Download

1 / 145

1.45k likes | 1.56k Views

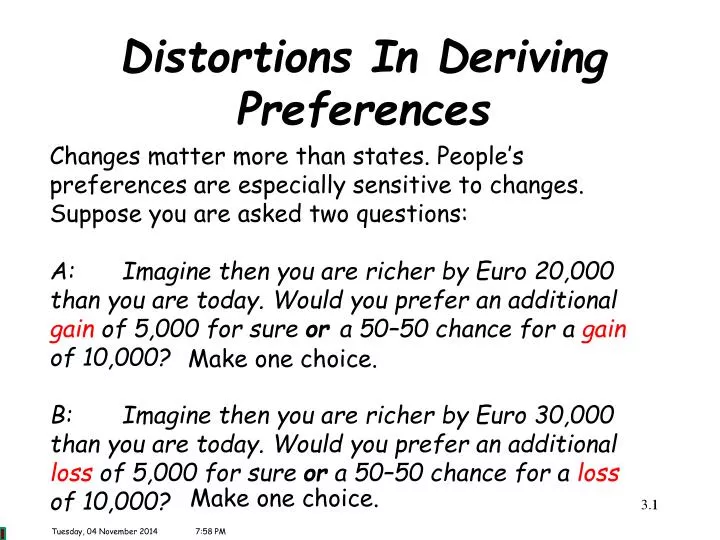

Changes matter more than states. People’s preferences are especially sensitive to changes. Suppose you are asked two questions: A: Imagine then you are richer by Euro 20,000 than you are today. Would you prefer an additional gain of 5,000 for sure or a 50–50 chance for a gain of 10,000?

E N D

Changes matter more than states. People’s preferences are especially sensitive to changes. Suppose you are asked two questions: A: Imagine then you are richer by Euro 20,000 than you are today. Would you prefer an additional gain of 5,000 for sure or a 50–50 chance for a gain of 10,000? B: Imagine then you are richer by Euro 30,000 than you are today. Would you prefer an additional loss of 5,000 for sure or a 50–50 chance for a loss of 10,000? Distortions In Deriving Preferences Make one choice. Make one choice. 1 Tuesday, 04 November 20147:58 PM

Although the final outcomes in the two problems are exactly the same, most people choose the gamble in Question A and the sure loss in Question B. Apparently, they tend to favour the narrow framing based on gains and losses rather than the broader (and more relevant) framing based on the final wealth. Distortions In Deriving Preferences 2

People’s sensitivity to losses is higher than their sensitivity to gains. Suppose you are asked the question: Consider a bet on the toss of the coin. If heads, you lose Euro 100. What is the minimum gain, if tails, that would make you accept the gamble? Most answers typically fall in the range from 200 to 250, which reflects a sharp asymmetry between the values that people attach to gains and loses. Distortions In Deriving Preferences - Loss Aversion Make a choice. 3

One ubiquitous pattern stands out: Losses resonate more than gains. In a wide variety of domains, people are more averse to losses than they are attracted to same-sized gains. One of the main realms where loss aversion plays out is in preferences over wealth levels. Distortions In Deriving Preferences - Loss Aversion 4

What distinguishes loss aversion from conventional risk aversion is that people are significantly “risk averse” for even small amounts of money. People dislike losing $10 more than they like gaining $11, and hence prefer their status quo to a 50/50 bet of losing $10 or gaining $11. Tversky and Kahneman (1991) suggest that in most domains where sizes of losses and gains can be measured, people value moderate losses roughly twice as much as equal-sized gains. Distortions In Deriving Preferences - Loss Aversion 5

Finally, in prospect theory (which is a key concept in behavioural economics), the pain associated with a possible loss is much greater than the pleasure associated with a gain of the same magnitude. In the strip, Dilbert's garbage man clearly understands this concept much better than Dilbert. Cartoon(Kramer 2014) Distortions In Deriving Preferences - Loss Aversion 6

Distortions In Deriving Preferences - Loss Aversion People fear losing more than they desire to win. This phenomenon, first demonstrated by Tversky and Kahneman (1991), is known as loss aversion, and it shows up everywhere. Kahneman (2011) describes how economists Pope and Schweitzer (2011) reasoned that golf provides a perfect example of a reference point: par. 3.7 7

