Download

1 / 11

110 likes | 119 Views

Marine Management Organisation and Sea Bed User and Developer Group Work shop. 30 th March 2017. Prepared by: Sophie Hartfield. Approved by:. Brief History of Offshore Wind in the UK. Blyth Offshore became the UK's first offshore wind farm when it was commissioned in December 2000.

E N D

Marine Management Organisation and Sea Bed User and Developer Group Work shop 30th March 2017 Prepared by: Sophie Hartfield Approved by:

Brief History of Offshore Wind in the UK • Blyth Offshore became the UK's first offshore wind farm when it was commissioned in December 2000. • Crown Estate owns almost all the UK coastline out to 12 nautical miles. • ‘Round 1’ - 18 sites of up to 30 turbines • ‘Round 2’ - 15 projects of up to 7.2 GW • ‘Round 3 – Target of 33 GW by 2020 There are now enough UK offshore wind farm sites built, under construction or in the planning system to power around 5 million homes.

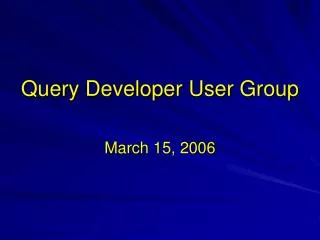

DONG Energy Wind Power overview DONG Energy Wind Power geographical footprint Unparalleled experience and track record Bay State Wind In operation 26 years of experience and track recordin the offshore wind sector 1991 2017 Under construction APAC Taipei office Under development Ocean Wind 21offshore wind farms in operation 7 offshore wind farms under construction Anholt Middelgrunden Walney 1 & 2 Horns Rev 1 & 2 Walney Extension Avedøre Westermost Rough Hornsea 1 West of Duddon Sands Vindeby Hornsea 2 & 3 & 4 Nysted Isle of Man Race Bank 3.6 GW Constructed capacity 2,000 Dedicated employees 3.8 GW under construction Gode Wind 2 Lincs Gode Wind 3 & 4 Barrow Gode Wind 1 Gunfleet Sands 1 & 2 Burbo Bank Ext. Borkum Riffgrund 1 Borssele 1&2 Burbo Bank Borkum Riffgrund 2 Gunfleet Sands 3 German Cluster London Array 7.5 million Europeans with clean electricity 3.6 GW World's leading operator 14 Partnerships

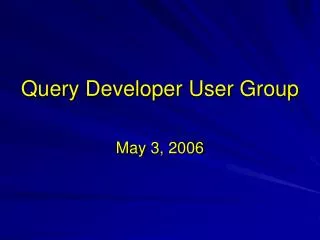

Proven construction track-record and leading operating capabilities Strong construction track-record due to full EPC1 control Leader in operating offshore wind farms# of operated turbines January 2017 2x Vattenfall E.On Innogy SSE Centrica Statoil Source: Bloomberg New Energy Finance January 2017 • Engineering, procurement and construction

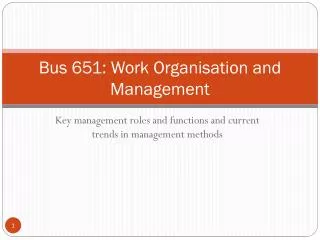

Proven track record in developing long-term partnerships Westermost Rough (50%) 210 MW (2014) Race Bank (50%) 573 MW (2016) Walney I & II (50.1%) 367 MW (2009 / 2010) Anholt (50%) 400 MW (2011) Horns Rev 1 (40%) 160 MW (2006) West of Duddon Sands (50%) 389 MW (2010) Nysted (42.7%) 166 MW (2010) Burbo Bank Extension (50%) 258 MW (2016) (KIRKBI) Gode Wind 2 (50%) 252 MW (2014) Lincs (25%) 270 MW (2017)* London Array (25%) 630 MW (2009 / 2014) Gunfleet Sands (50.1%) 173 MW (2011) Borkum Riffgrund 1 (50%) 312 MW (2012) Gode Wind 1 (50%) 330 MW (2015) (KIRKBI) ( ) represents DONG Energy ownership interest * The transaction is subject to approval by the competition authorities. The transaction is expected to be completed in February 2017 Major institutional investors are partners in DONG Energy's offshore wind projects

Getting energy to shore Building an offshore wind farm

Supporting the Consent application, pre construction, construction and operation Potential Environmental Impacts to be considered – other infrastructure: • OWFs • Oil & Gas • Aggregates • Cables and Pipelines • Ports and Navigational Dredging • Disposal Sites • Carbon Capture and Storage • Aquaculture Potential Environmental Impacts to be considered – social: • Local Impact Assessment • Commercial Fisheries • Shipping and navigation • Archaeology • Leisure and Tourism • Visual impacts • Supply chain Potential Environmental Impacts to be considered – environment: • Designations • Conservation value • Marine mammals • Birds • Benthos • Fish & Shellfish • Bathymetry • Archaeology • Coastal processes • Newts • Bats

Challenges • Further Offshore & Lowering the Cost of Energy • Supply Chain Bottlenecks • Lack of data on impacts • Grid connection constraints • Limited choice of contractors/suppliers • Deep water engineering • Health and Safety • O&M Strategies • Still a “young” industry • New Designations • Commercial Fisheries • BREXIT • Resourcing • Lowering the Cost of Energy