Download

1 / 64

640 likes | 762 Views

Lender Remedies After Default by Borrower. Lender’s basic choices are; (1) accept the proceeds of a sale to a third party in satisfaction of the mortgage (“short sale”); (2) accept a deed from the borrower in lieu of a foreclosure proceeding against the borrower (“deed in lieu”);

E N D

Lender Remedies After Default by Borrower • Lender’s basic choices are; (1) accept the proceeds of a sale to a third party in satisfaction of the mortgage (“short sale”); (2) accept a deed from the borrower in lieu of a foreclosure proceeding against the borrower (“deed in lieu”); (3) file a foreclosure action; or, (4) in some states, foreclose pursuant to state law that authorizes foreclosure by out-of-court sale. Donald J. Weidner

“Short Sales” • A “short sale” takes place when a lender accepts in satisfaction of a mortgage the net proceeds of a sale by the borrower to a third party, even though the proceeds are less than the amount due on the mortgage. • A lender is more likely to entertain a short sale if the property is worth less than the amount of the mortgage and a deficiency judgment against the borrower is either theoretically or practically improbable. Donald J. Weidner

“Short Sales” (cont’d) • Short sales permit lenders to avoid: • The delays incident to foreclosure. • The costs of foreclosure. • The carrying costs or management responsibilities incident to owning property upon consummation of foreclosure. • The resale costs of property acquired through foreclosure. • The appearance of too many “REO” properties (real estate owned as a result of foreclosure) on its books. Donald J. Weidner

Lender Remedies While Foreclosure Action is Pending • There are 3 remedies a lender might seek while a foreclosure action is pending: • 1. Physical possession of the mortgaged property. • 2. Assignment of rents from the mortgaged property. • 3. Appointment of a receiver to take charge of the mortgaged property. Donald J. Weidner

Lender Remedies After Default, Prior to Foreclosure (cont’d) • In the area of Lender remedies after default and prior to foreclosure, the theory of the mortgage has some, although limited, predictive value. Recall the three theories are: 1. Lien—A mortgage is only a lien, that is, a right to obtain title and possession by prosecuting a foreclosure action to completion. 2. Intermediate—A mortgage is initially only a lien, but title, and the right to possession, passes to the mortgagee when the mortgagor defaults 3. Title—A mortgage is a conveyance that passes title, and the right to possession, as soon as it is executed. Donald J. Weidner

Lender Remedy # 1: Physical Possession See Lifton article at text p. 870: • “Even in the title and intermediate states, modern courts are reluctant to grant a mortgagee physical possession of the property.” • Even if physical possession is possible, “restraints on the mortgagee and the risks of possession may dissuade lenders from seeking it.” Depending upon the jurisdiction a mortgagee in possession: • may have limited power over the property; • may not be compensated for its own management efforts and may not be able to recover money it spends to improve or to maintain the property; and • may risk having to account to the owner under stringent accounting rules for decisions on renting and operating the property if the owner later redeems. Donald J. Weidner

Lender Remedy # 2: Assignment of Rents Lifton article (cont’d): • Rather than seek physical possession, “the lender will usually look to the traditional remedies granting constructive possession. These are contained in standard mortgage provisions for • assignment of rents and for • appointment of a receiver in case of default.” • “Generally, an assignment of rents can be activated in title, intermediate and some lien states (such as Florida) by the mortgagee’s serving notice on the tenants . . . to pay their rents to the mortgagee.” • See the Florida assignment of rents Statute 697.07 • Most courts prefer to appoint an independent receiver. Donald J. Weidner

Florida Assignment of Rents Statute 697.07 • Purpose: to avoid the necessity of getting a receiver appointed to collect rents. • If a mortgage or separate instrument provides for an assignment of rents to secure repayment of an indebtedness, “the mortgagee shall hold a lien on the rents, and the lien created by the assignment shall be perfected and effective against third parties upon recordation of the mortgage or separate instrument with the public records of the county in which the real property is located . . . .” 690.07(1) and (2). • The assignment is enforceable “upon the mortgagor’s default and written demand for the rents made by the mortgagee . . . .” 690.07(3). • Therefore, on this issue, Florida is not the strictest of lien states Donald J. Weidner