Distortions In Deriving Preferences - Loss Aversion Every hole on the golf course has a number of strokes associated with it; the par number provides the baseline for good — but not outstanding — performance. For a professional golfer, a birdie (one stroke under par) is a gain, and a bogey (one stroke over par) is a loss. The economists compared two situations a player might face when near the hole: putt to avoid a bogey putt to achieve a birdie 3.8 8

Distortions In Deriving Preferences - Loss Aversion Every stroke counts in golf, and in professional golf every stroke counts a lot. According to prospect theory, however, some strokes count more than others. Failing to make par is a loss, but missing a birdie putt is a foregone gain, not a loss. Pope and Schweitzer reasoned from loss aversion that players would try a little harder when putting for par (to avoid a bogey) than when putting for a birdie. They analysed more than 2.5 million putts in exquisite detail to test that prediction. 3.9 9

Distortions In Deriving Preferences - Loss Aversion They were right. Whether the putt was easy or hard, at every distance from the hole, the players were more successful when putting for par than for a birdie. The difference in their rate of success when going for par (to avoid a bogey) or for a birdie was 3.6%. This difference is not trivial. Tiger Woods was one of the “participants” in their study. If in his best years Tiger Woods had managed to putt as well for birdies as he did for par, his average tournament score would have improved by one stroke and his earnings by almost $1 million per season. 3.10 10

Distortions In Deriving Preferences - Loss Aversion These fierce competitors certainly do not make a conscious decision to slack off on birdie putts, but their intense aversion to a bogey apparently contributes to extra concentration on the task at hand. The study of putts illustrates the power of a theoretical concept as an aid to thinking. Who would have thought it worthwhile to spend months analysing putts for par and birdie? The idea of loss aversion, which surprises no one except perhaps some economists, generated a precise and non-intuitive hypothesis and led researchers to a finding that surprised everyone — including professional golfers. “Golf is a good walk spoiled” Mark Twain (30 November 1835 Florida - Missouri) 3.11 11

Loss Aversion - Barings Bank How destructive is loss aversion? Perhaps the most familiar case of loss aversion or “get-evenitis,” occurred in 1995, when 28-year-old Nicholas Leeson caused the collapse of his famous employer, the 233-year-old Barings Bank. At the end of 1992, Leeson had lost about £2 million, which he hid in a secret account. By the end of 1993, his losses were about £23 million, and they mushroomed to £208 million at the end of 1994 (at the time, this was $512 million). Instead of admitting to these losses, Leeson gambled more of the bank’s money in an attempt to “double-up and catch-up.” Rogue Trader, Pub. Pathé, 1999 here also Rogue Trader: How I Brought Down Barings Bank and Shook the Financial World, Nick Leeson, Pub. Little, Brown & Company, 1996 here 3.12 12

Loss Aversion - Barings Bank On February 23, 1995, Leeson’s losses were about £827 million ($1.3 billion) and his trading irregularities were uncovered. Although he attempted to flee from prosecution, he was caught, arrested, tried, convicted, and imprisoned. Also, his wife divorced him (Jordan et al. 2012). For a review that focuses on banks rather than borrowers and associated risks see Beatty and Liao (2014). There is a very large literature on bank debt contracting, the literature is surveyed by Armstrong et al. (2010). 3.13 13

Women are found to be more risk averse in making financial decisions than men (Donkers and Van Soest, 1999; Powell and Ansic, 1997; Weber et al., 2002). Women also tend to own less risky assets than single men or married couples and reduce their risky assets when the number of children increases, in contrast to single men and married couples (Jianakoplos and Bernasek, 1998). Furthermore, older people tend to take less financial risks than younger people (Jianakoplos and Bernasek, 2006). Distortions In Deriving Preferences - Risk Aversion 14

On the other hand, it has been shown that it was possible to teach effective risk diversification (Hedesström et al., 2006). “In 4 experiments, undergraduates made hypothetical investment choices. … In order to counteract naive diversification, novice investors need to be better informed about the rationale underlying recommendations to diversify.” Distortions In Deriving Preferences - Risk Aversion 15

