Download

1 / 9

0 likes | 23 Views

Unlocking Financial Flexibility: Equity Line of Credit delves into the versatile world of HELOCs. Discover how this financial tool empowers homeowners to access home equity for various needs, from home renovations to debt consolidation. Explore the benefits, risks, and responsible usage, all aimed at helping you make informed financial decisions. Join us on this journey to unleash the potential of your home's equity for a more secure financial future. Visit us!

E N D

EQUITY LINE OF CREDIT IMAGINE LIVING www.imagineliving.ca

CONCEPT OF AN EQUITY LINE OF CREDIT A Home Equity Line of Credit (HELOC) is a flexible financial tool that allows homeowners to access funds based on the equity they've built in their homes. It functions like a revolving credit line, where borrowers can withdraw and repay money as needed, up to a predetermined credit limit. HELOCs typically have variable interest rates, and borrowers only pay interest on the amount they use. They are commonly used for home renovations, debt consolidation, education expenses, or other financial needs. HELOCs provide financial flexibility, enabling homeowners to tap into their home's value without selling it.

HOW DOES A HOME EQUITY LINE OF CREDIT WORK? A Home Equity Line of Credit (HELOC) operates as a revolving line of credit, allowing homeowners to borrow against their home equity. The process begins with applying and being approved based on factors like credit score and available home equity. Once approved, borrowers can access funds during a designated draw period, usually several years. They can withdraw as much or as little as they need, up to the approved credit limit. Interest is only accrued on the amount borrowed, and borrowers can make interest-only payments during the draw period. After the draw period ends, a repayment period begins, during which both principal and interest payments are required.

THE BENEFITS OF A HOME EQUITY LINE OF CREDIT • Flexible Access to Funds: Home equity line of credit provides a revolving line of credit, allowing homeowners to access funds as needed, up to a predetermined credit limit. • Lower Interest Rates: Home equity line of credit typically offer lower interest rates compared to credit cards and personal loans. This can result in significant interest savings over time, making it a cost-effective borrowing option. • Tax Deductibility: In some cases, the interest paid on a home equity line of credit may be tax-deductible, especially if the funds are used for home improvements or other eligible purposes. Consult with a tax advisor for specific guidance. • Financial Flexibility: Borrowers can choose how to use the funds, whether for home renovations, debt consolidation, education expenses, or other financial goals. This versatility allows homeowners to tailor the HELOC to their unique needs.

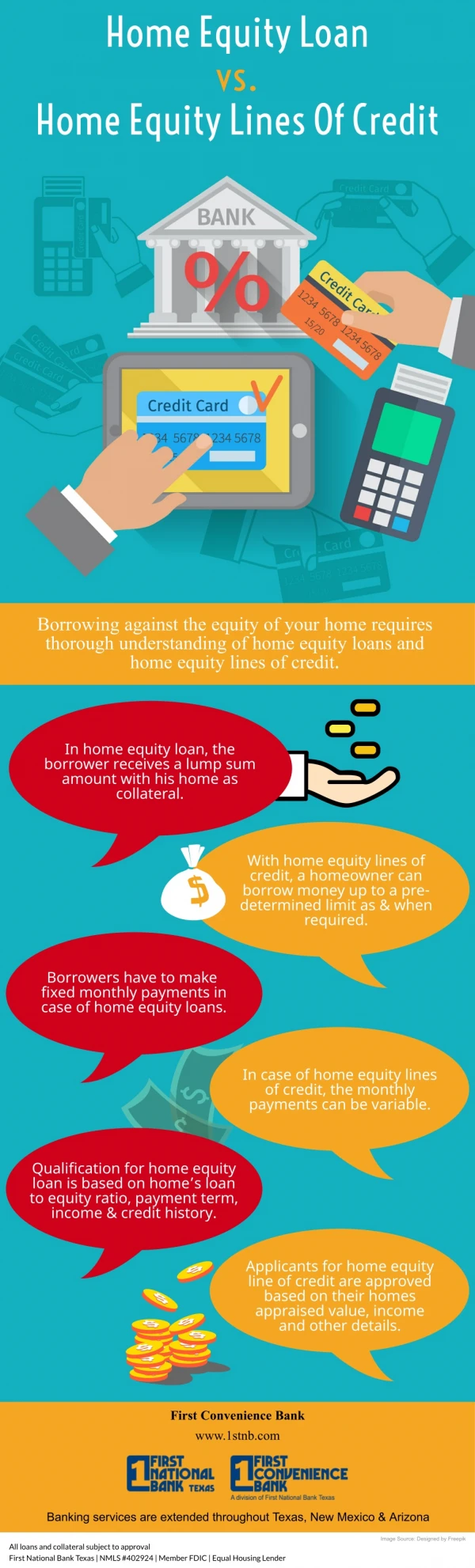

HOME EQUITY LINE OF CREDIT HOME EQUITY LOAN Home Equity Loan Provides a one-time lump sum, and borrowers cannot access more funds once the loan is disbursed. Usually comes with a fixed interest rate, providing predictable monthly payments. Requires regular monthly payments of both principal and interest from the beginning. Typically used for specific one-time expenses, like a major home improvement project or debt consolidation. HELOC is a revolving line of credit, similar to a credit card. Borrowers have a credit limit and can withdraw and repay funds as needed during the draw period. HELOC Offers flexible access to funds, allowing homeowners to borrow as little or as much as they need up to the credit limit. HELOC Typically has a variable interest rate tied to a benchmark rate (e.g., Prime Rate), which can change over time.

THE INTEREST RATES AND TERMS OF HOME EQUITY LINE OF CREDIT INTEREST RATES: • Variable Interest Rates: Most HELOCs feature variable interest rates. These rates are typically tied to a benchmark rate, such as the prime rate, and can fluctuate over time. • Introductory Rates: Some HELOCs offer introductory or promotional interest rates, often lower than the standard variable rate. These rates are typically in effect for a specified period before transitioning to the regular variable rate. • Fixed-Rate Options: In some cases, lenders may offer a fixed-rate option for a portion of the HELOC balance. This allows borrowers to lock in a fixed interest rate on a portion of their debt while keeping the rest at a variable rate.

TERMS: • Draw Period: The draw period is the initial phase of the Home equity line of credit during which borrowers can access funds as needed, up to the approved credit limit. This period typically lasts 5-10 years, during which borrowers make interest-only payments on the outstanding balance. • Repayment Period: After the draw period ends, the Home equity line of credit enters the repayment period, which can last 10-20 years. During this phase, borrowers can no longer access additional funds • Credit Limit: The credit limit is the maximum amount a borrower can access through the HELOC. It is determined based on factors like the home's appraised value, the amount of existing mortgage debt, and the lender's policies. • Loan-to-Value (LTV) Ratio: Lenders often set maximum LTV ratios for Home equity line of credits. This ratio compares the total debt secured by the home to the home's appraised value.

CONTACT US! 604-603-9060 www.imagineliving.ca info@imagineliving.ca 2569 Hyannis Point, North Vancouver, V7H 1R9

THANK YOU! www.imagineliving.ca

![[Ebook] Unlocking Equity and Trusts (Unlocking the Law)](https://cdn7.slideserve.com/12461186/slide1-dt.jpg)