Florida Assignment of Rents Statute 697.07 (cont’d) • Upon application by either the mortgagor or the mortgagee, in a foreclosure action, a court “may require the mortgagor to deposit the collected rents into the registry of the court, or in such other depository as the court may designate.” 697.07(4). • The court may authorize the use of the collected rents to pay “the reasonable expenses solely to protect, preserve, and operate the real property, including, without limitation, real estate taxes and insurance,” and to make payments to the mortgagee. 697.07(4)(a) and (c). • “The court shall expedite the hearing on the application by the mortgagee or mortgagor to enforce the assignment of rents.” 697.07(6). Donald J. Weidner

Lender Remedy # 3: Appointment of Receiver Lifton article (cont’d): • States vary in their approach to appointment of a receiver: • At one extreme, an agreement to appoint a receiver is usually sufficient to support an appointment. • In the middle, some states will appoint a receiver if there is proof: • that the security is impaired (courts differ on what constitutes impairment) and/or • that the borrower is insolvent. • At the other extreme, it is almost impossible to obtain a receiver. Donald J. Weidner

Lender Remedy # 3: Appointment of Receiver (cont’d) • Drawbacks of the Remedy of Appointment of a Receiver: • It can take a long time to get a receiver appointed. • The receiver may not be a good manager. • The receiver’s fees may eat up a good portion of the income. • Many lenders will simply choose to accept a deed in lieu of foreclosure. • Which can have risks. Donald J. Weidner

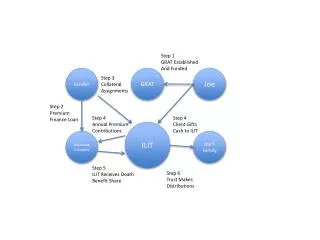

3 notes to finance 3 townhouse purchases CUNA Mortgage v. Aafedt (Text p. 875) 1985 Borrower Credit Union 3 Mortgages to secure notes HUD insured the Mortgages Credit Union Assign Ns & Ms CUNA Assignee Defaulted 1989 Borrower Commenced action to foreclose, stating it will not seek Deficiency .Judgment. CUNA Assignee CUNA Assignee Offers Deeds in Lieu of Foreclosure Rejects offer because CUNA’s mortgage insurer, HUD, said it would not reimburse CUNA if all CUNA could assign to HUD was a title acquired by a Deed in lieu of Foreclosure. CUNA filed foreclosure action Borrower Executed Quitclaim Deeds of 3 properties and records w/out CUNA’s knowledge Borrower Moved to dismiss foreclosure action because it executed the Deeds in lieu of foreclosure Borrower Donald J. Weidner

CUNA Mortgage v. Aafedt (cont’d) • CUNA said its ability to receive the mortgage insurance proceeds from HUD would be impaired if it accepted a deed in lieu rather than title through foreclosure. • Trial Court: • 1. Quitclaim deed was void [it was a unilateral act without CUNA’s consent, acquiescence, and hence there was no delivery]; and • 2. CUNA was entitled to bring the foreclosure proceeding. Donald J. Weidner

