Download

1 / 41

410 likes | 416 Views

Learn about compound interest, its benefits, and its application in the analysis of gross income. Explore the impact of time on money and understand the difference between compound and simple interest.

E N D

Chapter 2: Analysis of Gross Income Chapter Objectives • Define the comparisons between simple and compound interest. • Describe how to forecast future cost based on a compounded rate. • Identify which column of compound interest is applicable to developing the Income Approach. • Describe the impact of time on money.

Chapter 7: Compound Interest and the Net Operating Income Chapter Introduction • Compound Interest • Answers the benefit of borrowing opposed to paying cash • Opportunity costs of an investment through debt leveraging • A useful technique that incorporates the assumption of change over time when performing an appraisal

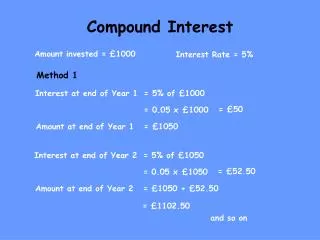

Chapter 7: Compound Interest and the Net Operating Income Compound Interest vs. Simple Interest • Compound Interest vs. Simple Interest • Difference in how the interest is applied • Simple interest loan • Divide the interest to be charged in equal payments over the life of the loan • Compound Interest Loan • Payments made will majorly reduce the interest charged on the loan first • Principal will be proportionately increased minimally over the initial years

Chapter 7: Compound Interest and the Net Operating Income Compound Interest vs. Simple Interest (cont.) Simple Interest vs. Compound Interest Comparative Recapitulation See Page 83 to review a Comparative Debt Reduction: Simple Interest vs. Compound Interest Method

Chapter 7: Compound Interest and the Net Operating Income Compound Interest Chart: The Time It Represents • Compound Interest Chart • Impact of time on $1 can be seen from the future and present time perspective • See Page 83 to review the chart revealing an explanation and overview of each symbol present in the compound interest chart

Chapter 7: Chapter Title Compound Interest Chart at 6% Interest • Examine the 6% Compound Interest Chart presented on Page 84 • Based on an annual rate of compound interest • Every number represents the impact of time on $1 at a specific compounded rate of interest • The first 3 columns are based on future value or the forecasting of what $1 will be • Sinking Fund Factor • Chart forecasts what annual payments are needed to reach $1 if the payment is deposited in a compound interest bearing account • Compound interest problems are solved by multiplying a specific number of dollars by the applicable factor.

Chapter 7: Compound Interest and the Net Operating Income Working with the FW1: Time and Rate of Interest Impact on $1 • FW1 • Reveals the future worth of $1 • Result of a future amount or value of $1 deposited and left in the interest bearing account

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.1 Working with the compound interest charts (3% and 5%) provided on Page 85, answer the questions that focus on the forecasting of $1 utilizing FW1 factors. • What would $1 be worth if it were deposited today in an interest-bearing account that paid 5% over a 10 year term? $1 x 1.628895 = $1.63 • The roof has a cost new of $4,200. What will the roof cost in four years, if inflation is rising at a compounded rate of 3%? FW1 Factor 1.125509 Roof Cost Today x $4,200 Future Cost $4,727.14

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.1 (cont.) • The monies received from an unexpected windfall were $12,000. If that money is deposited in an interest-bearing account at 5%, how much money would be available in seven years? 1.407100 (FW1 Factor) X $12,000(Dollar Amount of Windfall) $16,885.20 (Money Available in Seven Years) • There were two investments being looked at, one at a slightly higher risk than the other. What is the difference in gain between 3% and 5% over six years on a $2,500 deposit? FW1 Factor @3% 1.194052 @5% 1.340096 Amount of Deposit x 2,500x 2,500 Future Value of Deposit $2,985.13 $3,350.24 $3,350.24-$2,985.13=$365.11 (Difference in Gain)

Chapter 7: Compound Interest and the Net Operating Income Working with the FW1/P: Time and Rate of Interest • FW1/P • Future Worth of $1 per period • A compound interest factor that forecasts the future value of level stream $1 deposits each period of the holding term of the investment • The FW1/P $1 will be deposited each year into a compounded rate of interest account.

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.2 Using the FW1/P Column provided on Page 86 answer the following question. • Using data from the excerpted FW1/P column above, find the difference between $1 deposited each year in an interest bearing account compounding at a rate of 6% over a five year period versus continuing the same dollar deposits in the account for eight years? Solve by going to the second column, years 5 and 8; find the future value of $1 deposited each year for 5 years and 8 years to see the difference. The dollars will grow additionally $4.77 over the three-year term difference at 6%. (10.636628-5.866601 = 4.77)

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.3 Working with the compound interest charts (3% and 5%) provided on Page 87, answer the questions that focus on the forecasting of $1 utilizing FW1/P factors. • What would be the balance if $1 was deposited annually into an interest-bearing account that paid 5% over a 10 year term? FW1/P = 12.577893 • Deposits of $1,100 are planned to be annually deposited each year for seven years, at a compounded rate of 3%. How much money will be available in the future? 7.662462 (FW1/P) X $1,100 (Annual Deposit) $8,428.71 (Money Available)

