Download

1 / 8

100 likes | 289 Views

Interest Rate and Currency Swaps. Interest Rate Swaps(A). 1. An Interest Rate Swap is a derivative. That is, it is derived from various money market and bond market instruments. It is not a direct source of funding.

E N D

Interest Rate Swaps(A) • 1. An Interest Rate Swap is a derivative. That is, it is derived from various money market and bond market instruments. It is not a direct source of funding. • 2. Originally Interest Rate Swaps were developed to allow different borrowers to arbitrage different markets to get below target borrowing costs. (Example: Tektronix and Wells Fargo Bank)

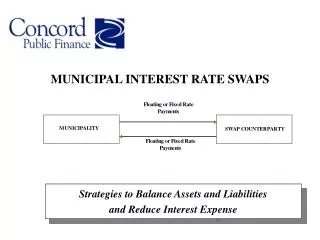

Interest Rate Swaps(B) • 3. An Interest Rate Swap allows one counterparty to receive a certain type of interest payment. And to pay a different type of interest payment. Both the payment and the receipt are in the same currency. • 4. The most common Interest Rate Swap has one counterparty receiving 3 or 6 month LIBOR and paying a fixed rate for the tenor of the swap. (Tenors can be as long as 30 years).

Interest Rate Swaps(C) • 5. The interest payments are based on a notional amount and only the net amount is paid or received. • 6. As a derivative it is off balance sheet, while the underlying investment or borrowing is on balance sheet. • 7. These swaps are used to convert a borrowing from fixed rate to floating or to manage interest rate risk.

Interest Rate Swaps(D) • 1. Initially these transactions were done a matched basis. But with the advent of desktop computing power and the development of a variety of interest rate futures contracts, banks could warehouse any mismatches and two way quotes became common. • 2. Banks that quote prices for interest rate swaps are called Swap Banks.

Swap Banks(A) • 1. Swap Banks provide its clients with two way quotes. For example a quote of 2.15% - 2.20% for five years against 6 month LIBOR means the Swap Bank will pay 2.15% and receive 6 month LIBOR or receive 2.20% and pay 6 month LIBOR. • 2. Thus if a client wanted to receive fixed it would receive 2.15% and pay the 6 month LIBO rate.

Swap Banks(B) • 1. The Swap Bank acts as a counterparty to the transaction to provide a higher degree of credit safety • 2. The Swap Bank also manages any mismatch in principal amortization schedules.

Currency Swaps • 1. Currency Swaps are similar to Interest Rate Swaps but are in different currencies. • 2. Since the currencies are different the principal payments are also paid and received. • 3. For example, a corporation may want to pay floating rate dollars and receive fixed yen. The fixed yen may offset the payments on a yen based loan. The net effect is to change the loan from fixed yen to floating dollars.