CUNA Mortgage v. Aafedt (cont’d) • Normally, recording a deed creates a rebuttable presumption of its delivery to, and its acceptance by, the grantee. • However, the presumption of acceptance arises only if the deed is beneficial to the grantee, not when the deed places a burden on the grantee. • Here, CUNA’s refusal to accept a deed in lieu was not in bad faith. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure Lenders are wary of “deeds in lieu” for a variety of reasons: 1. If bankruptcy is filed against the debtor within 90 days of the conveyance, a deed in lieu may be set aside as a preference. • Many title companies won’t insure on a deed in lieu until the 90-day preference period has passed. 2. Another possibility, though less likely, is that, if bankruptcy is filed within a year of the conveyance, it may be deemed a fraudulent transfer. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) 3. A voluntary conveyance from the owner does not cut off junior mortgagees or mechanics lien claimants. • Therefore, a foreclosure action may still be necessary to wipe out those liens. • Also: a junior lienor may argue, under the merger doctrine, that it is now the senior lien. • In short, if intervening liens are discovered, “the only prudent alternative for the mortgagee is to foreclose.” • In some states, the tax on voluntary transfers may be very high—based on the total value of the property (unreduced by the mortgage). Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) • There is a difference between theory and practice as state courts consider deeds in lieu. • In theory: • The rule against contemporaneous clogs on the equity of redemption does not apply to transactions subsequent to the original mortgage • Most courts permit the mortgagee to purchase the mortgagor’s equity of redemption. Donald J. Weidner

Lender Wariness of Deeds in Lieu of Foreclosure (cont’d) • However, in practice, courts examine a deed in lieu to assure it is: 1. Free from fraud. 2. Based on an adequate consideration; and 3. Is truly subsequent to the mortgage and not contemporaneous with it (not put in escrow when the mortgage was first executed). Donald J. Weidner

Lender Wariness of Deeds in Lieu (cont’d) 5. Theory versus practice and deeds in lieu (cont’d) • Courts are concerned with the disparity in bargaining strength between a lender and a borrower in default. • There are two situations in which the courts are more likely to be especially solicitous of the borrower: 1. If the transaction might be construed “as unfair and unconscionable,” • “especially if the consideration paid is disproportionately less than the value of the equity or if none is paid where the equity has value.” 2. Nonrecourse Debt. If “the deed is not by the mortgagor, but by a non-assuming grantee of the mortgagor, a release of the debt, since there was no personal liability, would be no consideration for the conveyance . . . and subject it to being set aside.” Donald J. Weidner

Lender Wariness of Deeds in Lieu (cont’d) 5. Theory versus Practice (cont’d) • “[T]here is always the possibility that a court will construe the [deed in lieu] as simply another mortgage transaction.” • “If the mortgagor is successful, he will be treated as a mortgagor under two mortgages—under the original mortgage which was not eliminated by the deed in lieu and under the deed in lieu treated as a second mortgage.” • “[T]he possibility [also] exists that because of insolvency of the mortgagor or an actual intent on his part to defraud creditors the conveyance may be subject to avoidance at the suit of creditors outside of bankruptcy.” Donald J. Weidner

Growth of Securitization of Real Estate Debt • In 1934, Congress created the Federal Housing Administration (FHA) to induce thrift institutions to originate long-term loans with relatively low down payments by insuring those lenders against the risk of default. • In 1938, the Federal National Mortgage Association (Fannie Mae) was created to buy and to sell federally insured mortgages. • In 1968, the Government National Mortgage Association (Ginnie Mae) was created as a second, secondary market agency to take over the low-income housing programs previously run by Fannie Mae. Donald J. Weidner

Growth of Debt Securitization in Real Estate (cont’d) • Fannie Mae “was then restructured as a private corporation with ties to the federal government” • And “given the authority to buy and sell conventional (non-federally insured) home mortgage loans.” • In 1970, Congress established the third major secondary mortgage market agency, the Federal Home Loan Mortgage Corporation (Freddie Mac), • which is also empowered to buy and to sell conventional mortgages. Donald J. Weidner

Growth of Debt Securitization in Real Estate • “In the 1970s, the secondary market agencies became critical in promoting the growth of securitization.” • “Issuers of mortgage-backed securities pool hundreds of loans together, obtain credit enhancement, usually in the form of guarantees, from a secondary market agency, and sell their interests in a pool of mortgages to investors.” 1. “The first generation of mortgage-backed securities were pass-through certificates that entitled the holders to a proportionate share of interest and principal as these amounts were paid by mortgagors.” 2. Issuers of mortgage-backed securities “subsequently divided the flow of mortgage interest and principal from the pool to create debt instruments of varying maturities and levels of risk.” • These different slices are known as “tranches” Donald J. Weidner

