Download

1 / 19

210 likes | 544 Views

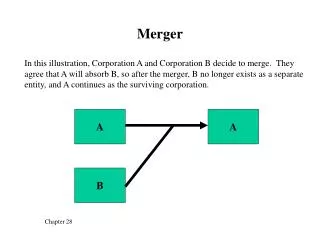

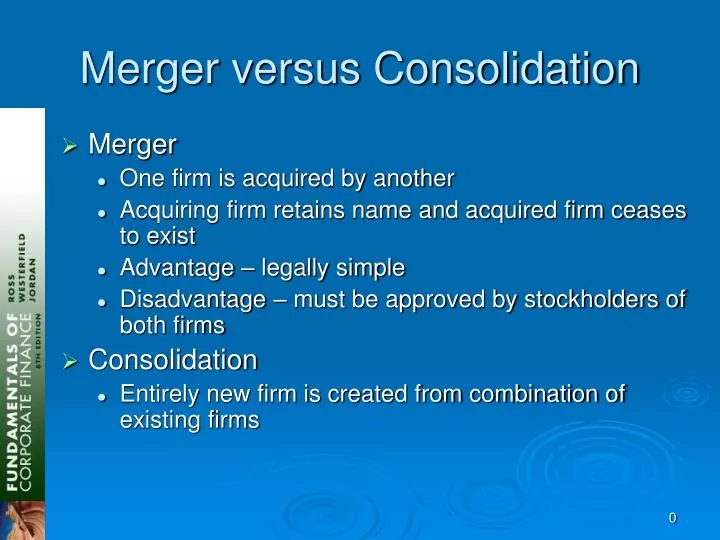

Merger versus Consolidation. Merger One firm is acquired by another Acquiring firm retains name and acquired firm ceases to exist Advantage – legally simple Disadvantage – must be approved by stockholders of both firms Consolidation

E N D

Merger versus Consolidation • Merger • One firm is acquired by another • Acquiring firm retains name and acquired firm ceases to exist • Advantage – legally simple • Disadvantage – must be approved by stockholders of both firms • Consolidation • Entirely new firm is created from combination of existing firms

Acquisitions • A firm can be acquired by another firm or individual(s) purchasing voting shares of the firm’s stock • Tender offer – public offer to buy shares • Stock acquisition • No stockholder vote required • Can deal directly with stockholders, even if management is unfriendly • May be delayed if some target shareholders hold out for more money – complete absorption requires a merger • Classifications • Horizontal – both firms are in the same industry • Vertical – firms are in different stages of the production process • Conglomerate – firms are unrelated

Takeovers • Control of a firm transfers from one group to another • Possible forms • Acquisition • Merger or consolidation • Acquisition of stock • Acquisition of assets • Proxy contest • Going private

Taxes • Tax-free acquisition • Business purpose; not solely to avoid taxes • Continuity of equity interest – stockholders of target firm must be able to maintain an equity interest in the combined firm • Generally, stock for stock acquisition • Taxable acquisition • Firm purchased with cash • Capital gains taxes – stockholders of target may require a higher price to cover the taxes • Assets are revalued – affects depreciation expense

Accounting for Acquisitions • Pooling of interests accounting no longer allowed • Purchase Accounting • Assets of acquired firm must be reported at fair market value • Goodwill is created – difference between purchase price and estimated fair market value of net assets • Goodwill no longer has to be amortized – assets are essentially marked-to-market annually and goodwill is adjusted and treated as an expense if the market value of the assets has decreased

Synergy • The whole is worth more than the sum of the parts • Some mergers create synergies because the firm can either cut costs or use the combined assets more effectively • This is generally a good reason for a merger • Examine whether the synergies create enough benefit to justify the cost

Revenue Enhancement • Marketing gains • Advertising • Distribution network • Product mix • Strategic benefits • Market power

Cost Reductions • Economies of scale • Ability to produce larger quantities while reducing the average per unit cost • Most common in industries that have high fixed costs • Economies of vertical integration • Coordinate operations more effectively • Reduced search cost for suppliers or customers

Taxes • Take advantage of net operating losses • Carry-backs and carry-forwards • Merger may be prevented if the IRS believes the sole purpose is to avoid taxes • Unused debt capacity • Surplus funds • Pay dividends • Repurchase shares • Buy another firm • Asset write-ups

Reducing Capital Needs • A merger may reduce the required investment in working capital and fixed assets relative to the two firms operating separately • Firms may be able to manage existing assets more effectively under one umbrella • Some assets may be sold if they are redundant in the combined firm (this includes human capital as well)

General Rules • Do not rely on book values alone – the market provides information about the true worth of assets • Estimate only incremental cash flows • Use an appropriate discount rate • Consider transaction costs – these can add up quickly and become a substantial cash outflow

EPS Growth • Mergers may create the appearance of growth in earnings per share • If there are no synergies or other benefits to the merger, then the growth in EPS is just an artifact of a larger firm and is not true growth • In this case, the P/E ratio should fall because the combined market value should not change • There is no free lunch

Diversification • Diversification, in and of itself, is not a good reason for a merger • Stockholders can normally diversify their own portfolio cheaper than a firm can diversify by acquisition • Stockholder wealth may actually decrease after the merger because the reduction in risk, in effect transfers wealth from the stockholders to the bondholders

Cash Acquisition • The NPV of a cash acquisition is • NPV = VB* – cash cost • Value of the combined firm is • VAB = VA + (VB* - cash cost) • Often, the entire NPV goes to the target firm • Remember that a zero-NPV investment may also desirable

Stock Acquisition • Value of combined firm • VAB = VA + VB + V • Cost of acquisition • Depends on the number of shares given to the target stockholders • Depends on the price of the combined firm’s stock after the merger • Considerations when choosing between cash and stock • Sharing gains – target stockholders don’t participate in stock price appreciation with a cash acquisition • Taxes – cash acquisitions are generally taxable • Control – cash acquisitions do not dilute control

Defensive Tactics • Corporate charter • Establishes conditions that allow for a takeover • Supermajority voting requirement • Targeted repurchase A.K.A. greenmail • Standstill agreements • Poison pills (share rights plans) • Leveraged buyouts

More (Colorful) Terms • Golden parachute • Poison put • Crown jewel • White knight • Lockup • Shark repellent • Bear hug • Fair price provision • Dual class capitalization • Countertender offer

Evidence on Acquisitions • Shareholders of target companies tend to earn excess returns in a merger • Shareholders of target companies gain more in a tender offer than in a straight merger • Target firm managers have a tendency to oppose mergers, thus driving up the tender price • Shareholders of bidding firms earn a small excess return in a tender offer, but none in a straight merger • Anticipated gains from mergers may not be achieved • Bidding firms are generally larger, so it takes a larger dollar gain to get the same percentage gain • Management may not be acting in stockholders’ best interest • Takeover market may be competitive • Announcement may not contain new information about the bidding firm

Divestitures and Restructurings • Divestiture – company sells a piece of itself to another company • Equity carve-out – company creates a new company out of a subsidiary and then sells a minority interest to the public through an IPO • Spin-off – company creates a new company out of a subsidiary and distributes the shares of the new company to the parent company’s stockholders • Split-up – company is split into two or more companies and shares of all companies are distributed to the original firm’s shareholders