Download

1 / 136

1.42k likes | 1.75k Views

Hedging Strategies Using Futures. Chapter 3. HEDGERS OPEN POSITIONS IN THE FUTURES MARKET IN ORDER TO ELIMINATE THE RISK ASSOCIATED WITH THE SPOT PRICE OF THE UNDERLYING ASSET. Spot price risk. Pr. S j. S t. time. j. t.

E N D

Hedging Strategies Using Futures Chapter 3

HEDGERS OPEN POSITIONS IN THE FUTURES MARKET IN ORDER TOELIMINATE THE RISK ASSOCIATED WITH THESPOT PRICEOF THE UNDERLYING ASSET

Spot price risk Pr Sj St time j t

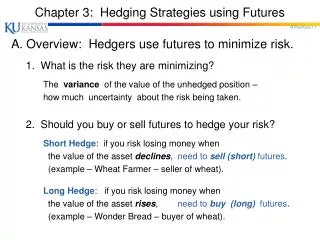

HEDGERSPROBLEM: TO OPEN A LONG HEDGEOR A SHORT HEDGE?There are two ways to determine whether to open a short or a long hedge:

1. A LONG HEDGE A SHORT HEDGE OPEN A LONG FUTURES POSITION IN ORDER TO HEDGE THE PURCHASE OF THE PRODUCT AT A LATER DATE. THE HEDGER LOCKS IN THE PURCHASE PRICE. OPEN A SHORT FUTURES POSITION IN ORDER TO HEDGE THE SALE OF THE PRODUCT AT A LATER DATE. THE HEDGER LOCKS IN THE SALE PRICE

2. A LONG HEDGE A SHORT HEDGE OPEN A LONG FUTURES POSITION WHEN THE FIRM HAS A SHORT SPOT POSITION. OPEN A SHORT FUTURES POSITION WHEN THE FIRM HAS A LONG SPOT POSITION.

Example: A LONG HEDGE DateSpot marketFutures marketBasis t St = $800/unit Ft,T = $825/unit -25 Contract to buy long one gold Gold on k. futures for delivery at T k Buy the gold Short one gold Sk = $816/unit futures for delivery at T. Fk,T = $842/unit-26 1 T Amount paid: 816 + 825 – 842 = $799/unit or 825 + (816 – 842) = $799/unit

Example: A SHORT HEDGE DateSpot marketFutures marketBasis t St = $800/unit Ft,T = $825/unit -25 Contract to sell short one gold Gold on k, futures for delivery at T k Sell the gold Long one gold Sk = $784/unit futures for delivery at T. Fk,T = $812/unit -28 3 T Amount received: 784 + 825 – 812 = $797/unit or 825 + (784 – 812) = $797/unit

NOTATIONS: t< T t = current time; T = delivery time F t,T = THE FUTURES PRICE AT TIME t FOR DELIVERY AT TIME T. St = THE SPOT PRICE AT TIME t. k = THE DATE UPON WHICH THE FIRM TRADES THE ASSET IN THE SPOT MARKET. k ≤ T Sometimes t = 0 denotes the date the hedge is opened.

THE HEDGE TIMING k = is the date on which the hedger conducts the firm spot business and simultaneously closes the futures position. This date is almost always before the delivery month; k ≤ T. Today Trade spot andDelivery Open the hedge: Close the futures open a futures position position t k TTime

THE HEDGE TIMIMG Date k is (almost) always before the delivery month. WHY? • Often k is not in any of the delivery months available. 2. From the first trading day of the delivery month, the SHORT can decide to send a delivery note. Any LONG with an open position may be served with this delivery note.

Spot and Futures prices over time Commodities and assets are traded in the spot and futures markets simultaneously. Thus, the relationship between the sport and futures prices: At any point in time And Over time Is of great importance for traders.

The Basis The basis at any time point, j, is the difference between the asset’s spot price and the futures price on j. BASISj = SPOT PRICEj - FUTURES PRICEj Notationally: Bj = Sj - Fj,T j < T. When discussing a basis, one must specify the futures in question, i.e., a specific delivery month. Usually, however, it is understood that the futures is for the nearest month to delivery.

A LONG HEDGE TIMESPOTFUTURESB t Contract to buy LONG Ft,T Bt Do nothing k BUY Sk SHORT Fk,T Bk T delivery Actual purchase price = Sk + Ft,T - Fk,T = Ft,T + [Sk - Fk,T] = Ft,T +BASISk

A SHORT HEDGE TIMESPOTFUTURESB t Contract to sell SHORT Ft,T Bt Do nothing k SELL Sk LONG Fk,T Bk T delivery Actual selling price = Sk + Ft,T - Fk,T = Ft,T + [Sk - Fk,T] = Ft,T +BASISk

In both cases, Long hedge and short hedge the hedger’s purchase/sale price, when the hedge is closed on date k, is: Ft,T +BASISk This price consists of two portions: a known portion: Ft,T and a random portion: the BASISk We return to this point later.