People’s financial history has a strong impact on their taste for risk. Malmendier and Nagel (2011) investigated whether individual experiences of macroeconomic shocks affect financial risk taking. As has often been suggested for the generation that experienced the Great Depression (1930s). Using data from the Survey of Consumer Finances from 1960 to 2007, they found that individuals who have experienced low stock market returns throughout their lives so far report lower willingness to take financial risk. They are less likely to participate in the stock market. Invest a lower fraction of their liquid assets in shares if they participate. They are more pessimistic about future share returns. Distortions In Deriving Preferences - Risk Aversion 16

Exposure to economic turmoil appears to dampen people’s appetite for risk irrespective of their personal financial losses. That is the conclusion of Knüpfer et al. (2013) who suggest that labour market experiences are a natural candidate for explaining portfolio heterogeneity. In the early 1990s a severe recession caused Finland’s GDP to sink by 10% and unemployment to soar from 3% to 16%. Using detailed data on tax, unemployment and military conscription, the authors were able to analyse the investment choices of those affected by Finland’s “Great Depression”. Distortions In Deriving Preferences - Risk Aversion 17

The results suggest that workers who have experienced more adverse labour market conditions are significantly less likely to invest in risky assets. The decrease in risky investment is robust to controls for parental variables, family fixed effects, and cognitive ability, and is not fully attributable to the impact labour market shocks have on future income, unemployment risk, and wealth accumulation. They found that those hit harder by unemployment were less likely to own stocks a decade later. Individuals’ personal misfortunes, could explain at most half of the variation in stock ownership. They attribute the remainder to “changes in beliefs and preferences” that are not easily measured. Distortions In Deriving Preferences - Risk Aversion 18

Financial trauma appears to dampen people’s appetite for risk. Guiso et al. (2013) examined the investments of several hundred clients of a large Italian bank in 2007 and again in 2009 (i.e. before and after the plunge in global stock markets). The authors also asked the clients about their attitudes towards risk and got them to play a game modelled on a television show in which they could either pocket a small but guaranteed prize or gamble on winning a bigger one. Distortions In Deriving Preferences - Risk Aversion 19

Risk aversion, by these measures, rose sharply after the crash, even among investors who had suffered no losses in the stock market. They found that both a qualitative and a quantitative measure of risk aversion increases substantially after the crisis. After considering standard explanations, they investigated whether this increase might be an emotional response (fear) triggered by a scary experience. The reaction to the financial crisis, the authors conclude, looked less like a proportionate response to the losses suffered and “more like old-fashioned ‘panic’.” To show the plausibility of this conjecture, they conducted a laboratory experiment. Distortions In Deriving Preferences - Risk Aversion 20

The authors’ conclusions were reinforced by a separate test administered to a few hundred university students. About half were asked to watch a five-minute excerpt of a gruesome torture scene from a horror film. Then, the entire group answered the same questions about risk as the Italian bank’s clients. Watching the horror movie increased the students’ aversion to risk by roughly as much as the financial crisis had chastened the bank’s clients, although not among those who claimed to like horror movies. They found that subjects who watched a horror movie have a certainty equivalent that is 27% lower than the ones who did not, supporting the fear-based explanation. Distortions In Deriving Preferences - Risk Aversion 21

Does the Caveman Within Tell You How to Invest? Changes in human biology across the seasons helps shape investment decisions - Psychology Today - 18 August 2014 - Lisa Kramer Is there a rational theory of human behaviour that helps explain both the “Sell in May, then go away” effect observed in risky stock markets and an opposing seasonal cycle observed in safe Treasury bond markets. The paper (Kamstra et al. 2014 KKLW) is a bit technical, but it can be summed up easily with reference to our caveman ancestors. The study finds that the historical patterns of stock and bond returns through the seasons implies not only seasonally changing investor risk aversion, but also seasonal changes in the way investors decide between consuming now versus saving for the future. Risk Aversion – Seasonality 22

Many people experience severe seasonal depression (seasonal affective disorder - SAD), during the dark seasons of autumn and winter. When people get depressed in the winter, they become more averse to financial risk. The implication is a much larger reward, on average, for investors who are willing to hold risky stock during the dark seasons. Once daylight returns, investors become much more tolerant of risk, and with droves of people heading back into stocks in the spring, the rate of return investors earn holding stocks reduces, on average, leading to lower rewards for holding risk in the spring and summer. Lo and behold, Wall Street has an adage for that: “Sell in May, and go away.” (KKLW) Risk Aversion – Seasonality 23