Federal Reserve Policy • When the Federal Funds Rate was only 1%, Federal Reserve Chairman Alan Greenspan announced that the FOMC would maintain an “highly accommodative stance” for as long as needed to promote “satisfactory economic performance” • Thus, there was cheap money to help drive up prices • Treasury obligations were not paying investors very much • Investors turned to mortgaged-backed securities for higher yields than Treasury bills at, they thought, relatively little risk • At the same time, Chairman Greenspan believed that the discipline of the markets, rather than regulation, would prevent excessive risk taking. Donald J. Weidner

“Crisis Looms in Market for Mortgages”(Supplement p. 1) Gretchen Morgenson, “Crisis Looms in Market for Mortgages,” New York Times, March 11, 2007. • As of March, 2007, the nation’s $6.5 trillion mortgage securities market was even larger than the United States treasury market. • “Already [March 2007], more than two dozen mortgage lenders have failed or closed their doors, and shares of big companies in the mortgage industry have declined significantly. Delinquencies on loans made to less creditworthy borrowers—known as subprime mortgages — recently reached 12.6 percent.” • 35% of all mortgage securities issued in 2006 were in the subprime category. Donald J. Weidner

Crisis Looms in Mortgage Market (cont’d) • Subprime Lenders created “affordability products,” mortgages that • Require little or no down payment • Require little or no documentation of a borrower’s income • Extend terms to 40 or 50 years • Begin with low “teaser” rates that rise later in the life of the loan. • Mortgages that require little or no documentation were known as “liar loans.” Donald J. Weidner

Crisis in Mortgage Market (cont’d) • “Securities backed by home mortgages have been traded since the 1970s, but it has been only since 2002 or so that investors, including pension funds, insurance companies, hedge funds and other institutions, have shown such an appetite for them.” • Wall Street was happy to help refashion mortgages into ubiquitous and frequently traded securities, and now dominates the market. By 2006 Wall Street had 60 percent of the mortgage financing market. Donald J. Weidner

Crisis in Mortgage Market (cont’d) • The big firms “buy mortgages from issuers, put thousands of them into pools to spread out the risks and then divide them into slices, known as tranches, based on quality. Then they sell them.” • Some of the big firms even acquired companies that originate mortgages. • Investors demands for mortgage-backed securities was insatiable • The greater the demand, the less the investment banks insisted on quality loans. Donald J. Weidner

Banks Sue Originators on Repurchase Agreements(Supplement p. 8) Carrick Mollenkamp, James R. Hagerty, Randall Smith, “Banks Go on Subprime Offensive,” The Wall Street Journal, March 13, 2007 • “Although the specifics vary from deal to deal, repurchase agreements obligate the mortgage originator, under some circumstances, to buy back a troubled loan sold to a bank or investor. That obligation sometimes kicks in if the borrower fails to make payments on the loan within the first few months or if there was fraud involved in obtaining the original mortgage.” • Billions in mortgages are covered by repurchase agreements. • However, many originators say that they cannot afford to buy back the loans or they are seeking bankruptcy protection. • Many loans went to “straw borrowers,” people who obtain the loan for another home buyer. • In some cases, brokers wrote contracts through straw men Donald J. Weidner

Rating Agencies • Credit rating agencies are supposed to assess risk of investment securities—however, the agencies are paid by the issuer of the security. • The rating agencies gave the mortgaged-backed securities a AAA rating, which suggested they were as safe as Treasury Obligations. • The projections they made about loan performance assumed a low foreclosure rate • That data focused only on recent history and thus suggested a foreclosure rate of perhaps only 2% • It didn’t include the newer, more risky mortgages • Nor did it anticipate falling real estate prices Donald J. Weidner