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.3 (cont.) • What is the difference in gain between 3% and 5% compound interest over four years on a $500 annual deposit? FW1/P deposits @3% 4.183627 @5% 4.310125 Annual Deposit x $500x $500 Future Value $2,091.81 $2,155.06 Difference $2,155.06 - $2,091.81 = $63.25

Chapter 7: Compound Interest and the Net Operating Income Time and Rate of Interest Impact on $1: Sinking Fund Factor • Sinking Fund Factor • Used to calculate how much money needs to be held in a reserve account • Requires the need to identify the future cost at the time the short-item needs to be replaced • The factor is identified based on the number of years and the compounded rate • When multiplied by that future cost, the factor will conclude the annual amount that needs to be held from the income stream and deposited into an interest bearing account

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.4 Using the Sinking Fund Factor Column provided on Page 88 answer the following question. • What is the difference between the amount that needs to be deposited each year in an interest-bearing account compounding at a rate of 6% over five years versus eight years if $1 is needed in the future? Solve by going to the second column, Years 5 and 8, and find the sinking fund factor of deposits each year for five years and eight years to see the amounts needed to reach a future $1. The difference in the annual deposits necessary to reach $1 is $0.08 (0.177396 – 0.101036 = 0.08).

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.5 Working with the compound interest charts (3% and 5%) provided on Page 89, answer the questions that focus on the forecasting of $1 utilizing SFFfactors. • How much money would need to be deposited annually in an interest-bearing account paying 5% over a ten-year term, in order to reach $1? SFF = $ 0.079505 or 8¢ • In three years, a couple will have a dependent who will require $4,000 in order to attend a school of fine arts for one year. The cost of moving expenses and a housing deposit will be another $14,000. How much money will need to be deposited in a 5% compounded interest account to reach the amount necessary? 0.317209 (SFF in Three Years @5%) X $18,000 (Total Amount Needed in Three Years) = $5,709.76 (Money to Deposit)

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.5 (cont.) • What is the difference in deposits between 3% and 5% compound interest over nine years, when the goal is to end with a sum of $10,000? SFF Factors @3% 0.098434 @5% 0.090690 Amount Needed x $10,000 x $10,000 Annual Deposits Needed $984.34 $906.90 Difference $984.34 – $906.90 = $77.44

Chapter 7: Compound Interest and the Net Operating Income Time and Rate of Interest Impact on $1: PW1 • PW1 • Present Worth of $1 • A compound interest factor that discounts a future $1 deposited into a current value

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.6 Using the PW1 Column provided on Page 90 answer the following question. • What is the difference in the current value of $1 to be received over five years versus eight years when the discount rate is compounding at 6%? To solve, look in the fourth column under years 5 and 8 to find the present value of the $1. The dollar will be worth $0.12 less if received three years earlier at 6%. 0.747258 – 0.627412 = $0.12

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.7 Working with the compound interest charts (3% and 5%) provided on Page 91, answer the questions that focus on the forecasting of $1 utilizing PW1 factors. • What would a dollar, anticipated to be received in 10 years, be worth today if the discount rate is 5%? PW1 = $0.613913 • The roof in five years will have a future cost new of $4,200. Considering inflation at a compounded rate of 3%, what is the current cost of the roof? 0.862609 (PW1) X $4,200.00 (Future cost of roof) = $3,622.96 (Current cost of roof)

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.7 (cont.) • A small lot is projected to be worth of $12,000 in seven years. What is the current value of the lot at a discount rate of 5%? PW1 @5% 7 years 0.710681 Future value of lot x $12,000.00 Current value of lot $8,528.17 • How much more can be paid for a property (which is projected in six years to be worth $75,000) if the discount rate is 3% as opposed to 5%? At which rate would the higher yield be gained? PW1 in 6 yr.’s @3% 0.837484 @5% 0.746215 FV of Property x $75,000.00x $75,000.00 Present Value $62,811.30 $55,966.13 Difference $62,811.30 - $55,966.13 = $6,845.17 The higher yield would be gained a 5%. If you paid $55,966.13 today instead of $62,811.30 you would gain a higher profit at the projected $75,000.

