Download

1 / 50

510 likes | 684 Views

Chapter 5 MONEY AND INFLATION Dr. Mohammed Alwosabi. DEFINITION OF INFLATION Inflation is a process of continuous (persistent) increase in the price level. Inflation results in a decrease of the value of money. In the definition of inflation we have to observe that:

E N D

Chapter 5 MONEY AND INFLATION Dr. Mohammed Alwosabi

DEFINITION OF INFLATION • Inflation is a process of continuous (persistent) increase in the price level. Inflation results in a decrease of the value of money. • In the definition of inflation we have to observe that: • Inflation is an increase in the prices of all goods and services not only of a particular good or service. An increase in the price of one good is not inflation. • Inflation is an ongoing process, not a one-time jump in the price level.

Milton Friedman proposed that "inflation is always and everywhere a monetary phenomenon". • The source of inflation is the high growth rate of money supply with “too much money chasing too few goods”. • A quick and simple solution to fighting inflation is reducing the growth rate of the money supply. • The proposition that inflation is the result of a high rate of money growth is supported by evidence from inflationary episodes throughout the world.

The German hyperinflation of the 1921-23 supports the proposition that excessive monetary growth causes inflation and not the other way around since the increase in monetary growth appears to have been exogenous, the government expands the money supply to finance its expenditures. • Evidence for Latin American countries over the ten-year period 1989-1999 indicates that in every case in which a country's inflation rate is extremely high for any sustained period of time, its rate of money growth is extremely high

INFLATION RATE: • To measure the inflation rate, we calculate the annual percentage change in the price level. • we measure the price level (P) of a country using GDP Deflator or CPI.

These two equations show the connection between the inflation rate and the price level. If the price level in the current year is higher than that of the last year, the inflation rate will be positive meaning higher inflation rate the lower is the value of money.

VIEWS OF INFLATION • According to aggregate demand and supply analysis, inflation is caused by expansionary monetary policies. • A continually increasing money supply causes a continual increase in aggregate demand, everything else held constant. • Fiscal policy alone cannot produce inflation. There is a limit on the total amount of possible government expenditure. Decreasing taxes also has a limit.

Negative supply shocks increase the price level, but cannot increase the inflation rate. • Suppose that the economy is at the natural rate of output. In the absence of accommodating policy and everything else held constant, the net result of a negative supply shock is that the economy returns to full employment at the initial price level.

SOURCES OF INFLATION • Inflation usually occurs as a result of expansionary monetary policy. (1) Cost-Push Inflation and High Employment Targets • Cost-push inflation arises due to a decrease in supply as a result of the rise in the per-unit cost of production. • The negative supply shocks mainly occur because of the push by workers to get higher wages, the increase in the prices of other factors of production, or the increase in the prices of raw materials (e.g. oil price)

At a given price level, cost-push inflation starts as the rise in the cost of production, because of an increase in the money wage rate or an increase in the prices of raw material firms are willing to produce less amount of the output SAS decreases SAS shifts leftward an increase in prices and unemployment and a decrease in RGDP stagflation

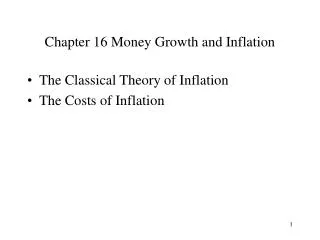

LAS P SAS3 SAS2 P4 E SAS1 P3 D P2 C AD3 P1 B A P0 AD2 AD1 Y Y1 Y0

Suppose that the last year price level was P0 and PGDP is Y0, where AD0, SAS0 and LAS intersect at point A, the LR FE equilibrium. • If, in the current year, nominal wages or prices of other factors of production increase production cost increases firms reduce production SAS SAS curve shifts leftward to SAS1 to point B. • At point B, price level increases to P1 and RGDP decreases to Y1 and therefore unemployment increases above its natural rate (below FE) • If government fiscal and monetary policies remain unchanged, the economy would move back to point A

