Download

1 / 38

380 likes | 390 Views

MONETARY INSTITUTIONS AND MECHANISMS. BEJU DANIELA GEORGETA Assoc. prof. Ph.D Finance Department Office: 337 room E-mail: daniela.beju@econ.ubbcluj.ro danibeju@yahoo.com. Contents (I). Chapter I. Money , money supply and inflation/deflation 1.1. The evolution of money. Types of money

E N D

MONETARY INSTITUTIONS AND MECHANISMS BEJU DANIELA GEORGETA Assoc. prof. Ph.D Finance Department Office: 337 room E-mail: daniela.beju@econ.ubbcluj.ro danibeju@yahoo.com

Contents (I) • Chapter I. Money, money supply and inflation/deflation 1.1. The evolution of money. Types of money 1.2. Money: definition and functions 1.3. Money supply. Monetary aggregates 1.4. Payment instruments. Payment system 1.5. Money creation and money demand 1.6. Inflation and deflation. Purchasing power of money • Chapter II. Monetary system 2.1. The elements of monetary system 2.2. The evolution of monetary systems 2.3. The international monetary system 2.4. The European monetary system 2.5. The Romanian monetary system

Contents (II) • Chapter III. Credit and interest rate 3.1. The role and functions of credit 3.2. Types of credits 3.3. Interest rates 3.4. Credit instruments 3.5. Lending activity 3.6. Credit collateral • Chapter IV. Monetary financial institutions 4.1. Money market 4.2. Commercial banks 4.3. Other credit institutions 4.4. Banking performance and risks 4.5. Central bank 4.6. Monetary policies 4.7. Banking supervision

Course outline – Money and money supply • The evolution of money. Types of money • Money: definition and functions • Money supply. Monetary aggregates

Clarification of some fundamental concepts • Money: • currency (the circulating currencies with legal tender status) • deposits accounts • Currency: • one form of money • takes the form of coins and paper money (banknote). • Coin: • a piece of metal used as a form of money • in other languages the words “coin” and “currency” are synonymous. • Banknote: • a promissory note made by a bank, payable to the bearer on demand. • Legal tender(forced tender): • a payment that, by law, cannot be refused in settlement of a debt denominated in the same currency.

Evolution of money. Types of money (I) • Commodity money: • money whose value comes from a commodity out of which it is made. • the users of this money directly perceive its value. • Representative money: • token coins and other physical tokens, that can be reliably exchanged for a fixed quantity of gold and silver. • fixed relation to the commodity which backs it. • has face value greater than its intrinsic value. • Scriptural money (bank money) • money placed into a banking institution for safekeeping. • recording money units in a current account opened in a bank. • has replaced, first commodity, and then representative money. • credit money: • money issued by the practice of fractional reserve banking which allowed the banks to lend the borrower in excess of the reserve it carries at any time.

Evolution of money. Types of money (II) • Fiat money: • any money declared by governments to be legal tender; • it is not backed by reserves of another commodity; • its value derived from the relationship between supply and demand for moneyit risks becoming worthless due to inflation; • has no intrinsic value, so it is based solely on faith; • fiat is the Latin word for "it shall be“. • Fiat money rose to prominence when the issuing government suspends the convertibility of representative money into precious metal. • Most modern currencies are fiat currencies: • have no intrinsic value; have fiat values lower than the intrinsic value. • so they are fiduciary money. • The USA was the latest state that switched to the fiat money in 1971, when the USA ceased to allow the conversion of the dollar into gold.

The etymology of word “money” • The origin of “money” comes from the Latin word “Moneta”, an epithet of the Roman goddess Juno, (the Jupiter’s wife). • In or near her temple, the Romans placed the first Mint (3th century BC). • The name Moneta is derived from the Latin monēre, which mean "to warn or advise“: • Juno Moneta is cited as warning Rome of impending danger on multiple occasions. • Juno Moneta was responsible with protecting Roman’s financial stability. • According to Herodotus: • the Lydians were the first people to introduce the use of gold and silver coins: • these first stamped coins were minted around 650–600 BC. • Paper money (banknotes) were first used in China during the 7th century.