The Rating Agencies(Supplement p. 11) • Floyd Norris, “Being Kept in the Dark on Wall Street.” The New York Times, November 2, 2007. • Securitization was extremely profitable for investment banks, and only they seemed to understand what was going on. • The products they sold (sometimes labeled CDOs [collateralized debt obligations]) “could be valued according to models, which made for nice, consistent profit reports” for the people who bought them. Donald J. Weidner

The Rating Agencies (cont’d) • “No one seemed to be bothered by the lack of public information on just what was in some of these products. If Moody’s, Standard & Poor’s or Fitch said a weird security deserved an AAA, that was enough.” • “And then they blew up.” • “Now we are learning that the investment banks did not know what was going on either, and they ended up with huge pools of securities whose values are, at best, uncertain.” Donald J. Weidner

The Rating Agencies (cont’d) • “Rating agency downgrades do not destroy markets for corporate bonds, simply because enough information is disseminated that other analysts can reach their own conclusions.” • “But the securitization markets collapsed when it became clear the rating agencies had been overly optimistic.” • Some suggest that information shared with rating agencies should be shared with the entire market. Donald J. Weidner

The Rating Agencies (cont’d) • The SEC is investigating the rating agencies to see if their ratings complied with their own published standards. • Neither one of two plausible scenarios, knaves or fools, is pretty: • “It is hard to know which conclusion would be worse. [1] If the agencies violated their own policies, they will be vilified for the conflicts of interest inherent in their being paid by the issuers of the securities. [2] If they did not, they will be derided as fools who could not see how risky the securities clearly were. (In hindsight, of course.)” Donald J. Weidner

The Rating Agencies (cont’d) • The collapse of securitization has made credit hard to obtain for many, “and a change in the Fed funds rate will not offset that.” • “[I]t has become very difficult to get a home mortgage without some kind of government-backed guarantee.” Donald J. Weidner

Collateralized Debt Obligations • A collateralized debt obligation is a pool of different tranches (or slices) of mortgages • Or a pool of mortgages mixed with other receivables, such as credit card receivables • Lower-rated tranches were called “toxic waste” • That is, they are so high-risk, they are “toxic” • But the tranches were being pooled to make them appear to be less risky • And made to appear even less risky with credit default swaps (insurance against defaults) Donald J. Weidner

The Housing Bubble • From 2000-2003, there was a speculative bubble in housing. • Prices kept going up, mortgage financing was available. • People were seeing residences as investments, and non-real estate professionals were buying multiple residences to “flip” • However, from 2000-2007, the median household income was flat. Donald J. Weidner

The Housing Bubble • Therefore, the more prices rose, the more unsustainable the rise of prices and the increased financing costs. • By late 2006, the average home cost nearly 4 times what the average family made • As opposed to an historic multiple of only 2 or 3 • People began to default on their mortgages soon after taking them out. • By late 2006, housing prices started going down. • As defaults started, more houses came on the market, prices went further down. Donald J. Weidner

The Housing Bubble • While prices were rising, people were taking out “Home Equity Lines of Credit” • They were borrowing to pay off their mortgage and other debts. • When the Investment Bankers saw the defaults start increasing, they stopped buying the risky loans • Credit became tight for homeowners • The mortgage companies that specialized in buying up and packaging these loans to investment banks started going out of business • They were highly leveraged Donald J. Weidner

Foreclosure Filings: 2008-2012(2012 figures projected) • 2008 – 2,350,000 • 2009 – 2,920,000 • 2010 - 3,500,000 • 2011 - 3,580,000 • 2012 – 2,100,000 Source: RealtyTrac, Federal Reserve, Equifax Donald J. Weidner