However, as a response to the increase in P and unemployment, and a decrease in RGDP, the government increases Qm, G or decreases T AD increases AD curve starts to shift rightward until it reaches AD1 at point C, where AD1 intersects with SAS1 and LAS. • At point C, the economy is at higher price level (P2) and RGDP goes back to PGDP (Y0) at full employment • With the new higher price, money wage rate and prices of other productive resources start to increase again which leads to increase in the cost of production SAS curve will shift leftward from SAS1 to SAS2 stagflation the process will be repeated higher price level (inflation) • This is an ongoing process of rising price level.

Note that a one-time increase in the price of one resource without any following change in AD produces stagflation but not inflation. • The combination of a successful wage push by workers and the government's commitment to high employment leads to cost-push inflation. • Cost-push inflation is a monetary phenomenon because it cannot occur without the monetary authorities pursuing an accommodating policy of a higher rate of money growth.

Accommodating policy (usually monetary policy) occurs when government pursue active, discretionary policy to eliminate high unemployment that developed after a successful wage push by workers. • Monetary expansion increases AD repeatedly, and wages continue to adjust upward. This recipe leads to inflation • In the absence of an accommodating monetary policy and everything else held constant, a push by workers to get higher wages will cause higher unemployment and higher prices, and the net result of a negative supply shock is that the economy returns to full employment at the initial price level.

(2) Demand-Pull Inflation • Demand-pull inflation occurs when policy makers pursue policies that raise AD and shift the aggregate demand curve to the right • Demand-pull inflation is a result of the increase in spending faster than the increase in production of output. • An increase in aggregate demand is caused mainly by the increase in Money supply (quantity of money (Qm)), or the increase in any of C, I, G, or X

Suppose the economy is at LR full employment equilibrium point A, where LAS, AD0 and SAS0 intersect with each other. At this point, RGDP = PGDP = Y0 and P = P0. • Then, because government goal is to achieve high level of employment (high level of output), government may increase Qm, or G, or decrease T, which leads to an increase in AD AD curve shifts rightward from AD0 to AD1 the new SR equilibrium is at point B,

At B, RGDP is greater than PGDP, price level increases from P0 to P1, real wage rate has decreased and unemployment falls below its natural rate (above FE) there is a shortage of labor money wage rate starts to increase to attract more labor SAS starts to decrease SAS curve starts to shift leftward P starts to increase and RGDP starts to decrease until SAS curve shifted to SAS1 where it intersects AD1 and LAS at point C

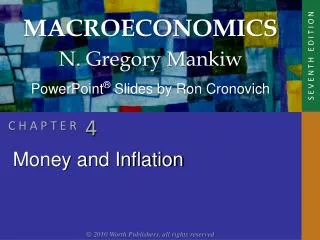

P LAS SAS3 SAS2 P4 E D P3 SAS1 P2 C AD3 P1 B P0 A AD2 AD1 Y Y0 Y1

At point C, RGDP goes back to its potential LR and FE level (Y0) and the price level increase further to P2. • This process is only a one-time rise in P. For inflation to proceed, AD must persistently increase. • At this stage two actions may occur simultaneously: (1) Government wants to achieve a specific target of high employment (and high production) so it will increase G, Qm or decrease taxes, and (2) Since now the money wage is higher which means people can spend more and as a result P is higher (P2), the result is the increase in Qm • In either case increase in AD AD curve will shift from AD1 to AD2 the process will continue higher price level (inflation) • This is an ongoing process of rising price level.

From the discussion above, according to aggregate demand and supply analysis, it is evidenced that high inflation cannot be driven by fiscal policy alone. High money growth produces high inflation. Inflation is caused by expansionary monetary policies. • Theoretically, one can distinguish a demand-pull inflation from a cost-push inflation by comparing the unemployment rate with its natural rate level.