What is money? • One of the most important financial asset of the economy. • All financial asset are valued in terms of money. • Flows of funds between lenders and borrowers occur through the medium of money. • Money itself is true financial asset, because all forms of money in use today are claims against some institution, public or private: • checking accounts (scriptural money) – a debt of a bank; • currency (coins and banknotes) – debt obligations of the issuing bank (central bank). • Definitions: • Economists’ use of the word money differs from conventional usage. • There is no single, precise definition of money, even for economists: • Money is anything that is generally accepted in the payment for goods and services and for the repayment of debts. • Money is anything that serves as a medium of exchange, a store of value and a standard of value.

What is money? • When most people talk about money, they’re talking about currency: • to define money just as currency is much too narrow for economists. • The word money is frequently used synonymously with wealth: • wealth: total collection of pieces of property that serve to store value; • wealth includes not only money but also other assets such as bonds, common stock, art, land, furniture, cars, and houses. • People also use the word money to describe what economists call income: • Income is a flow of earnings per unit of time; • Money, by contrast, is a stock: it is a certain amount at a given point in time. • The money discussed in this course refers to anything that is generally accepted in the payment for goods and services or in the repayment of debts and is distinct from income and wealth.

Functions of money (I) • Money is a medium of exchange: • facilitates the flow of goods and services; • the only financial asset that anyone will accept in payment for goods and services; • by itself, money typically has little or no use as a commodity; • people accept money only because they know that they can exchange it at a later date for goods and services; • promotes economic efficiency by minimizing the time spent in exchanging goods and services (transaction cost); • money eliminates the trouble of finding a double coincidence of needs. A medium of exchange must: • be easily standardized; • be widely accepted; • be divisible; • be easy to carry; • not deteriorate quickly.

Functions of money (II) 2) Money is a standard of value (or unit of account): • measures value in economy (the value of the goods and services); • measures the relative worth of different goods; • without money, the price of every product or service would have to be expressed in terms of the exchange ratio with all the other goods and services an enormous information for both buyers and sellers; • the formula for telling us the number of prices we need when we have N goods is the formula that tells us the number of pairs when there are N items: • using money as a unit of account reduces transaction costs in an economy by reducing the number of prices that need to be considered.

Functions of money (III) 3) Moneyis a store of value; • money is a reserve of purchasing power (PP) over time; • it is used to save PP from the time income is received until the time it is spent; • any asset is a store of wealth: there are goods that store the PP better than money in the long run; • why do people hold money? it is liquid: an asset is liquid if it can be converted into cash quickly with little or no loss in value; • other assets involve transaction costs when they are converted into money; • it is the only perfectly liquid asset: • 3 essential characteristics of a liquid asset: • price stability; • ready marketability; • reversibility. • the most liquid assets tend to carry the lowest rate of return; • the value of money depends on the price level;

Money supply • Money supply is the entire stock of monetary assets (currency and other liquid instruments) within an economy as of a particular time. • The money supply can include: • cash (coins and banknotes); • balances held in checking and savings accounts; • other liquid assets. • The money supply is usually expressed in terms of four growing categories M0, M1, M2, and M3, also known as monetary aggregates. • The categories grow in size: • M3 representing all forms of money; • M0 being just monetary base (coins, bills, and central bank deposits). • Their construction differs from country to country depending some criteria.

Criteria for Monetary Aggregate Classifications (I) 1. Degree of liquidity: • financial assets with high liquidity are included in narrower measures. • financial assets with lower liquidity are included in broader measures. 2. The size of the denomination or minimum deposits: • financial instruments requiring small denominations or low minimum levels are in narrower measures, on the assumption that these tend to be held by households. • financial instruments requiring large denominations or high minimum levels are in broader measures or not included at all. 3. The original maturity of the deposits: • maturity may not matter at all (United States and Australia). • some countries place deposits with short original maturities in narrower money (ECB, Romania). 4, The characteristics of the asset holders: • personal holdings are in narrower money than non-personal holdings.

