Download

1 / 2

20 likes | 32 Views

<br><br><br>Gloster Limited (Gloster), the listed company announced the group re-structuring where Gloster got merged with Kettlewell Bullen & Company Limited (KBC), the promoter group holding company having other investments and immovable property and earlier listed on Calcutta stock exchange now unlisted. For more details, Visit at - http://www.huconsultancy.com/blog/gloster-reverse-merger/

E N D

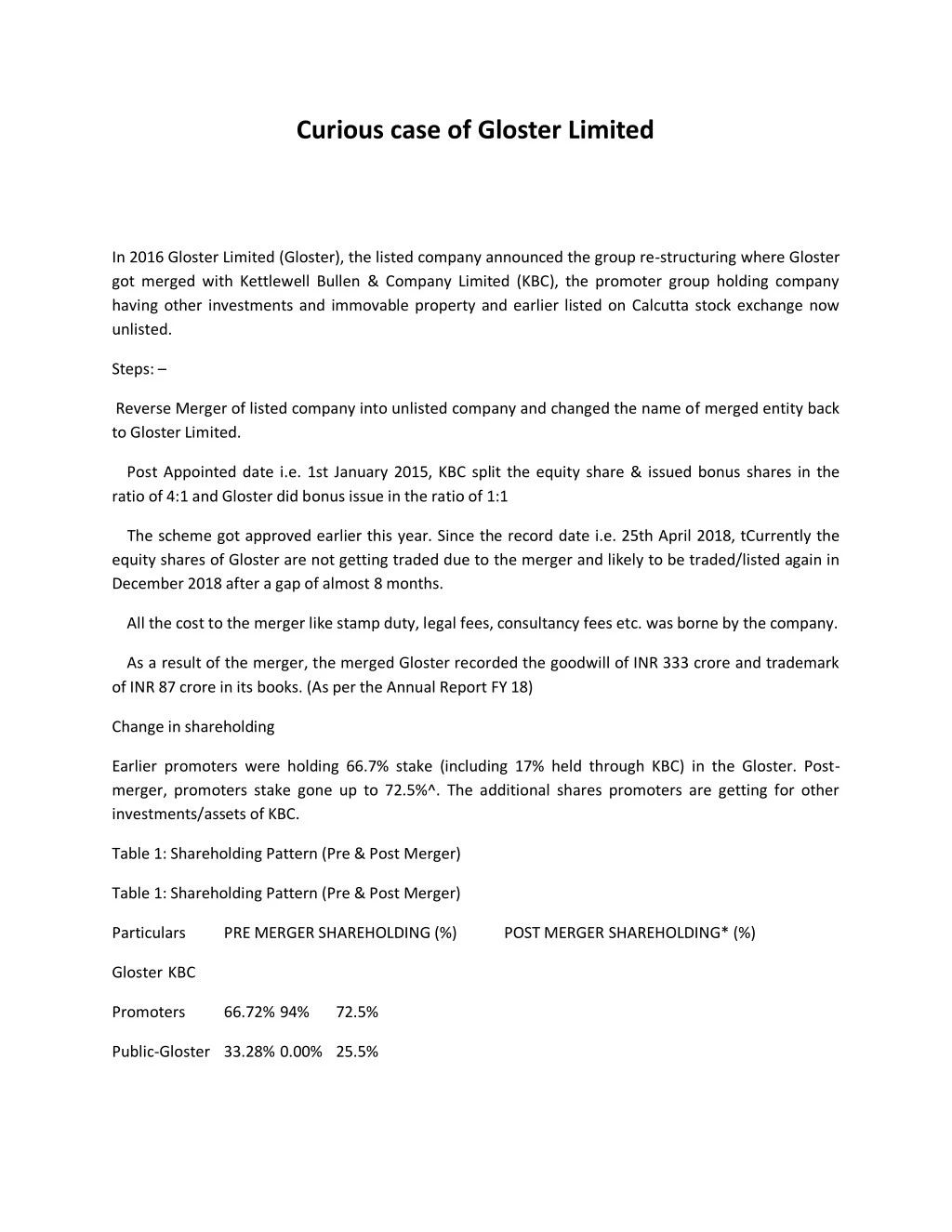

Curious case of Gloster Limited In 2016 Gloster Limited (Gloster), the listed company announced the group re-structuring where Gloster got merged with Kettlewell Bullen & Company Limited (KBC), the promoter group holding company having other investments and immovable property and earlier listed on Calcutta stock exchange now unlisted. Steps: – Reverse Merger of listed company into unlisted company and changed the name of merged entity back to Gloster Limited. Post Appointed date i.e. 1st January 2015, KBC split the equity share & issued bonus shares in the ratio of 4:1 and Gloster did bonus issue in the ratio of 1:1 The scheme got approved earlier this year. Since the record date i.e. 25th April 2018, tCurrently the equity shares of Gloster are not getting traded due to the merger and likely to be traded/listed again in December 2018 after a gap of almost 8 months. All the cost to the merger like stamp duty, legal fees, consultancy fees etc. was borne by the company. As a result of the merger, the merged Gloster recorded the goodwill of INR 333 crore and trademark of INR 87 crore in its books. (As per the Annual Report FY 18) Change in shareholding Earlier promoters were holding 66.7% stake (including 17% held through KBC) in the Gloster. Post- merger, promoters stake gone up to 72.5%^. The additional shares promoters are getting for other investments/assets of KBC. Table 1: Shareholding Pattern (Pre & Post Merger) Table 1: Shareholding Pattern (Pre & Post Merger) Particulars PRE MERGER SHAREHOLDING (%) POST MERGER SHAREHOLDING* (%) Gloster KBC Promoters 66.72% 94% 72.5% Public-Gloster 33.28% 0.00% 25.5%

Public-KBC Total 100% 100% 100% 0.00% 6% 2% This can change slightly. The value assigned to these other investments/assets while arriving at swap ratio is around INR 320 crore^^. I am not very sure about how such a huge value derived to the rest business of KBC as the position of KBC as on 31st March 2017 was^^^: The last news uploaded on BSE was on 18.04.2018. Further, half of the tabs on the company’s website are not working properly and doesn’t have complete information available (Even the shareholding pattern uploaded is as on 31st March 2018). Since the last 5 months, shareholders don’t have access to the complete information. Neither the company website or exchanges have such provisions of uploading the information as a listed company bound to. Commercial Reasons, if any, for the reverse merger and accounting huge intangible assets needs to be articulated by the company which resulted in no exit opportunity and price discovery for the long for public shareholders (which includes LIC with 22% pre-merger stake). If KBC had no business synergetic or otherwise and only some surplus assets and investments how it will create value for the listed company which is already having surplus assets of INR ~62 Crore as on FY17 needs to be understood. Main Contributor: Anirudha Jain (@Inviquest) If you like the article share it with your colleagues.