Securitisation, When it goes wrong . . . .(Supplement p. 13) • “Securitisation, When it goes wrong . . . ., The Economist (September 20, 2007) • “Securitisation” is “the process that transforms mortgages, credit-card receivables and other financial assets into marketable securities • Brought huge gains • Also brought costs that are only now becoming clear. • “Thanks largely to securitisation, global private-debt securities are now far bigger than stockmarkets.” Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) • Benefits of securitization: • “Global lenders use it to manage their balance sheets, since selling loans frees up capital for new businesses or for return to shareholders.” • Small regional banks no longer need to place all their bets on local housing markets—”they can offload credits to far-away investors such as insurers or hedge funds.” 3. Reduces borrowing costs for consumers and businesses. Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) 4. One “systemic” gain was said to be: “Subjecting bank loans to valuation by capital markets encourages the efficient use of capital.” --However, the capital markets were not making their own valuations (Allan Greenspan admits that the Fed got it wrong on this point). • Broadens the distribution of credit risk. However, there are three cracks in the new model: 1. A high level of complexity and confusion. 2. Fragmentation of responsibility warped incentives. 3. Regulations came to be gamed. Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) 1. Problem # 1: complexity: “financiers did not fully understand what they were trading.” • Schwarcz says some contracts “are so convoluted that it would be impractical for investors to try to understand them” • Skel and Partnoy concluded that CDOs “are being used to transform existing debt instruments that are accurately priced into new ones that are overvalued.” 2. Problem #2: “securitisation has warped financiers’ incentives.” • “Securitisations are generally structured as ‘true sales’: the seller wipes its hands of the risks.” • One middleman has been replaced with several. Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) In mortgage securitisation, the lender is supplanted by --the broker --the loan originator --the servicer (who collects payments) --the arranger --the rating agencies --the mortgage-bond insurers -- the investor By January of 2008, there was widespread concern over the stability of the bond insurers. Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) • “This creates what economists call a principal-agent problem.” • “The loan originator has little incentive to vet borrowers carefully because it knows the risk will soon be off its books.” • “The ultimate holder of the risk, the investor, has more reason to care but owns a complex product and is too far down the chain for monitoring to work.” • Most investors were sophisticated institutions too taken with alluring yields to push for tougher monitoring Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) 3. Problem #3: Regulations were gamed. • Only now are the politicians looking at the rating agencies. • “Regulatory dependence on ratings has grown across the board.” • Banks can reduce the amount of capital they are required to set aside if they hold highly-rated paper. • Some investors, such as money-market funds, are required to stick to AAA-rated securities. Donald J. Weidner

Securitisation, When it goes wrong . . . .(cont’d) Looking forward: • “Investors need to know who is holding what and how it should be valued.” • There will be calls for greater standardization of “structured products.” • Regulators will want to see the interests of rating agencies “aligned more closely with investors, and to ensure that they are quicker and more thorough in reviewing past ratings.” • “[Securities Rating Agency] is one of the few businesses where the appraiser is paid by the seller, not the buyer.” Donald J. Weidner

Fannie Mae and Freddie Mac: End of Illusions(Supp. P. 22) • Fannie Mae and Freddie Mac: End of Illusions, The Economist, July 19, 2008, p. 79. • Fannie and Freddie “were set up to provide liquidity for the housing market by buying mortgages from the banks. They repackaged these loans and used them as collateral for bonds called mortgage-backed securities; they guaranteed buyers of those securities against default.” Donald J. Weidner

Fannie Mae and Freddie Mac: End of Illusions(Cont’d) • The belief in the implicit government guarantee of the obligations of Fannie and Freddie: • Permitted them to borrow cheaply. • They engaged in a “carry trade”—they earned more on the mortgages they bought than they paid for the money they raised. • Allowed them to operate with tiny amounts of capital and they became extremely leveraged (“geared”): 65 to 1! • $5 trillion of debt and guarantees! • Their core portfolio had been fine, with an average Loan/Value ratio of 68% at the end of 2007: “in other words, they could survive a 30% fall in house prices.” Donald J. Weidner