Criteria for Monetary Aggregate Classifications (II) 5. Foreign currency denominated deposits: • are excluded from the monetary aggregates by most countries or included only in broad money, with some exceptions (ECB, Norway). 6. The types of money issuers: • central banks are the issuers of currencies. 7. The types of financial institutions: • deposits with commercial banks are in narrower money than those with non-bank depository institutions. 8. The scope of money holders: • money holders usually consist of the private non-bank (or non-depository) residents. 9. Location of depository institutions: • deposits at oversea branches of domestic depositories may be excluded or included only in broader money than those at domestically located depository institutions.

Monetary aggregates(I) • M0 (monetary base, money base or reserve money): • cash money: • currency circulating in the hands of the public (outside of banks) • currency held in the bank’s vault • commercial bank deposits held in the CB’s reserves; • it is not a component of money supply. • M1 (narrow money): • currencies in circulation outside of banks; • demand deposits held by the public; • is the most liquid component of money supply. • M2 (intermediate money) = M1 plus: • savings accounts, term deposits, small certificates of deposit • is also called “quasi-money”. • M3 (broad money) = M2 plus • other less liquidity assets (large deposits, debt securities, repurchase agreements, money merket shares, foreign currency deposits, etc.)

Monetary aggregates(II) • There are some countries that also have M4 (L – general liquidity). • M1 focuses mainly upon immediately spendable money and views money primarily as a medium of exchange. • M2 and M3 reflect mainly the role of money as a store of value. • L reflects both store of value role and the near-money assets held by the public that can be quickly converted (liquidated) into spendable cash. • M0 is a term relating to money supply, consisting of only the most liquid forms of money. • The equation below reflects the relation between M0 and M1: M0*m = M1 • where: • M0 – monetary base: M0=Currency+Reserves = Currency + Deposits* Required Reserve Ratio • m – money multiplier • M1 – narrow money

Monetary aggregates in USA In March 2006, the FED ceased publishing the M3 monetary aggregate.

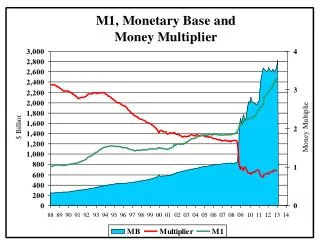

Evolution of U. S. money supply (USD billion) Source: http://www.nowandfutures.com/key_stats.html Some analysts compute M3 using various weekly Federal Reserve reports that are still available.

Evolution of U. S. money supply M2 Source: https://fred.stlouisfed.org/series/M2

Evolution of U. S. money supply M1 Source: https://fred.stlouisfed.org/series/M2

Monetary aggregates in euro area (I) • Based on conceptual considerations and empirical studies, and in line with international practice, the Eurosystem has defined a narrow aggregate (M1), an "intermediate" aggregate (M2) and a broad aggregate (M3). • These aggregates differ with regard to the degree of moneyness of the assets included. • M1 (“narrow” monetary aggregate)composed by: • Currency in circulation • Overnight deposits • M2 (“intermediate” monetary aggregate)composed by M1 plus: • Deposits with an agreed maturity of up 2 years • Deposits redeemable at notice with a maturity of up to 3 months • M3 (“broad” monetary aggregate)composed by M2 plus: • Repurchase agreements (repo) • Money market fund shares/units (MMF shares/units) • Debt securities with a maturity of up to 2 years.