How does an examination of our ancestors help shed light on all of this? The likelihood of our ancestors surviving another year was almost certainly enhanced by certain traits, such as willingness to save in the spring and summer so one could consume from stores of food in the autumn and winter. If our ancestors had acted like the proverbial grasshopper during the spring and summer — wildly consuming instead of judiciously saving — the odds of surviving through the next autumn and winter were certainly worsened. Thus, saving instead of consuming during the spring and summer would be the preferred behaviour for folks aiming to maximize the odds of survival. Additionally, by adopting cautious, “risk averse” habits through the autumn and winter, hunkering down until the daylight rebounded, they would increase their odds of surviving through to the spring. (KKLW) Risk Aversion – Seasonality 24

What are the key elements? Be aware of the way the changing seasons can influence your mood and ultimately your behaviour. Be cautious about making important financial decisions during particularly emotional times. Recognise that what might look like a great investment idea in the summer might not feel so appropriate once the winter doldrums set in, so try to build a portfolio that can endure the seasons. Investors who “buy and hold” tend to do better on average than those who trade frequently in an attempt to outperform the market. Accordingly, consider holding investments you’ll be comfortable holding through thick and thin. Kamstra, M.J., Kramer, L.A., Levi, M.D. and Wang T. 2014 “Seasonally Varying Preferences: Theoretical Foundations for an Empirical Regularity” The Review of Asset Pricing Studies 4(1) 39-77. Risk Aversion – Seasonality 25

Daylight-Saving Time Changes, Anxiety, & Investing. Disruptions in your sleep can have an impact on your portfolio - Psychology Today - 30 October 2013 - Lisa Kramer During the first weekend of November, people will turn their clocks back an hour. The gain or loss of an hour on the clock typically translates immediately into the gain or loss of an hour of sleep. Psychologists refer to the fallout from such disruptions as “sleep desynchronosis”, with the symptoms of the changed sleep habits closely resembling jet lag. And the phenomenon can have significant consequences. For instance, psychologists have noticed that whenever we shift the clocks to or from daylight-saving time, car accident rates tend to rise, likely due to the cognitive changes that accompany disrupted sleep habits. Risk Aversion – Seasonality 26

Perhaps surprisingly, the phenomenon is observed whether people are gaining or losing an hour of sleep. Several large-scale disasters have been associated with lack of sleep or disrupted sleep due to shift work, including the Exxon Valdez oil spill, the space shuttle Challenger explosion, the Three Mile Island near-meltdown, and the Chernobyl nuclear accident. Adverse effects of daylight-saving time changes can also spill over into financial markets, seemingly through increased anxiety that accompanies altered sleep patterns. Risk Aversion – Seasonality 27

In the language of financial economists, an increase in anxiety translates into greater reluctance to bear financial risk (or greater risk aversion). If investors wake up on the Monday following the time change feeling more anxious (and more risk averse) than usual, they may be less willing to buy risky stock and could even consider selling the stocks they already own. With many investors simultaneously experiencing such a shift in their sentiment , the result is often a drop in stock markets on the Monday following the time change. Of course financial markets are impacted by many different factors (not least important of which is fundamental economic news), so naturally the stock market could go up or down following any given daylight-saving time change (Kamstra et al. 2000, Pinegar 2002 and Kamstra et al. 2002). Risk Aversion – Seasonality 28

The study considers stock market returns from four countries, some of which change the clocks on different dates. They found the market downturn associated with daylight-saving time changes amounted to a single-day loss of $31 billion in US markets, on average. Risk Aversion – Seasonality 29

The finding does not imply ordinary investors should do anything drastic in preparation for the time change. I am definitely not counselling anyone to time their purchase or sale of securities in accordance with the time change. In fact, experience tells us the best way to navigate through our emotions in the context of investing is to avoid making important decisions whenever feelings come in to play. Making investing decisions during emotional times often results in suffering dramatic financial consequences. Think of all the people who panicked during the recent financial crisis, selling just when their fears – and markets – were at their worst. Many of them ended up liquidating their assets at steeply discounted prices. Had they just sat tight and stuck to a buy and hold approach, they would eventually have noticed their stocks resuming their previous values. Risk Aversion – Seasonality 30

