Download

1 / 22

220 likes | 325 Views

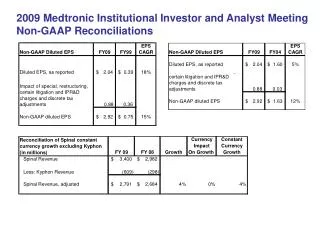

Euromoney Institutional Investor PLC. 2008 Half Year Results Presentation Colin Jones, FD May 15, 2008. 2008 HALF YEAR. Financial Review Trading Review Strategy/Outlook. RECORD RESULTS. 1 As reconciled in note 15. HIGHLIGHTS.

E N D

Euromoney Institutional Investor PLC 2008 Half Year Results Presentation Colin Jones, FD May 15, 2008

2008 HALF YEAR • Financial Review • Trading Review • Strategy/Outlook 2

RECORD RESULTS 1As reconciled in note 15 3

HIGHLIGHTS • Record results despite global credit crisis and volatility in financial markets • Strong results prove strategy is working: • More robust, subscription-driven business: subs revenue up 15%, now 37% of total vs 35% • Flexible, international business - significant exposure to emerging markets provides geographic opportunities and counters dependence on global institutions • More diverse post-MB acquisition – continued strength of commodities, energy and legal sectors • Continued investment in marketing and new products (£1m+), esp subscriptions / electronic 4

CASH FLOW AND NET DEBT £12.8m £42.4m £7.7m £13.4m £5.7m £204.6m £201.8m Cash conversion 117% Q1 IMS debt £191.6m FY 07 Acquisitions Dividend Tax Other (Interest, Capex, FX) Operating Cash Flow FY 08 5

NET FINANCE COSTS see note 5 6

TAX see note 6 7

2008 HALF YEAR • Financial Review • Trading Review • Strategy/Outlook 8

TRADING BACKGROUND • Global macro concerns and credit crisis limited impact on results • Growth in advertising / sponsorship slowed as expected… • …. but subscription and delegate revenues resilient • Emerging markets continue to provide growth opportunities and extend customer base • Business better balanced across both geographies and sectors • No dependence on any one customer – Top 20 = 20% • Tight cost control but no contingency plans implemented and no cuts in marketing / investment • Adjusted operating margin unchanged 23% • Some negative currency impact 9

FINANCIAL PUBLISHING • Revenue £0.5m (-1%) Profit level £9.4m Margin unchanged 24% • Subscription revenues up as move online • Advertising revenues fell across most titles - notable exceptions: Euromoney & Asiamoney • Thriving emerging markets driving new customer base 13

BUSINESS PUBLISHING • Revenue £2.6m (+13%) Profit £2.1m (+39%) Margin 33% vs 27% • Four sectors – metals, energy, legal & telecoms – all buoyant markets • Excellent performances: • Metal Bulletin cost and revenue synergies • Legal Publishing • TelCap / Capacity 14

TRAINING • Revenue £1.5m (+9%) Profit £0.1m (-2%) Margin 25% vs 27% • Continued 2007 revenue growth through increased course volumes, but… • …margin hit by lower avg delegate numbers and increased costs • Actions to correct take effect in H2 15

CONFERENCES & SEMINARS • Revenue £4.3m (+11%) Profit £0.1m (+1%) Margin 26% vs 28% • Timing differences • Pressure on big ticket sponsorship and events in structured finance….. • ….. offset by growth in delegate-driven events and emerging market focus • II Membership revenue up 20%, renewal steady at 90% 16

DATABASE & INFO SERVICES • Revenue £5.9m (+24%) Profit £1.2m (+14%) Margin 32% vs 35% • Record sales and revenue performances from BCA and ISI • Demonstrates value of quality, hard-to-get data esp in difficult markets • Investment in new products – DealWatch and CEIC expansion 17

2008 HALF YEAR • Financial Review • Trading Review • Strategy/Outlook 18

STRATEGY UPDATE • Group more focused, more robust and higher quality than 2001 – better downside protection • Maintain margin: • Operational gearing • Focus on low margin product and cost control just as rigorous – but no “fat” • Drive organic growth: • Invest in high growth subscription products esp electronic • Focus on quality over quantity – build existing brands • Flexibility to roll out successes quickly to new geographies • Selective acquisitions to accelerate strategy 19

REVENUE MIX (1) 2003 Other 2008 7% Advertising Other Delegates Advertising 4% 22% 34% Delegates 18% 28% 7% 30% Sponsorship 13% 37% Sponsorship Subscriptions Subscriptions 20

REVENUE MIX (2) 2003 Data 2008 9% Publishing Publishing Data Events 20% 35% 56% 40% 40% Events 21

OUTLOOK • April revenue and profits strong, Q3 outlook positive, limited September visibility as usual • Stronger H2 cash flows • Minimal timing, acquisition, FX etc impact • Continue to focus on successful strategy: • Invest in increasing subscription base • Extend emerging market coverage… • …and broaden sector coverage – commodities, energy etc • Market expectations for tougher H2 and 2009 • Watch closely for further signs of downturn and react quickly - cost base is flexible • Stronger than ever and positioned for growth 22