ALSO NOTICE: The purchase/sale price when the hedge is closed on date k is: Ft,T +BASISk Which may be rewritten: = Ft,T + BASISk + St – St = St – [St – Ft,T - Bk] = St + [Bk – Bt] t k T

Spot prices and futures prices over time The key to the success of a hedge is the relationship between the cash and the futures price over time: Statistically, Futures prices and Spot prices of any underlying asset, co vary over time. They tend to co move “together” ; not in perfect tandem and not by the same amount, nevertheless, these prices move up and down together most of the time, during the life of the futures.

Openclose the hedge Long hedgeShort hedge a successa failure Loss on the hedge a failurea success Loss on the hedge Fk,T Sk Fk,T Sk Ft,T St

Example: A LONG HEDGE TIMESPOTFUTURESBASIS t St= $3.40 LONG Do nothing Ft,T=$3.50 -$.10 k BUY Sk=$3.80 SHORT F k,T=3.85 -$.05 T delivery Actual purchase price: NO hedge: $3.80 With hedge: $3.45 (Successful hedge)

Example: A LONG HEDGE TIMESPOTFUTURESBASIS t St= $3.40 LONG Do nothing Ft,T=$3.50 -$.10 k BUY Sk=$3.00 SHORT F k,T=3.05 -$.05 T delivery Actual purchase price: NO hedge: $3.00 With hedge: $3.45 (Unsuccessful hedge)

The basis upon delivery: BT = 0 On date k, the basis is Bk = Sk - Fk,T k < T. If k coincides with the delivery date, however, k = T. The basis is: BT = ST - FT, T at T. BUT, FT,T is the futures price on date T for delivery on date T, which implies that: FT,T = ST BT = 0.

Convergence of Futures to Spot over the life of the futures Futures Price Spot Price Futures Price Spot Price Time Time (a) (b)

Basis Risk The Basis is the difference between the spot and the futures prices. I.e., the Basis is a RANDOM VARIABLE. Thus, Basis risk arises because of the uncertainty about the Basis when the hedge is closed out on k. The basis, however, is the difference of two random variables and thus, the Basis is LESS RISKY than each price by itself. Moreover, we do know that BT = 0 upon delivery.

Generally, the basis fluctuates less than both, the cash and the futures prices. Hence, hedging with futures reduces risk. Basis risk exists in any hedge, nonetheless. Sk Pr Bk Ft,T St BT = 0 Bt time k T t

We showed that for both types of hedge A SHORT HEDGE or A LONG HEDGE, The price received/paid by the hedger: Ft,T +BASISk This price consists of two parts: Part one: Ft,T is KNOWN when the hedge is opened. Part two: BASISk is risky.

Conclusion: At time t, WITHOUT HEDGING cash-price risk. WITH HEDGING, basis risk. Hedging with futures is nothing more than changing the firm’s spot price risk Into a smaller risk, namely, The basis risk.

A CROSS HEDGE: When there is no futures contract on the asset being hedged, choose the contract whose futures price is most highly correlated with the spot asset price. NOTE, in this case, the hedger creates a two components basis: one component associated with the asset underlying the futures and one component associated with the spread between the two spot prices.

A CROSS HEDGE: Let S1t be the spot asset price at time t. Remember! - This is the asset that the hedger is trying to hedge; e.g. jet fuel. Let S2t be the spot price at time t of the asset underlying the futures. E.g., natural gas. This, of course, is a different asset and that is why this hedge is called a CROSS HEDGE

A CROSS HEDGE TIMECASHFUTURES t Contract to trade S1 Ft,T(2) Do nothing k Trade for S1K Fk,T(2) T delivery PAY/RECEIVE= S1K + Ft,T(2) - Fk,T(2) = Ft,T(2) +[S2k - Fk,T(2)] +[S1k - S2k] = Ft,T(2) +BASIS(2)k + SPREADK

Arguments in Favor of Hedging Companies should focus on the main business they are in and take steps to minimize risks arising from interest rates, exchange rates, and other market variables

Arguments against Hedging • Explaining a situation where there is a loss on the hedge and a gain on the underlying can be difficult. • Shareholders are usually well diversified and can make their own hedging decisions.

Delivery month? MOSTLY, the hedge is opened with a futures for the delivery month closest to the firm’s spot trading of the asset, or the nearest month beyond that date. The key factor in choosing the futures’ delivery month is the correlation between the spot and futures prices or price changes. Statistically, in most cases, the spot price highest correlation is with the nearest delivery month futures price, which is closest to the firm’s cash activity.

The number of Futures to use in the hedge Open a hedge. Questions: Long or Short? Delivery month? Commodity to use? How many futures to use in the hedge?

HEDGE RATIOS, NOTATION: NS = The number of units of the commodity to be traded in the SPOT market. NF = The number of units of the commodity in ONE FUTURES CONTRACT. n = The number of futures contracts to be used in the hedge. h = The hedge ratio.

HEDGE RATIOS: Open a hedge. Question: Given that the firm has a contract to trade NS units of the underlying commodity on date k in the spot market and given that one futures covers NF units of the underlying commodity: How many futures to use in the hedge? i.e., what is n?

