Transaction steps: • Enron restructures forward sale agreement with Mahonia, reducing volumes to be delivered according to the above proposal - in consideration, Enron would wire to Mahonia $102,393,904.00 • The financial and physical hedges between Enron and Chase would be terminated - in consideration, Chase would wire to Enron $103,442,646.00 • Enron and Chase would enter into new financial and physical hedges at the proposed volume and prices • The surety companies would provide a letter of consent agreeing to the amendments to the original transaction.

June ‘99 $500MM • Balances as of July 31, 2000 • Existing forward sale volumes • Transco Sta. 65 50,000 MMBtu/d • TGT/SL 50,000 MMBtu/d • Columbia Gulf La. 40,000 MMBtu/d • Forward sale remaining volumes MTM value: $(606,701,479) • Existing financial hedge fixed prices • Transco Sta. 65 $2.4862/MMBtu • TGT/SL $2.4612/MMBtu • Columbia Gulf La. $2.4623/MMBtu • Financial hedge MTM value:$179,018,630 • Existing daily cash flow: $345,862.00 • Restructure existing forward sale agreement by: • Proposed volumes would be: Transco Sta. 65 TGT/SL Columbia Gulf La. • Aug-00 to Jul-01 31,000 MMBtu/d 25,000 MMBtu/d 31,000 MMBtu/d • Aug-01 to Jul-02 35,000 MMBtu/d 28,000 MMBtu/d 35,000 MMBtu/d • Aug-02 to Jul-03 41,000 MMBtu/d 31,000 MMBtu/d 41,000 MMBtu/d • Aug-04 to Jun-04 44,000 MMBtu/d 35,000 MMBtu/d 44,000 MMBtu/d

June ‘99 $500MM (con’t) • Proposed margin reference prices would be: • Aug-00 to Jul-01 $3.9888/MMBtu on 87,000 MMBtu/d • Aug-01 to Jul-02 $3.5385/MMBtu on 98,000 MMBtu/d • Aug-02 to Jul-03 $3.2285/MMBtu on 113,000 MMBtu/d • Aug-04 to Jun-04 $3.1509/MMBtu on 123,000 MMBtu/d • Value of the volumes removed: $179,526,085 • Restructure financial and physical hedges by: • Existing hedges would be terminated • New financial hedge proposed prices on the restructured volumes would be: Transco Sta. 65 TGT/SL Columbia Gulf La. • Aug-00 to Jul-01 $4.0100/MMBtu $3.9397/MMBtu $3.9697/MMBtu • Aug-01 to Jul-02 $3.5518/MMBtu $3.5176/MMBtu $3.5160/MMBtu • Aug-02 to Jul-03 $3.2714/MMBtu $3.1772/MMBtu $3.2385/MMBtu • Aug-04 to Jun-04 $3.1875/MMBtu $3.1772/MMBtu $3.1554/MMBtu • New physical hedge would be struck under new physical master with Chase • Restructured daily cash flow: $345,866.14 • Transaction steps: • Enron restructures forward sale agreement with Mahonia, reducing volumes to be delivered according to the above proposal - in consideration, Enron would wire to Mahonia $179,526,085.00

June ‘99 $500MM (con’t) • Transaction steps (con’t) • The financial and physical hedges between Enron and Chase would be terminated - in consideration, Chase would wire to Enron $180,753,564.00 • Enron and Chase would enter into new financial and physical hedges at the proposed volume and prices • The surety companies would provide a letter of consent agreeing to the amendments to the original transaction.

Action steps • Confirm prices and volumes are acceptable for each restructure (Chase) • Confirm that restructures are acceptable to Sureties (Enron) • Prepare documents (Enron, V&E) • Document review (Enron, Chase) • Trade execution & wire transfers (Enron/Chase/Mahonia)

![[Commodity Name] Commodity Strategy](https://cdn3.slideserve.com/6088618/commodity-name-commodity-strategy-dt.jpg)