(3) Budget Deficit and Inflation • High government budget deficit relative to GDP can be a source of sustained inflation only if • it is persistent rather than temporary, and • if the government finances it by creating money rather than by issuing bonds to the public

ACTIVIST / NONACTIVIST POLICY DEBATE • Activist is an economist who views the self-correcting mechanism through wage and price adjustment to be very slow and hence sees the need for the government to pursue active, discretionary policy to eliminate high unemployment whenever it develops. • Activists argue that monetary and fiscal policies should be deliberately used to smooth out the business cycle. • They are in favor of economic fine-tuning, which is the frequent use of monetary and fiscal policies to counteract even small undesirable movements in economic activity.

According to activists, the economy does not always equilibrate quickly enough at natural real GDP. • They believe that activist monetary policy works; it is effective at smoothing out the business cycle.

Nonactivist is an economist who believes that the performance of the economy would be improved if the government avoided active policy to eliminate unemployment • Nonactivists argue against the use of deliberate fiscal and monetary policies. • They believe the discretionary policies should be replaced by a stable and permanent monetary and fiscal framework and the rules should be established in place of activist policies. • According to nonactivists, in modern economies, wages and prices are sufficiently flexible to allow the economy to equilibrate at reasonable speed at natural real GDP.

They believe activist monetary policies may not work, and may be more destabilizing rather than stabilizing, and are likely to make matters worse rather than better.

If aggregate output is below the natural rate level, advocates of activist policy would recommend that the government try to eliminate the high unemployment by attempting to shift the aggregate demand curve to the right while advocates of nonactivist policy would recommend that the government to do nothing. • Activists usually view fiscal policy as having a shorter effectiveness lag than monetary policy, but there is substantial uncertainty about how long this lag is. • According to activist, the wage and price adjustment process being extremely slow, and a nonactivist policy results in a large loss of output

Nonactivists usually view fiscal policy as having a longer implementation lag than monetary policy, but there is substantial uncertainty about how long this lag is • Nonactivists contend that an activist policy of shifting the aggregate demand curve will be costly because it produces more volatility in both the price level and output • There are five time lags that prevent an activist policy from returning aggregate output to full employment instantaneously

The data lag is the time it takes for policymakers to obtain the data that tell them what is happening to the economy, • The recognition lag is the time it takes for policymakers to be sure of what the data are signaling about the future course of the economy. • The legislative lag represents the time it takes to pass legislation to implement a particular (fiscal) policy • The implementation lag is the time it takes for policymakers to change policy instruments once they have decided on a new policy. • The effectiveness lag is the time that it takes for an activist policy to actually influence economic activity.

The existence of lags prevents the instantaneous adjustment of the economy to policies changing aggregate demand, thereby strengthening the case for nonactivist policy. • However, activist respond that even with time lags, activist policy moves the economy to full employment before the economy's self-correcting mechanism would

EFFECTS OF INFLATION • Inflation may be anticipated (expected) or unanticipated (unexpected) • A moderate anticipated (expected) has a small cost, but a rapid anticipated inflation is costly because it decreases potential GDP and slow growth. • Unanticipated (unexpected) inflation has two main consequences in the labor market. It redistributes income and results in the departure from full employment

Higher than anticipated inflation (unexpectedly high) lowers the real wage rate employers gain at the expense of workers increases the quantity of labor demanded, makes jobs easier to find, and lowers the unemployment rate. • Lower than anticipated inflation (unexpectedly low) raises the real wage rate workers gain at the expense of employers decreases the quantity of labor demanded, and increases the unemployment rate. • If workers and employers base their wages on an inflation forecast that turns out to be correct, neither workers nor employers gain or lose from the inflation.