HEDGE RATIOS, DEFINITION: The hedge ratio, h, determines the number of futures to hold, n.

THE NAÏVE HEDGE RATIO: h = 1. The total number of units covered by the futures position = nNF , exactly covers the number of units to be traded in the spot market = NS.

Examples:NAÏVE HEDGE RATIO: h = 1. • A firm will sell NS = 75,000 • barrels of crude oil. • NYMEX WTI: NF = 1,000 barrels. • SHORT: • n = 75,000/1,000 • = 75 NYMEX futures.

A firm will buy NS = 200,000 • bushels of wheat. • CBT wheat futures: NF = 5,000. • LONG: • n = 200,000/5,000 • = 40 CBT futures.

A firm will sell NS = 3,600 • ounces of gold. • NYMEX gold futures: NF = 100 ounces. • SHORT: • n = 3,600/100 • = 36 CBT futures.

How to open a long hedge with multiple future spot trading? A Strip. DATESPOT MARKET Sep1,07 Contract to buy 75,000bbls of WTI crude oil. on: Oct 1,07; Nov 1,07; Dec 1,07; Jan 2,08.

A STRIP. A STRIP is a hedge in which there are several long (or several short) positions opened simultaneously with equal time span between the delivery months of the positions. Each one of these futures exactly hedges a specific future trade in the spot market

Open a long STRIP with h = 1 DATESPOT MARKETSFUTURES MARKETFFUTURES POSITIONS Sep1,07 contract to 92.00 buy 75,000bbls on Oct 1,07; Nov 1,07; Dec 1,07; Jan 2, 08. Long 75 NOV 07 93.00 long 75 NOV 07 Long 75 DEC 08 93.50 long 75 DEC 08 Long 75 JAN 08 93.85 long 75 JAN 08 Long 75 FEB 08 94.60 long 75 FEB 08

DateSPOT MARKETSFUTURES MARKETFFUTURES POSITIONS • Sep1,07 contract to 92.00 Long 75 NOV 2007 93.00 long 75 NOV 2007 buy 75,000bbls Long 75 DEC 2007 93.50 long 75 DEC 2007 Long 75 JAN 2008 93.85 long 75 JAN 2008 Long 75 FEB 2008 94.60 long 75 FEB 2008 • Oct1,07 buy 75,000bbls 93.00 short 75 NOV 07 93.10 long 75 DEC 2007 • long 75 JAN 2008 • long 75 FEB 2008 • Nov1,07 buy 75,000bbls 92.90 short 75 DEC 07 93.05 long 75 JAN 2008 • long 75 FEB 2008 • Dec1,07 buy 75,000bbls 94.00 short 75 JAN 08 94.15 long 75 FEB 2008 • Jan2,08 buy 75,000bbls 94.75 short 75 FEB 08 94.95 NO POSITION • The average price for the un hedged strategy : (93+92.90+94+94.75)/4 = 93.660 • The average price for the hedged strategy: • 93.00 + (93.00 - 93.10) = 92.90 • 93.50 + (92.90 – 93.05) = 93.35 • 93.85 + (94.00 – 94.15) = 93.609 • 94.60 + (94.75 - 94.95) = 94.40 • 93.5625

ROLLING THE HEDGE FORWARD Lack of sufficient liquidity in contracts for later delivery months may cause firms to hedge a long-term business trade employing shorter term hedges. In this case, the shorter term hedges must be rolled over until the firm trade in the cash market.

Roll over hedge with h = 1 DATESPOT MARKETSFUTURES MARKETFFUTURES POSITIONS DEC, 07 contract to sell 89.00 Short 100 NYMEX WTI; 88.20 100,000bbls on Futures for delivery on JAN, 09. MAY 08 SHORT 100 MAY 08 Fs. And Roll over the hedge on APR 2008 And AUG 2008

DateSPOT MARKETSFUTURES MARKETFFUTURES POSITIONS DEC, 07 contract to 89.00 short 100 MAY WTI 88.20 sell 100,000 bbls Oct1,07 buy 75,000bbls Short 100 MAY 2008 APR 08 long 100 MAY 2008 87.40 Short 100 SEP 2008 87.00 Short 100 SEP 2008 AUG 08 Long 100 SEP 2008 86.50 Short 100FEB 2009 86.30 Short 100 FEB 2009 JAN, 09 sell 100,000bbls 86.00 Long 100 FEB 2009 85.90 NO POSITION The selling price without the rolling hedge: $86.00/barrel The selling price with the rolling hedge: $87.70/barrel $86.00 + (88.20 – 87.40) + (87.00 – 86.50) + (86.30 – 85.90) = 87.70.

Other hedge ratios. Suppose that the relationship between the spot and futures prices over time is: SpotFutures case one: $1 $2 Case two: $1 $0.5 Clearly, the Naïve hedge ratio is not appropriate in these cases.

THE MINIMUM VARIANCE HEDGE RATIO OBJECTIVE: To minimize the risk associated with the hedge RISK = VOLATILITY. THE VOLATILITY MEASURE: THE VARIANCE