At the best of times, people can be forgiven for feeling a sense of anxiety when it comes to investing. Emotions can ride even higher than usual under some conditions, including times of sleep disruption such as those associated with daylight-saving time changes. By remaining calm and avoiding impulsive, emotion-driven investment decisions, there is no need to lose sleep over the market. Kamstra, M.J., Kramer, L.A. and Levi, M.D. 2000 “Losing sleep at the market: The daylight saving anomaly” American Economic Review 90(4) 1005-1011. Pinegar, J.M. 2002 “Losing sleep at the market: Comment” American Economic Review 92(4) 1251-1256. Kamstra, M.J., Kramer, L.A. and Levi, M.D. 2002 “Losing sleep at the market: The daylight saving anomaly: Reply” American Economic Review 92(4) 1257-1263. Risk Aversion – Seasonality 31

In new research (Thaiss et al. 2014), the microbes in the faeces of humans and mice were analysed, and it was discovered that gut microbes follow a rhythmic pattern throughout the day. The cycle depends on eating habits and the circadian cycle of the human or mouse. The microbes were disrupted when the mice were exposed to an abnormal eating schedule and changes in their exposure to light and dark, the study found. In two people who suffered from jet lag, certain types of bacteria became more common. The germs are linked to obesity and problems in the body's metabolic system, according to the researchers. Jet lag can cause obesity by disrupting the daily rhythms of gut microbes - ScienceDaily - 16/Oct/2014 Jet lag doesn’t just leave travellers feeling rotten – it is also being blamed for making them fatter - Telegraph - 16/Oct/2014 Or Is It A Gut Reaction? 32

Thaiss et al. “Transkingdom Control of Microbiota Diurnal Oscillations Promotes Metabolic Homeostasis”, Cell, 2014. Or Is It A Gut Reaction? 33

Risk Aversion – A Counter Previous studies of loss aversion in decisions under risk have led to mixed results. Losses appear to loom larger than gains in some settings, but not in others. The paper (Ert and Erev, 2013) highlighting six experimental manipulations that tend to increase the likelihood of the behaviour predicted by loss aversion. 3.34 34

These manipulations include: 1 framing of the safe alternative as the status quo; 2 ensuring that the choice pattern predicted by loss aversion maximizes the probability of positive (rather than zero or negative) outcomes; 3 the use of high nominal (numerical) payoffs; 4 the use of high stakes; 5 the inclusion of highly attractive risky prospects that creates a contrast effect; 6 the use of long experiments in which no feedback is provided and in which the computation of the expected values is difficult. Risk Aversion – A Counter 35

Their results suggest the possibility of learning in the absence of feedback: The tendency to select simple strategies, like “maximize the worst outcome” which implies “loss aversion”, increases when this behaviour is not costly. Theoretical and practical implications are discussed (Ert and Erev, 2013). Risk Aversion – A Counter 36

Loss aversion is related to the striking endowment effect identified by Thaler (1980, 1985). Once a person comes to possess a good, they immediately value it more than before they possessed it. How would you feel if you lost everything you owned, even if you were financially compensated? Like part of you had died? Or liberated? Examine the psychology of our lifelong relationship with objects (Jarrett, 2013). Distortions In Deriving Preferences - Endowment Effect 37

Kahneman et al. (1990) tested the endowment effect in a series of experiments, conducted in a classroom setting. In one of these experiments a decorated mug (retail value of about $5) was placed in front of one third of the seats after students had chosen their places. Distortions In Deriving Preferences - Endowment Effect 38

All participants received a questionnaire. The form given to the recipients of a mug (the “sellers”) indicated “You now own the object in your possession. You have the option of selling it if a price, which will be determined later, is acceptable to you. For each of the possible prices below indicate whether you wish to (x) Sell your object and receive this price; (y) Keep your object and take it home with you.” The subjects indicated their decision for prices ranging from $0.50 to $9.50 in steps of 50 cents. Distortions In Deriving Preferences - Endowment Effect 39

Some of the students who had not received a mug (the “choosers”) were given a similar questionnaire, informing them that they would have the option of receiving either a mug or a sum of money to be determined later. They indicated their preference between a mug and sums of money ranging from $0.50 to $9.50. The choosers and the sellers face precisely the same decision problem, but their reference states differ. Distortions In Deriving Preferences - Endowment Effect 40