Monetary aggregates in euro area (II) • Narrow money (M1): • Includes: • currency (banknotes and coins); • balances which can immediately be converted into currency or used for cashless payments (overnight deposits). • "Intermediate" money (M2): • comprises: • narrow money (M1); • deposits with a maturity of up to two years and deposits redeemable at a period of notice of up to three months; • depending on their degree of moneyness, such deposits can be converted into components of narrow money; • in some cases there may be restrictions involved, such as the need for advance notification, delays, penalties or fees.

Monetary aggregates in euro area (III) • Broad money (M3) : • comprises: • M2; • marketable instruments issued by the Monetary Financial Institutions (MFI) sector: • repurchase agreements, • money market fund shares/units • debt securities with a maturity of up to and including two years (including money market paper). • a high degree of liquidity and price certainty make these instruments close substitutes for deposits; • as a result of their inclusion, M3 is less affected by substitution between various liquid asset categories than narrower definitions of money; • is therefore more stable.

Repurchase agreements (repo): • a type of short-term loan much used in the money markets, whereby the seller of a security agrees to buy it back at a specified price and time; • for the party selling the security it is a repo; • for the party buying the security it is a reverse repo. • CBs often use repos to boost money supply, buying government securities from commercial banks and selling them back at a later date; • when the CB wants to tighten money supply, it sells the securities first, and buys them back later – this is called a reverse repo, an agreement to lend securities rather than funds. • Money market funds share/units: • a money market fund is an open-ended mutual fund (a collective investment scheme) that invests in short-term securities, such as Treasury bills, certificate of deposits and other money-market instruments; • money market funds are regarded as being as safe as bank deposits, providing a similar yield; • investors can purchase shares/units of money market funds through mutual funds, brokerage firms and banks.

Eurocurrency: • foreign currency deposited in banks outside the home country; • the most important are Eurodollars, which are U.S. dollars deposited in foreign banks outsidethe U.S. or in foreign branches of U.S. banks; • the euro, can create some confusion about this term: a currency denominated in euro is called Eurocurrency only if it is deposited outside the countries that have adopted the euro. • Monetary financial institutions (MFIs): • institutions whose business are: • to receive deposits and/or close substitutes for deposits from entities other than MFIs • and, for their own account (at least in economic terms), to grant credits and/or make investments in securities. • include: • central banks • credit institutions • other deposit-taking corporations • money market funds

Monetary aggregates and loans to the private sector in the euro area (annual growth rate)

Monetary aggregates and loans to the private sector in the euro area (annual growth rate) Source: https://www.ecb.europa.eu/press/pdf/md/md1612.pdf

Monetary aggregates in Romania • Since January 2007, the NBR has used: • M0 (reserve money) comprising: • Credit institutions vault cash • Currency in circulation • Credit institutions current account • M1 comprising • Currency in circulation • Overnight deposits • M2 including M1 plus • Deposits with an agreed maturity of up to and including 2 years • M3 made up of M2 plus • Repos operations • Money market fund shares/units (outstanding) • Debt securities.

Counterparts of money supply • Money supply is reflected in the liabilities side of the aggregate monetary balance sheet of MFIs (credit institutions and money market funds). • Money supply has as counterparts foreign and domestic assets of the aggregate monetary balance sheet of MFIs, such as: • Cash and other payment means • Loans: • to private sector • to household • to government • Debt securities held • Money market fund shares/units held • Equity (including investment fund shares/units) held • The counterparts of money supply represent the source of money creation in an economy.

Evolution of Romania money supply (RON thousand) Source: author’s processing using data available on www.bnr.ro

Evolution of Romania money supply counterparts (RON thousand) • Source: author’s processing using data available on www.bnr.ro

Equation of exchange • developed by Irving Fisher (1911) • relates nominal income to the quantity of money and velocity: M*V = P*Y, • where: • M – money supply • V – velocity of money – the rate of turnover of money (the average number of times per year that a monetary unit is spent in buying the total amount of goods and services produced in the economy) • P – price level • Y – real income • P*Y – nominal income (nominal GDP) • states that the quantity of money multiplied by the number of times that this money is spent in a given year must be equal to nominal income