Download

1 / 98

1.11k likes | 2.08k Views

CHAPTER 6 Bond Valuation Models. Key features of Bonds Bond valuation Measuring yield Assessing risk. Key Features of a Bond. Par value : face amount; paid at maturity. Assume $1,000.

E N D

CHAPTER 6 Bond Valuation Models • Key features of Bonds • Bond valuation • Measuring yield • Assessing risk

Key Features of a Bond • Par value: face amount; paid at maturity. Assume $1,000. • Coupon interest rate: stated interest rate. Multiply by par value to get dollar interest payment. Generally fixed.

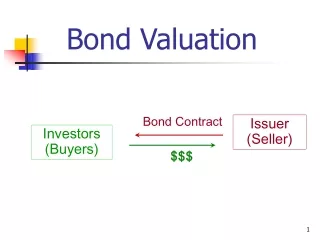

Maturity: years until bond must be repaid. Declines over time. • Issue date: date when bond was issued. • Call provision • Call Protection period • Call Premium • Default Risk • Special Features

How can we value assets on the basis of expected future cash flows? CF1 (1 + r)1 CF2 (1 + r)2 CFn (1 + r)n Value = + . . . . ABSOLUTELY FUNDAMENTAL.

How is the discount rate determined? The discount rate r is the opportunity cost of capital and depends on: • riskiness of cash flows. • general level of interest rates. • Inflation • Supply and Demand of Money and Credit • Production opportunities • Time profile of consumption

How is the discount rate determined? Again, the discount rate r is the opportunity cost of capital. i.e. the rate of return that could be earned on alternative investments of similar risk. Remember: ri = r* + IP + LP + MRP + DRP for debt securities.

The cash flows of a bond consist of: • The coupon payments (an annuity). • A lump sum (the maturity, or par, value to be received in the future). Value =Present Value of the interest annuity and the Present value of the maturity value.

Find the value of a 10-year annual coupon bond, when rd = 10%. 0 1 2 10 100 100 100 1,000

Two Ways to Solve Using tables: Value = INT(PVIFA10%,10)+ M(PVIF10%,10). Calculator: Enter: Solve for PV = $1,000, or 100% of Par. Computer: 10 10 100 1000 N I/YR PV PMT FV

PV annuity PV maturity value Value of bond $ 614.46 385.54 $1,000.00 = = = The bond consists of a 10-year, 10% annuity of $100/year plus a $1,000 lump sum at t = 10: INPUTS 10 10 100 1000 N I/YR PV PMT FV -1,000 OUTPUT

Find the value of a similar 20-year annual coupon bond, when rd = 10%. 0 1 2 20 100 100 100 1,000

Rule:When the required rate of return (rd) equals the coupon rate, the bond value (or price) equals the: ?

What would the value of the bonds be if inflation rose causing kd= 13%? N I/YR PV PMT FV Solution: ?

10-year, 10% coupon bond, rd =13% 10 13 100 1000 I/YR PMT N PV FV Solution: -837.21 or 83.72% of par.

What if it were a 20 year, 10% annual coupon bond, with rd = 13%? 20-year, 10% coupon bond 20 13 100 1000 N I/YR PV PMT FV Solution: -789.25, or 78.925% of Par

When rd rises above the coupon rate, bond values fall below par. • They sell at adiscount: A Discount Bond

What would the value of the bonds be if rd = 7%? 10-year bond 10 7 100 1000 N I/YR PV PMT FV Solution: -1210.71, (Price 121.07)

What would the value of the bonds be if rd = 7%? 20-year bond 20 7 100 1000 N I/YR PV PMT FV Solution: -1317.82, (Price 131.78)

When rd falls below the coupon rate, bond values rise above par. They sell at apremium: A PREMIUM BOND.

What would happen over time to the value of a 10 % coupon, 30 bond if (1)interest rates stayed at 10%?(2)If interest rates immediately rose to 13% and stayed there?(3)If interest rates immediately fell to 7.5% and stayed there?

If interest rates stay at 10% • Value of 30 year bond? • $1000. • Value of 10 year bond? • $1000 • Value of 1 year bond? • $1000

If interest rates rise to 13% and stay there? • Value of 30 year bond? • $775.13 • Value of 10 year bond? • $837.21 • Value of 1 year bond? • $973.45

If interest rates fell to 7% and stayed there? • Value of 30 year bond? • $1372.27 • Value of 10 year bond? • $1210.71 • Value of 1 year bond? • $1028.04

Value of 30 year, 10% coupon bond over time: rd = 7% 1372 1211 1000 837 775 rd = 10% M rd = 13% 30 20 10 0 Years to Maturity NOTE: Not symmetric

Value of 30 year, 10% coupon bond over time: rd = 7% 1372 1211 1000 837 775 rd = 10% M rd = 13% 30 20 10 0 Years to Maturity BULLET-VIC

What if 100 year bond? • $769.23 if k = 13% • $1000 if k = 10% • $1428.07 if k = 7% Cf9-23 Cf9-24

Summary If rd remains constant: • At maturity, the value of any bond must equal its par value. • Over time, the value of a premium bond will decrease to its par value. • Over time, the value of a discount bond will increase to its par value. • A par value bond will stay at its par value.