Chapter 7: Compound Interest and the Net Operating Income Time and Rate of Interest Impact on $1: PW1/P • PW1/P • Present Worth of $1 per period • A compound interest factor that discounts the future value of level stream $1 payments during each period of the future holding term of the investment • Used most often by appraisers to prove sufficiency of a reserve for replacement fund • Used to value a lease

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.8 Using the PW1/P Column provided on Page 92 answer the following question. • What is the difference between a series of $1 payments to be received each year in the future when the discount rate is 6% over the next five-year period versus continuing the $1 deposits discounted over an eight-year period? Solve by going to the fifth column, Years 5 and 8. Find the current value of $1 payments received each year for five years and eight years. Subtract the smaller number from the larger number to find the difference between the two time periods, which is $2. Factors: 6.209794 – 4.212364 = 1.99743

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.9 Working with the compound interest charts (3% and 5%) provided on Page 93, answer the questions that focus on the forecasting of $1 utilizing PW1/P factors. • What would $1, anticipated to be received each year for ten years in the future, be worth today if the discount rate was 5%? PW 1/P factor = $7.721735 • The lease payable at the end of a term has five remaining years. The annual rent scheduled on the lease is $15,700 per year. What is the value of that lease, if it is based on a discount rate of 3%? PW 1/P 4.579707 Lease Pmt.’s x $15,700.00 Current Value of Lease $71,901.40

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.9 (cont.) • Land rent has been agreed to be paid at the end of each year in the annual amount of $12,000 over an eight-year period. What is the current value of that lease at a discount rate of 5%? PW1/P 6.463213 Lease Pmt.’s x $12,000.00 Current Value of Lease $77,558.56

Chapter 7: Compound Interest and the Net Operating Income Time and Rate of Interest Impact on $1: Amortization • Amortization • Amortization of $1 • A compound interest factor that calculates the principal and interest payments of $1 borrowed in the present during each payment period of the future amortization term • Used to calculate the principal and interest re-payment of the loan • Key in the computation of capitalization rates

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.10 Using the Amortization Column provided on Page 94 answer the following question. • What is the difference between principal and interest payments each year on the $1 borrowed, when the loan rate is 6% over a five-year amortization period, versus an eight year amortization period? (0.237396 – 0.161036 = 0.076360 or $0.08) Solve by going to the sixth column, Years 5 and 8; find the principal and interest payments on $1 borrowed today for five years and eight years. The dollars of difference in principal and interest payments between the two loan terms is $0.08 over the three-year loan term difference.

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.11 Working with the compound interest charts (3% and 5%) provided on Page 95, answer the questions that focus on the forecasting of $1 utilizing Amortization factors. • What would the principal and interest payment of $1 borrowed today be, if the amortization term is ten years and the interest rate is 5%? Amortization Factor = $0.129505 or 13¢ • An amount to be borrowed is $15,000. What is the loan payment on a loan/amortization interest rate of 3%, if the loan term is eight years? Amortization Factor $0.142456 (or 14¢ for each $1 borrowed) Loan Value x $15,000 Loan Payment $2,136.84

Chapter 7: Compound Interest and the Net Operating Income Apply Your Knowledge 7.11 (cont.) • A sale price is $70,000. The owners are willing to finance the property over 10 years at an A.P.R. of 5%, based on an LTV ratio of 70/30. What would the principal and interest payments be? Sale Price $70,000 x LTVX .70 = Loan Value $49,000 x Amortization Factorx 0.129505 = P & I Payments $6,345.75

Chapter 7: Compound Interest and the Net Operating Income Summary • Compound interest allows the impact of time to be considered in the value. • Reserves for replacement will let the compounding rate of interest help pay for the future cost needed to replace short-lived items. • All compound interest factors are based on $1. • Compound interest factors are based on either forecasting the future, or discounting the future into a present. • Simple interest loans will have a greater amount of interest paid over the same loan term when compared to compound interest.

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 1. What is the primary difference between compound and simple interest? • Compound and simple interests are interchangeable terms. There is no difference. • Compound interest is generally a short-term holding period. • The interest is applied differently in each case. • Payments are higher in a simple interest loan.

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 2. If costs are rising at 6% per year, what will the carpet (with a current cost of $3,000) cost in five years? • $2,450.13 • $3,180.45 • $4,014.68 • $5,789.35

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 3. Which compound interest factor is used to estimate annual payments to deposit for the reserves for replacement? • amortization • FW1/P • PW1 • sinking fund factor

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 4. In developing a cap rate using the Band of the Investment method, which factor would be used to calculate the lender component known as the RM ? • amortization • PW1 • PW1/P • sinking fund factor

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 5. In four years, a property’s appliances are estimated to have a future cost of $2,500. If the reserve account is paying 6% at a compounded rate, what annual payments must be deposited to reach that future amount? • $250.98 • $328.34 • $571.48 • $625.12

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 6. To amortize means to • divide equally. • establish a performance ratio. • kill off slowly. • set aside reserve funding.

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 7. If land is currently worth $50,000, what will it be worth at the end of a projected investment holding term for eight years, if prices are rising at a compounded rate of 6%? • $79,692.40 • $82,765.32 • $83,456.89 • $101,934.78

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 8. What factor would be used to discount a lease? • amortization • FW1/P • PW1/P • sinking fund factor

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 9. What is the amount that must be held annually in a reserve account for a roof projected to cost $7,000 in 12 years, based on a 6% compound interest bearing account? • $414.94 • $583.33 • $637.25 • $708.28

Chapter 7: Compound Interest and the Net Operating Income Chapter 7 Quiz 10. Compound interest allows the factor of ____________ to be considered in the value. • employment rates • exchange rates • federal taxes • time