The choosers face a positive choice between two options that dominate (their reference state). The sellers must choose between retaining the status quo (the mug) or giving up the mug in exchange for money. Thus, the mug is evaluated as a gain by the choosers, and as a loss by the sellers. Loss aversion entails that the rate of exchange of the mug against money will be different in the two cases. Distortions In Deriving Preferences - Endowment Effect 41

Indeed, the median value of the mug was $7.12 for the sellers and $3.12 for the choosers in one experiment, $7.00 and $3.50 in another. The difference between these values reflects an endowment effect, which is produced, apparently instantaneously, by giving an individual property rights over consumption goods. Distortions In Deriving Preferences - Endowment Effect 42

The behaviour described here is usefully conceptualised as a case of loss aversion comparable to that identified in choice among lotteries. Individuals who are randomly given mugs treat the mug as part of their reference levels or endowments, and consider not having a mug to be a loss, whereas individuals without mugs consider not having a mug as remaining at their reference point. Distortions In Deriving Preferences - Endowment Effect 43

As established by Knetsch and Sinden (1984), Samuelson and Zeckhauser (1988), and Knetsch (1989), a comparable phenomenon - the status quo bias - holds in multiple-goods choice problems. Here, loss aversion implies that an individual's willingness to trade one object for another depends on which object they begin with: Individuals tend to prefer the status quo to changes that involve losses in some dimensions, even when these losses are coupled with gains in other dimensions. Distortions In Deriving Preferences - Status Quo Bias 44

Knetsch and Sinden (1984) and Knetsch (1989), for instance, demonstrated the status quo bias by randomly giving one set of students candy bars, and the remaining students decorated mugs. Later, each student was offered the opportunity to exchange their gift for the other one - a mug for a candy bar or vice versa. 90% of both mug-owners and candy-owners chose not to trade. Distortions In Deriving Preferences - Status Quo Bias 45

Because the goods were allocated randomly and transaction costs were minimal, the different behaviour for the two groups of subjects must have reflected preferences that were induced by the allocation. Distortions In Deriving Preferences - Status Quo Bias 46

Other experiments have shown that the more choices you are given, the more pull the status quo has. More people will, for instance, choose the status quo when there are two alternatives to it rather than one: For example A and B instead of just A. Why? Choosing between A and B requires additional effort; selecting the status quo avoids that effort. In business, where sins of commission (doing something) tend to be punished much more severely than sins of omission (doing nothing), the status quo holds a particularly strong attraction. Distortions In Deriving Preferences - Status Quo Bias 47

Lipowski (1970) call this problem an approach-approach conflict: faced with enticing options, you find yourself unable to commit to any of them quickly. And even when you do choose, you remain anxious about the opportunities that you may have lost: maybe the “grass is greener”. He maintains that it is specifically the overabundance of attractive alternatives, aided and abetted by an affluent and increasingly complex society that leads to conflict, frustration, unrelieved appetitive tension, more approach tendencies and more conflict — a veritable vicious cycle. That cycle, in turn, likely has far-reaching and probably harmful effects on the mental and physical health of affected individuals. Distortions In Deriving Preferences - Choice 48

Iyengar and Lepper (2000) revived the idea of conflict created by an overabundance of choice — a concept called the paradox of choice (Schwartz 2004) and focusing on the concept of cognitive demands. When shoppers had to choose between jams or chocolates, it was found, they were more likely to make a selection when faced with six choices than when presented with twenty-four or thirty. They were also more satisfied with their ultimate selection. Too much choice would reduce motivation. That could be because an abundance of options may simultaneously attract and repel choice-maker, an emotion-based explanation. In a series of imaging studies Shenhav and Buckner (2014) observed students making various choices when inside an fMRI scanner. They found that given more “good” choices, makes you feel more anxious. Distortions In Deriving Preferences - Choice 49

A related study by the Office of Fair Trading (2008) examined the psychology of personal current bank account usage, with a focus upon account switching and bank charges. Each year, only a small fraction of people switch current accounts and the overall switching rate is low. Each year, a large proportion of people incur bank charges. Six psychological factors that may affect switching and charge-incurring behaviour were considered. Distortions In Deriving Preferences - Status Quo Bias 50