Value of 30 year, 10% coupon bond over time: rd = 7% 1372 1211 1000 837 775 rd = 10% M rd = 13% 30 20 10 0 Years to Maturity ACTUAL BOND PRICE PROFILE

What is “yield to maturity”? YTM is the rate of return earned on a bond held to maturity. Also called “promised yield”; or That discount rate which equates PV (Bond’s CF) to its price.

What is the YTM on a 10-year, 9% annual coupon, $1,000 par value bond that sells for $887? 0 1 9 10 rd=? 90 90 90 1,000 PV1 . . . PV10 PVM Find rd that “works”! 887

First, what does the fact that this is a discount bond tell you about the relationship between rd and the bond’s coupon rate?

Find rd INT (1 + rd)1 INT (1 + rd)N M (1 + rd)N VB = + . . . + + 90 (1 + rd)1 90 (1 + rd)10 1,000 (1 + rd)10 887 = + . . . + + . 10 -887 90 1000 N I/YR PV PMT FV 10.91 Computer: (e-1) INPUTS OUTPUT

Find YTM if price were $1,134.20. 10 -1134.2 90 1000 N I/YR PV PMT FV 7.08 INPUTS OUTPUT Sells at a premium. Because coupon = 9% > rd = 7.08%, bond’s value > par. Computer:

If coupon rate > rd, premium. • If coupon rate < rd, discount. • If coupon rate = rd, par bond. • If rd rises (falls), price falls (rises). • At maturity, price = par.

Definitions Annual coupon pmt Current price Current yield = . Cap gains yld = . = YTM = + . Change in price Beg of period price Exp total return Exp Curr yld Exp cap gains yld

Find current yield and capital gains yield for a 9%, 10-year bond when the bond sells for $887 (and YTM = 10.91%.) $90 $887 Current yield = = 0.1015 = 10.15%.

Remember: YTM = Current yield + Capital gains yield. Therefore, Shortcut Answer: Cap gains yield = YTM - Current yld. = 10.91% - 10.15% = 0.77%. Could also find values in Years 0 and 1, get difference, and divide by value in Year 0. Same answer.

Proof: • Value of a 9 year, 9% coupon bond if YTM = 10.91? • $893.87 • (P1 - P0)/ P0 = ($893.87 - $887)/$887 = .0077 = .77%

10-year, 9% coupon bond with price = $1,134.20 (YTM = 7.08%) $90 $1,134.20 Current yield = = 7.94%. Capital gains yield = 7.08% - 7.94% = -0.85%.

9 year, 9% coupon bond, YTM = 7.08%;Price = $1124.52 (P1 - P0)/P0 = 1124.52 - 1134.20 1134.20 = -0.85%

What is interest rate (price)risk? Does a 1-yr or 10-yr 10% bond have more price risk? Price risk: Rising rd causes bond’s price to fall. rd 1-year Change 10-year Change 5% $1,048 $1,386 10% 1,000 4.8% 1,000 38.6% 15% 956 4.4% 749 25.1%

Value 10-year 1500 1-year 1000 500 kd 0 0% 5% 10% 15%

DURATION a measure of price risk • Duration = Sum( witi)where • wi =PV ( CFi)/ sum (PV ( CFi)) • = PV ( CFi)/ Price • ti = time to the ith cash flow

DURATION • e.g. [PV(CF1)/P] x 1 + • [PV(CF2)/P] x 2 + [PV(CF3)/P] x 3 + ... +[PV(CFn)/P] x n

What is the duration of a 1 year 10% coupon bond, rd = .10 • 0 1 • 1100

What is the duration of a 2 year 10% coupon bond, rd = .10 • Cash flows: 0 1 2 100 1100

What is the duration of a 2 year 10% coupon bond, rd = .10 • Duration = [((100/(1.1))/1000)*1] + [((1100/(1.1)2)/1000)*2] = • Greater Interest rate risk than a 1 year bond. 1.91

DURATION • WHAT IS DURATION OF A 2 YEAR ZERO COUPON BOND?