Unanticipated inflation has two main consequences in the market for financial capital: it redistributes income and results in too much or too little lending and borrowing. • When the inflation rate is higher than anticipated (unexpectedly high) the real interest rate is lower than anticipated borrowers gain but lenders lose borrowers want to have borrowed more and lenders want to have loaned less. • When the inflation rate is lower than anticipated (unexpectedly low) the real interest rate is higher than anticipated lenders gain but borrowers lose borrowers want to have borrowed less and lenders want to have loaned more

We can conclude from the above that Inflation that is higher than expected, transfers resources from workers to employers and from lenders to borrowers. • The opposite is true

High levels of unanticipated inflation have other negative impacts on economies for a number of reasons. • They lead to distortions in the economy and give confusing price signals to producers. • For individuals on fixed incomes, the rise in prices increases the cost of living, eroding purchasing power. • For investors it erodes the value of saving, while effectively reducing the real rate of borrowing for debtors. • It makes goods produced in the country more expensive relative to goods produced abroad resulting in a decrease in exports and an increase in imports.

People who hold a lot of money loose from inflation because money value becomes less overtime. • Those who own “real” assets such as land, stocks, etc. gain from inflation because the value of these assets goes up with inflation.

SNAPSHOT ON THE CURRENT INFLATION IN GCC COUNTRIES (2007- 08) • The growth rate of money supply in Gulf countries has in some cases exceeded 20 percent. Check the latest rates of inflation in GCC countries. • With this double digit inflation nominal interest rates are way below the inflation rate which has resulted in negative real rates of interests.

Factors Causing Inflation in GCC Stats • As a result of pegging GCC currencies - except the Kuwaiti dinar- to a weakening dollar there has been an increase in the cost of goods that are imported from countries whose currencies had appreciated against the dollar, like the EU, Japan and China. • Rising food prices internationally due to the high demand for some types of grains such as corn to use them as bio fuels in addition to the increase in the price of oil, this added to the increase in the food prices.

Huge money supply and abundant liquidity, triggered by sharply higher oil revenues, that is accompanied by a fixed supply of goods and services. • The rise in demand for real estate, which increases real estate prices in addition to sharp increase in the cost of housing due to shortage in property supplies such as steel and cement. • The dollar peg forces GCC central banks to follow the US Federal Reserve in setting interest rates. But while the US central bank continues cutting rates to stimulate a sluggish economy, GCC central banks are faced with expanding economies that were already overheating at the higher rates. Cutting interest rate just fuel the inflation more. • The increase in wages without controlling goods markets that just increase prices to take advantage of the wage rise

Solutions adopted by GCC • It is not necessary to adopt all solutions by all countries. Different countries adopted different solutions • De-peg GCC Currencies from the tumbling dollar and track a currency basket of their main trade partners, including the US dollar, euro, sterling and yen. The European Union is now the main trading partner of the GCC accounting for 35 per cent of their foreign trade, followed by Asian countries 30 per cent and the US 10 per cent. • As a recommended basket, GCC states may link their currencies with the International Monetary Fund's Special Drawing Rights (SDRs), a mixed basket of currencies.

Revaluation: the link to the dollar should be revisited without necessarily de-pegging the Gulf currencies, • Price should be controlled by governments, especially of the necessary products. • Increase in interest rates should be implemented to reduce money supply and liquidity in the hands of public. • Increase the reserve requirement for banks forcing lenders to keep more customer deposits in their vaults. • Central banks should engage in open market operations to decrease the abundant liquidity. • Create a suitable environment to invest the liquidity surplus in import substitution products.

The Current Global Financial Crises • The current financial crisis hits the world in many ways and has its impact on most countries around the world. • There have been many debates, discussions, articles, meetings, interviews, lectures, legislations, and summits that create a huge amount of literature on this crisis. • It is the assignment of every one of you to write an at least a 5-page (with 12 Times New Roman and 1.5 space)essay about this crisis stating the following:

The causes of the crisis • The different impacts of the crisis on countries, consumers’ welfare, and business strength • The impact of the crisis on Bahrain and other GCC countries • The actions that have been taken to reduce the impact of the crisis • The solutions to go out of this crisis